Against a backdrop of heightened volatility, rapid advances in artificial intelligence and ongoing geopolitical tension, an adaptable, disciplined and valuation-driven investment approach is essential. Ben Preston from our offshore partner, Orbis, discusses how the Orbis Global Equity Fund is positioned to navigate the constantly evolving global landscape by tilting towards attractive shares and selectively identifying undervalued opportunities in the market.

The first quarter of 2026 was an eventful one, bringing further significant developments in artificial intelligence (AI), a sharp sell-off in software-as-a-service shares (nicknamed the “SaaS-pocalypse”), a loss of confidence in previously hot private credit funds, and, tragically, the outbreak of another war in the Middle East. We extend our thoughts and best wishes to all those caught up in that conflict and we hope for a swift resolution.

Stock markets were modestly positive in the first two months of the year – before hostilities – but declined sharply in March, with the MSCI World Index ending the quarter down by 3.6%. Against that background, the Orbis Global Equity Fund fared better, generating a modest positive return.

We seek to reorientate the portfolio continuously towards the most attractive shares.

As we have previously stressed, navigating a volatile and dynamically shifting investment environment requires adaptability. Importantly, being adaptable doesn’t mean shortening our investment horizon. Far from it – we appraise the fair value of companies as if we’re planning to own them forever. Rather, it means being responsive to new information that can change a company’s share price, our assessment of its intrinsic value, and therefore the all-important gap between the two.

