It is generally accepted that artificial intelligence (AI) is reshaping industries and society. However, this is not the first time we are experiencing a technological revolution that inspires uncertainty, speculation and exuberance; there have been plenty of transformative disruptions in the past when, in the early stages, it was difficult to predict outcomes. From an investment perspective, history reminds us that identifying the long-term winners is rarely straightforward. Nshalati Hlungwane shares some enduring lessons from previous waves of technological disruption, including the railway and telecommunications booms, and discusses how they can help us navigate the unknowns of AI.

Over the last few years, AI has dominated news headlines and investor attention, with AI companies experiencing extraordinary growth. Listed AI darling Nvidia has seen its market capitalisation grow 13 times over the past five years, from US$340bn to US$4.3tn, while Anthropic, a private US-based AI company, is valued at US$380bn following a recent funding round – a twofold increase in less than six months. These numbers are eye-watering. Is this a bubble? Are we going through a step change? Will those who just observe miss out?

… long-term investing is not about predicting how technological change will unfold; it is about identifying resilient businesses ... that will thrive under changing circumstances …

Although history may not repeat itself, it does rhyme. Technological disruption in the past has prompted similar questions – and revealed there will always be some winners and many losers. The spoiler alert is that there is no way of knowing who the winner will be, how a technology will spread, or if it will have a lasting impact. Rather than trying to guess, we focus on company fundamentals and valuation-driven analysis in our bid to deliver long-term returns.

Looking back

As shown in Figure 1, history teaches us important lessons:

- Technological disruption does not necessarily reward the earliest participants. Some firms fail, others merge, and new entrants emerge with better business models or more effective ways of applying the technology. Sometimes the largest beneficiaries are not even directly invested, but capitalise on newfound economic opportunities created by the deployment of the technology.

- Investors rush to participate, valuations rise sharply, and companies expand aggressively. Eventually, reality sets in as expectations exceed what can be delivered in the short term.

- Technological disruption is typically followed by a period of exorbitant capital expenditure on expanding the infrastructure required to unlock the technology. Industries requiring large upfront investment can experience cycles of overinvestment and consolidation.

- The adoption of a new technology takes time. Infrastructure may be built long before the most valuable applications emerge.

- When large capital expenditure forms part of the new technology’s development, sufficient time is needed to generate sustainable revenues to recover those initial costs.

Looking back at previous periods of disruptive innovation, such as the development of British railways in the 19th century and the telecommunications boom of the late 1990s, offers valuable perspective on how new technologies evolve, and how investors can navigate a changing world. As futurist Roy Amara observed: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.”

The railway revolution

Before railways, Britain’s transport system was dominated by horse-drawn vehicles on roads, canals for heavy freight, and coastal shipping for long-distance bulk transport. The introduction of railway lines was initially met with safety concerns, but the economics of moving large volumes of both passengers and freight at faster speeds and lower cost made their expansion inevitable.

Establishing a company was relatively straightforward back then. Importantly, investors initially only had to pay about 10% of the capital required, with the remainder called later as construction progressed. The success of the first railway lines sparked early waves of excitement and encouraged new capital formation. Enthusiasm intensified in the mid-1830s after the UK’s parliament approved dozens of new lines. However, this surge proved short-lived: A financial panic and recession soon reversed fortunes, sending railway stocks into decline. The true boom arrived in the 1840s.

“We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.”

