Investors seeking diversification outside of South Africa can easily overlook the investment opportunities in other African markets. It is tempting to start by jotting down a list of African countries led by despots or with unstable political regimes. Sceptics will point out that Africa remains very reliant on commodities and that the well-told positive themes will take a long time to materialise (think: attractive demographics, ever-emerging middle class). However, the most pertinent consideration is your investment horizon.

Patience is key

The most compelling opportunities in African markets require patient capital deployed in a methodical contrarian approach. Significant valuation discrepancies often emerge during periods of political and economic uncertainty, yielding attractive bargains which are spurned by those with shorter-term expectations. We target longterm absolute returns and strive to earn our investors’ trust so that they will stick with us for long enough to reap the rewards when the tide turns. We have found that this investment philosophy travels well across different African markets and asset classes.

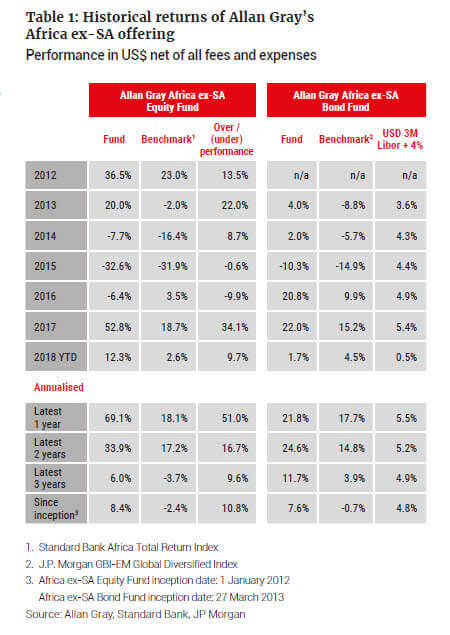

The Allan Gray Africa ex-SA Bond Fund (the Fund) was launched in March 2013, targeting attractive interest-bearing assets in Africa’s public and private debt markets. The Fund invests in corporate and government debt securities, denominated in both local currency and US dollars, and it is open to both individual and institutional investors. Table 1 compares the historical returns of the ex-SA Bond Fund and the Allan Gray Africa ex-SA Equity Fund relative to their respective benchmarks. Over this period, Africa’s debt markets have been less volatile than equity markets and tend to perform well when equities perform poorly.

How we apply our investment approach

A few examples illustrate our investment approach during periods of uncertainty.

African markets performed poorly from mid-2014 to 2015, precipitated by the collapse in oil prices. During this downturn, we invested in corporate US dollar bonds issued by top-tier Nigerian banks at double-digit yields. We also invested in outof- favour corporate bonds issued by oil-related companies such as Tullow and TransGlobe. In all these instances, our focus was on the sustainability of cash flows to service debt obligations and the intrinsic value of underlying assets to mitigate capital loss in the event of default. We have an internal credit risk rating mechanism and our foremost consideration is capital preservation – not prospective returns.

We apply the same framework to government bonds – first evaluating the risk of default, then comparing an appropriate long-term risk premium to prevailing market returns. Attractive opportunities emerge when market expectations are extremely negative, yet a country’s default risk is no worse for long-term investors.

In early 2016, Zambia’s US dollar bond due in 2027 was trading at a low of 66 cents on the dollar and yielding 15.5%. Copper prices had slumped to six-year lows, exacting a heavy toll on Zambia’s currency and the economy – copper accounts for 70% of export earnings and 25-30% of government revenues. The country was experiencing its worst drought in decades, impacting both hydro power generation and agricultural output. Political tensions were high ahead of the August 2016 presidential elections. It was a perfect storm of the most common of Africa’s perceived risks and most short-term investors ran for the exit door. Zambian US dollar bonds have since rallied as the risks dissipated with time. Zambia’s 2027 bond has returned 72% from its low in January 2016 to the end of 2017. This excludes the coupon payments received along the way.

The last two years have resulted in significant gains for investors.Although we are confident of its long term prospects, the Fund is unlikely to sustain this very high level of returns in the future. What investors can expect is that our approach to finding mispriced assets in Africa’s debt markets will not change. Our performance is the result of a simple, consistent focus on two things: the risk of permanent capital loss, and the prospects for long-term returns.