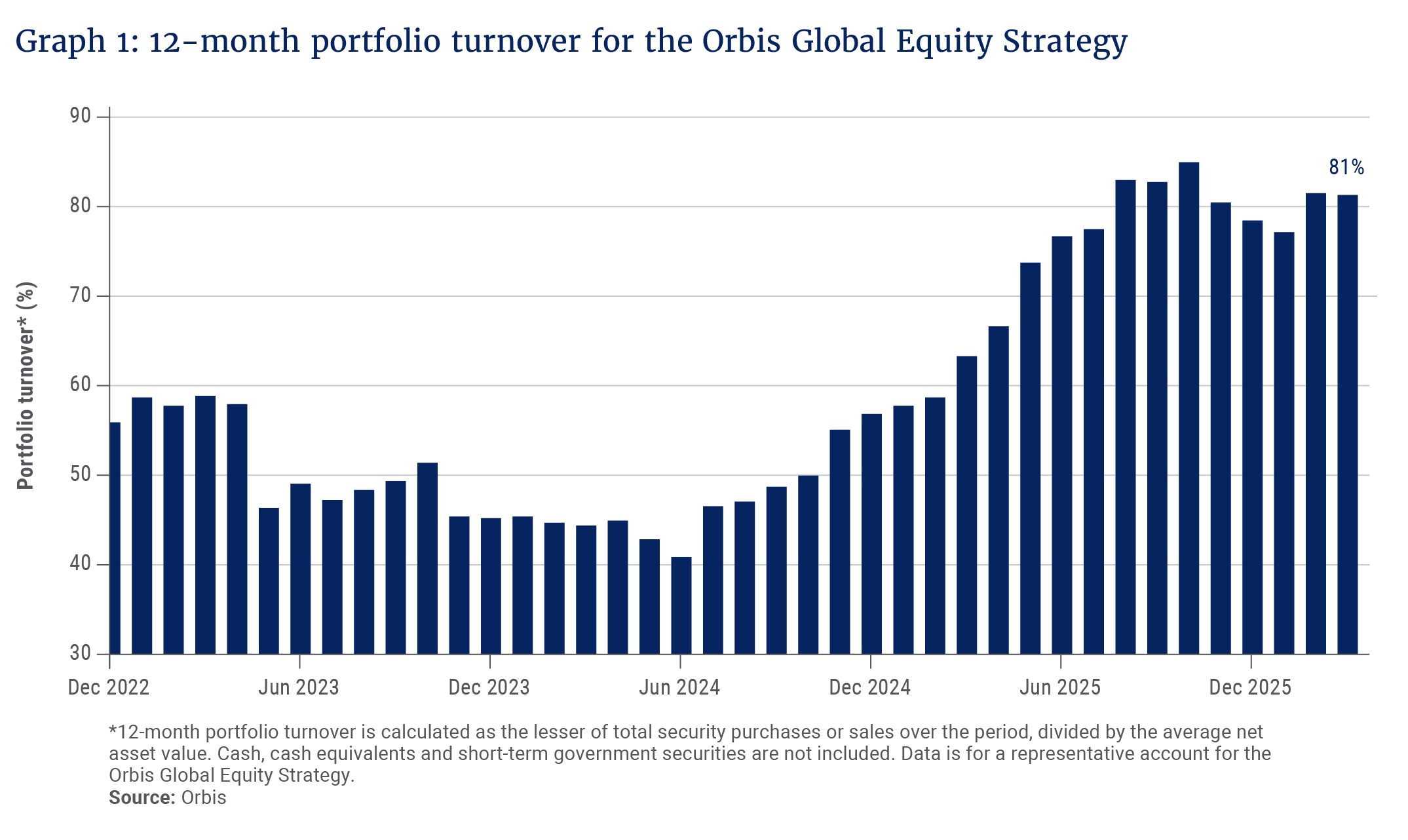

We seek to reorientate the portfolio continuously towards the most attractive shares. The faster things are moving, the greater the opportunity to actively adjust. It should therefore come as no surprise that our recent turnover has been higher than usual, as shown in Graph 1 below. We believe this to be healthy and perfectly consistent with a disciplined, long-term investment philosophy.

As well as adaptability, a changing market environment also tends to reward humility. We will not shy away from admitting our mistakes or identifying ways to learn from them, those being critical ingredients for continuous improvement. This quarter, as usual, has brought its fair share.

In particular, we will aspire to humility regarding our ability to predict the future. Last quarter, we highlighted a simple but powerful dynamic: We don’t have to be right all the time, as long as our winners win more than our losers lose. This attractive feature – positive “skew” – helped to differentiate performance relative to the losses suffered by the benchmark index.

Indeed, positive skew is a highly valuable portfolio attribute that often gets overlooked. It is tempting to believe that a high hit rate is the key to outperforming. But the nature of market pricing – a competitive tug of war between buyer and seller in an uncertain world – effectively makes it impossible to pick only winners.

That’s where skew helps. It’s not complicated; it just means identifying shares with vastly more upside than downside, and it’s one of the key benefits that result from a contrarian investment approach that emphasises margin of safety. The more volatile and uncertain the investment environment, the more valuable this skew becomes.