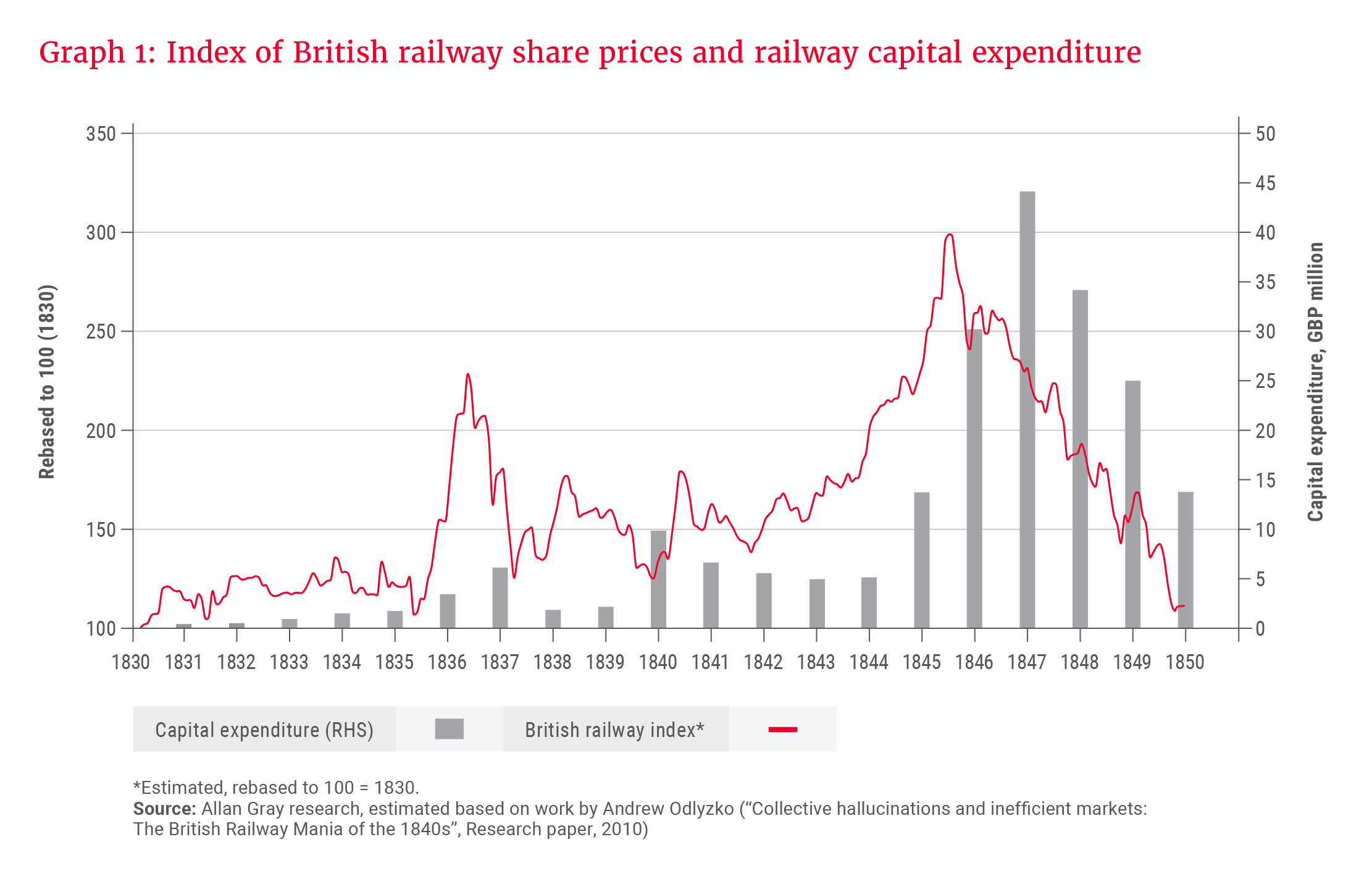

Petitions for new railway companies surged from 63 in 1843 to over 560 in 1845, driven by a growing middle class, easy access to capital, strong economic conditions and lower interest rates. Railway share prices doubled between 1843 and 1845, while capital expenditure rose from about GBP5m prior to 1843 to a peak of GBP44m in 1847, as shown in Graph 1 below. This frenzy became known as the British Railway Mania.

However, the boom proved unsustainable. Given that investors had committed only 10% of the required capital upfront, many found themselves unable to meet further payments when construction costs escalated. At the same time, economic conditions deteriorated. Interest rates rose, food prices increased after poor harvests, and the optimistic financial projections of many railway companies proved unrealistic.

Nearly one-fifth of planned track was abandoned, and the industry entered a long phase of consolidation through mergers and acquisitions. Over the following decades, railway shares delivered poor returns.

While hundreds of railway companies emerged during the 1840s, only a few remained and dominated. The businesses that proved more resilient and profitable were the steel manufacturers, which supplied the raw materials for the construction of railways, coal producers, which used the railways as routes to market, and the locomotive manufacturers. Much like the “pick and shovel” firms that benefited during the gold rush, these companies prospered by enabling the growth of the broader ecosystem rather than speculating on its success.

Yet despite the financial turbulence, railways transformed society. They reduced transportation costs, connected cities and rural areas, which accelerated urbanisation, and even led to the standardisation of time zones.

While returns varied significantly depending on entry point, many investors who bought during periods of peak optimism experienced disappointing long-term outcomes, but the infrastructure they financed became foundational to modern economies.

The telecoms boom

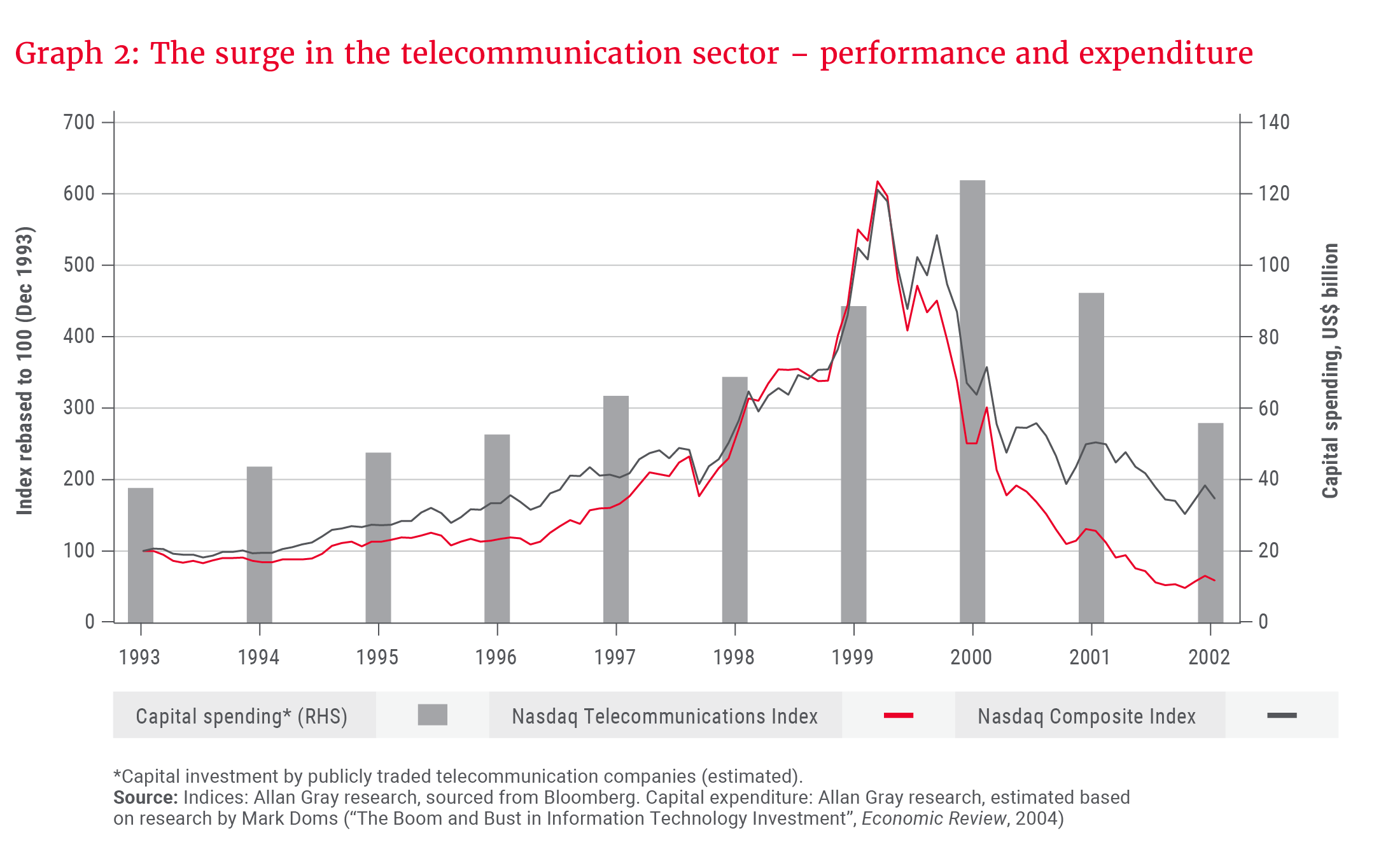

A similar pattern emerged more than a century later in the US. In the mid-90s, telecoms was seen as the next great growth engine. The 1996 US Telecommunications Act, which aimed to deregulate the sector, coincided with increasing internet use, falling mobile phone costs, and major advances in fibre-optic technology. Expectations soared that connectivity would reshape the way people worked, communicated and consumed media.