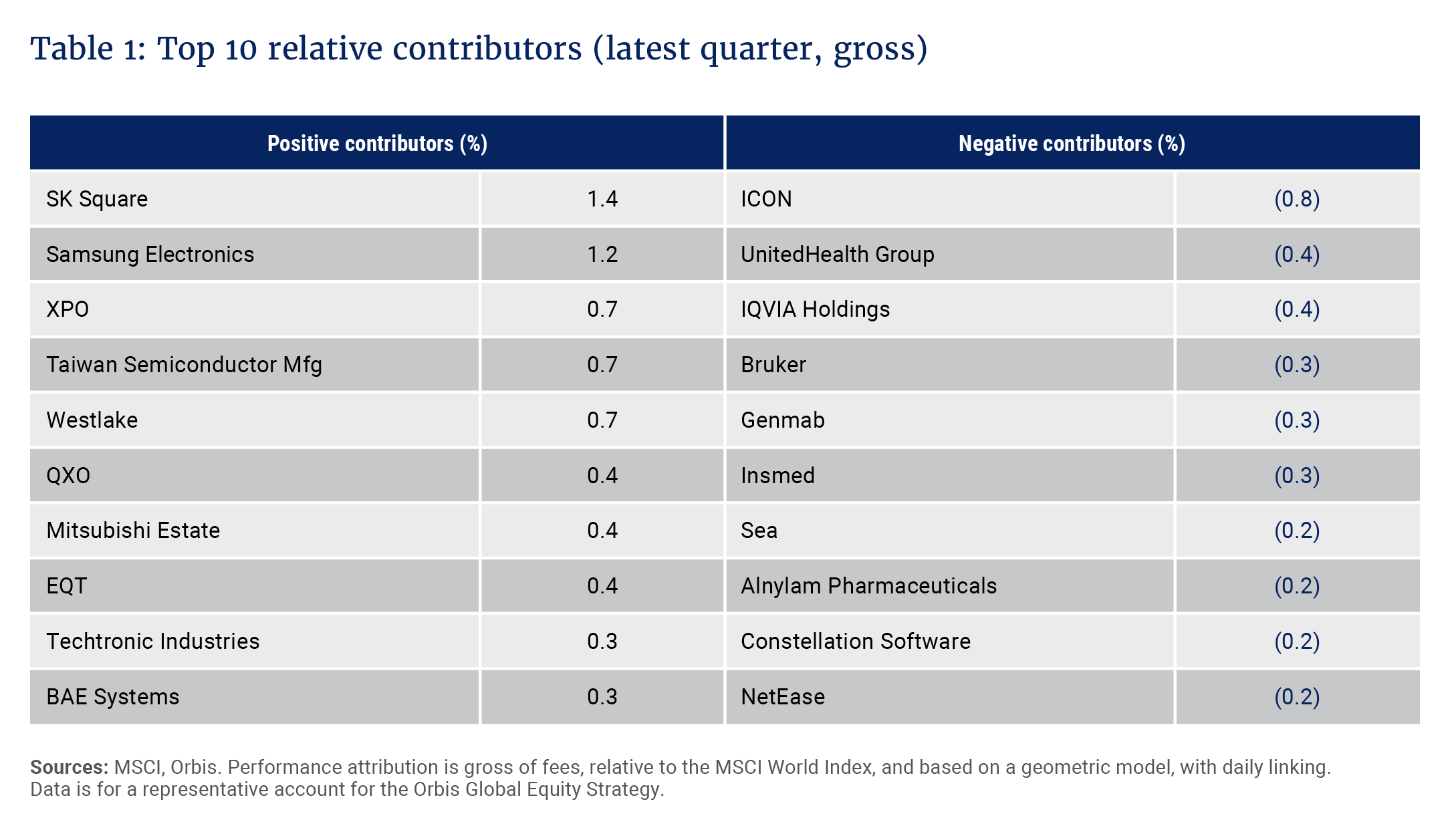

Three of our top winners this quarter were semiconductor manufacturers – “picks and shovels” to the AI boom – while seven of our top losers were healthcare-related companies, as shown in Table 1. Positive skew meant that the outperformance from the semiconductors more than offset the losses on healthcare.

Healthcare

The biggest detractor was ICON, a clinical trial company whose shares fell heavily after reporting financial irregularities related to revenue recognition. With the benefit of hindsight, we would place greater weight on earlier public signals around class actions and management culture. Consistent with our mindset of continuous improvement, we are working on our process for identifying cultural red flags. ICON was sold during the quarter, as was IQVIA, another clinical trial company, which was not implicated in any financial wrongdoing.

US-managed care organisations UnitedHealth and Elevance were detractors for the quarter and have also now been sold. Highly dependent on government-funded programmes, these companies received disappointing news that proposed 2027 reimbursement rates for Medicare Advantage will fall well short of what’s required to keep up with the rising cost of care. At best, this will delay the earnings recovery we had been expecting; at worst, it threatens it altogether if the 2027 rates are a sign of things to come. Our concern is that the US government now seems intent on squeezing healthcare expenditure, and managed care companies are an easy target.

It can be painful to lock in losses by selling underperforming shares, but it’s often the right thing to do. We continually reassess the fair value of the shares we hold, and if the share price no longer stacks up well against the value on offer, we can best serve our clients by dispassionately rotating the capital into more attractive ideas.

Elsewhere in healthcare, we kept positions in biopharma and equipment-makers, where we remain enthusiastic.

Semiconductors

Notwithstanding a recent sell-off in Korean equities, given the country’s reliance on imported energy, our semiconductor holdings have been strong performers for the quarter and, especially, since purchase. During the quarter, we have taken profits on SK Square, a particularly large contributor, and have now raised more in cash from net sales than it cost us to establish the position. Still, it remains a large holding, reflecting what we see as the value on offer.