The result was a wave of new entrants and heavy investment across the industry. Between 1997 and 2000, telecom stocks surged, with the Nasdaq Telecommunications Index rising more than sixfold, as shown in Graph 2.

Much of the capital flowing into the sector funded long-haul fibre-optic networks. From 1996 to 2001, US telecom companies invested heavily in fibre-optic infrastructure, spending an estimated US$444bn and laying more than 30 million kilometres of cable. Investors believed these networks would become immensely valuable as internet use expanded and demand for bandwidth soared, reflecting the notion that “if you build it, they will come”, and an anticipation of new applications that would lead to increased demand for the infrastructure.

However, the industry dramatically overestimated near-term demand. By the early 2000s, it became clear that network capacity far exceeded actual usage. At one point, as much as 90% of installed fibre remained unused. Several major players, including WorldCom and Global Crossing, collapsed under the weight of their debt-fuelled expansion.

Yet the story did not end there. This abundant and inexpensive infrastructure later supported new digital use cases that were not anticipated at the time. Early streaming media and the rise of large web platforms began to use the excess capacity – but the real demand surge came with the emergence of the smartphone. Companies such as Apple and Samsung rely heavily on high-capacity fibre backbones to carry rapidly growing mobile data traffic, while platforms like YouTube and Netflix thrive on the widespread availability of fast internet.

The infrastructure eventually proved enormously valuable, but much of the economic value accrued to companies that built services and products on top of it, rather than those that had financed its construction.

Using yesterday’s lessons to guide us through today

We are living through the latest wave of technological disruption. While it certainly echoes past episodes, there are also distinct differences.

Similarities

- Global equity markets, as reflected in the MSCI World Index, have been driven by AI-related companies, showing a familiar pattern of investor exuberance.

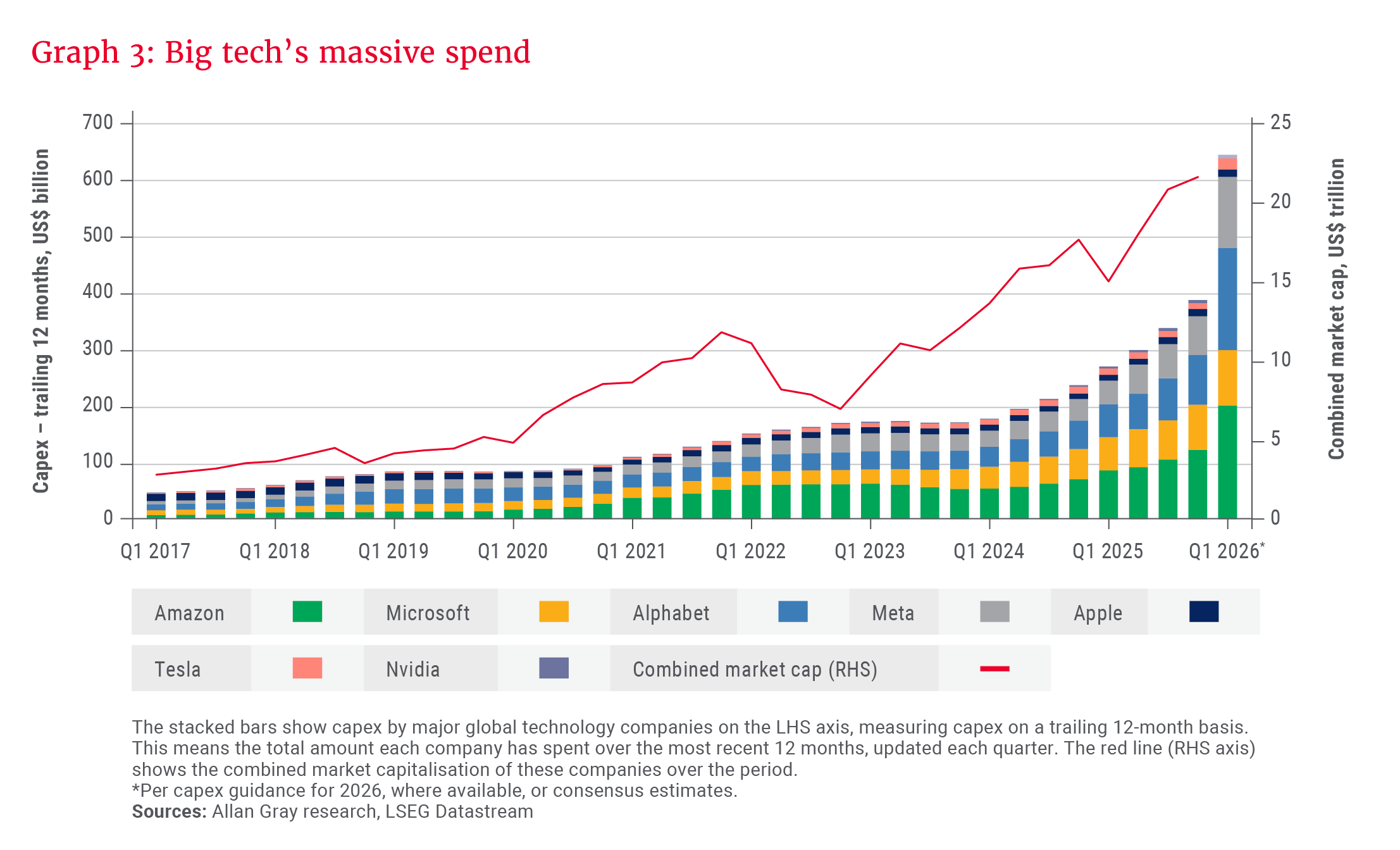

- AI companies are investing heavily in data centres and computing infrastructure, with spending exceeding US$400bn in 2025 and expected to rise above US$600bn this year – see Graph 3. (By comparison, South Africa’s GDP is around US$450bn.) This follows the pattern of considerable capital expenditure on infrastructure buildout.

Differences

- The pace of adoption is far faster than that of previous disruptions: OpenAI’s ChatGPT reached 100 million users within two months.

- Earlier technologies mainly improved efficiency by automating existing tasks; AI goes further, operating with a degree of autonomy.

Companies across sectors are investing heavily in AI, and the technology is often portrayed as transformative. While this may prove true, it remains unclear how AI will evolve, or which companies will capture the most value. As illustrated, periods of rapid innovation are often marked by high expectations, heavy investment and elevated valuations, creating both opportunity and risk.

Discipline in the face of disruption

AI is having, and will likely continue to have a profound impact on the global economy in the years ahead. As Ben Preston from our offshore partner, Orbis, notes in his article, “Is AI a bubble, or is the best yet to come?”, the challenge for investors is not determining whether the technology will matter, but rather how to participate. Orbis has been able to buy the sellers of picks and shovels that have turned out to be clear beneficiaries of AI, such as Taiwan Semiconductor Manufacturing Company, Nebius and SK Square, without having to pay high multiples.

Ultimately, long-term investing is not about predicting how technological change will unfold; it is about identifying resilient businesses with sound economics and strong management that will thrive under changing circumstances – and owning them at reasonable valuations. This is what we aim to do through the disciplined application of our investment philosophy.

AI may transform industries in ways that are difficult to foresee today, but if history offers one clear lesson, it is that maintaining discipline and perspective during periods of technological excitement remains a valuable advantage.

Explore more insights from our Q1 2026 Quarterly Commentary

- 2026 Q1 Comments from the Chief Operating Officer by Mahesh Cooper

- Dis-Chem: A great business at a great price? by Jonty Fish

- Pan African Resources: The golden goose? by Andrew Boulton

- Higher discretionary allowance: The opportunity to invest offshore by Daniel van Andel

- Orbis Global Equity: The art of adaptability in turbulent markets by Ben Preston

- Mind the gap by Horacia Naidoo-McCarthy

- Maximising new tax benefits to boost long-term investment outcomes by Shaun Duddy

To view our latest Quarterly Commentary or browse previous editions, click here.