Aside from the here-and-now of the Iran conflict, the bigger long-term theme that will shape the future of the semiconductor sector is AI. Here, the debate rages on: Is it, or is it not, a bubble?

Broadly, we acknowledge valid points on both sides of that debate. Extraordinary levels of capital expenditure are certainly a concern, particularly when much of it is funded by newly raised capital rather than reinvested profits. On the other hand, it is clear that real intrinsic value is being created. Despite being only a few years old, ChatGPT has already amassed almost a billion regular users worldwide, while Anthropic already has over 500 corporate customers spending at least US$1m per year, and nine over US$100m. Companies do not spend such sums lightly.

All that demand requires vast amounts of computing power – both logic and memory – and there are only a few companies capable of supplying it. The portfolio holds Taiwan Semiconductor Manufacturing Company for the logic, and Samsung Electronics and SK Hynix (held via the deeply discounted holding company SK Square) for the memory. Insatiable demand for more compute has driven earnings to unprecedented cyclical highs. All three stocks have been exceptionally rewarding.

A key question is whether their currently high earnings can be maintained or will fall back as the cycle fades. As usual, we would rather consider both possibilities than pin our hopes on just one, and it’s this exercise that convinces us that the upside/downside skew is still in our favour.

With the shares priced at very reasonable earnings multiples, the stock market is treating the AI boom as a normal (albeit large) semiconductor cycle, signalling that earnings are widely expected to revert to lower levels. Recent breakthroughs in memory compression have fuelled these fears. If earnings do indeed moderate, the shares will likely be weak, but not disastrous – because that bearish outcome is already priced in.

But a far more bullish scenario is also possible, namely that more computing power will improve the capabilities of AI, thus creating more user demand that will, in turn, necessitate more computing power. That dynamic would power a self-perpetuating feedback loop without a natural upper limit, one to be enjoyed by only a small number of companies that have the scale and technical know-how to become critical providers of a revolutionary technology.

We remain confident of the power of our investment philosophy to generate superior returns over time.

Rest of the portfolio

We have also made adjustments elsewhere in the portfolio. We started the year with little to no exposure to software, which has historically been one of the more expensive areas of the market. But when there is widespread fear, such as today’s concerns about disruption, that often plays to our strengths; it creates opportunities to be selective. Not all software business models are the same, so when software shares sold off, we asked a simple question: Will there be fundamental disruption to this business or not? That has guided our focus towards companies with defensive network effects and proprietary data sets – including a new position in the software-enabled credit bureau Experian.

At the same time, we have been looking for opportunities to strengthen the resilience of the portfolio. The conflict in the Middle East has severely constrained the flow of energy out of the Persian Gulf, but initial moves in the share prices of energy producers were relatively muted, indicating that the market expected the disruption to be short-lived.

What if it’s not? We were able to take advantage of the market’s apparent complacency and made some purchases of shares that should give clients increased protection against an adverse scenario, while also being good absolute value even absent an energy crunch. To that end, we have added to the portfolio’s energy exposure through EQT, a natural gas producer in the Appalachian Basin that we believe will benefit from AI-fuelled data centre demand for reliable “behind the meter” power, and Shell, a diversified energy business and keystone global liquefied natural gas producer.

As a reminder, our focus is on long-term returns, and clients should not expect positive relative returns each quarter or each year. Historically, we have outperformed the MSCI World Index in 57% of quarters, 61% of calendar years, 75% of 10-year periods, and 100% of 20-year periods since inception. We remain confident of the power of our investment philosophy to generate superior returns over time.

Explore more insights from our Q1 2026 Quarterly Commentary

- 2026 Q1 Comments from the Chief Operating Officer by Mahesh Cooper

- Investing through disruption: Lessons from history for the age of AI by Nshalati Hlungwane

- Dis-Chem: A great business at a great price? by Jonty Fish

- Pan African Resources: The golden goose? by Andrew Boulton

- Higher discretionary allowance: The opportunity to invest more offshore by Daniel van Andel

- Mind the gap by Horacia Naidoo-McCarthy

- Maximising new tax benefits to boost long-term investment outcomes by Shaun Duddy

To view our latest Quarterly Commentary or browse previous editions, click here.