Periods of heightened uncertainty often feel exceptional while we are living through them. But history suggests that markets have consistently rewarded investors who can look beyond prevailing narratives, remain disciplined through volatility and focus on long-term fundamentals. Thandi Skade summarises key investment insights recently presented by portfolio manager Varshan Maharaj at our May 2026 events, “The Times with Allan Gray”.

Markets are constantly shaped by dominant narratives. At different points in history, these have ranged from wars and inflation shocks to financial crises, pandemics and technological disruption. In the present-day context, marked by a sea of dominant trends lifting asset prices, the focus has shifted to artificial intelligence (AI), geopolitics and the broader implications of a rapidly changing global economy.

These narratives matter because they shape how investors perceive risk and opportunity. At times, sentiment can shift far more rapidly than underlying fundamentals, creating meaningful dislocations between price and intrinsic value. For bottom-up, valuation-driven investors, these dislocations can create compelling opportunities.

Rather than attempting to predict every macroeconomic outcome or short-term market movement, we focus on assessing the long-term fundamentals of businesses and identifying opportunities where prevailing sentiment may have distorted asset prices relative to intrinsic value.

Our approach implicitly acknowledges that the future is uncertain. When we assess an investment opportunity, we insist on an adequate margin of safety using conservative assumptions. Even if outcomes prove less favourable than expected, this discipline improves the probability of generating acceptable long-term returns.

When markets price fear over fundamentals

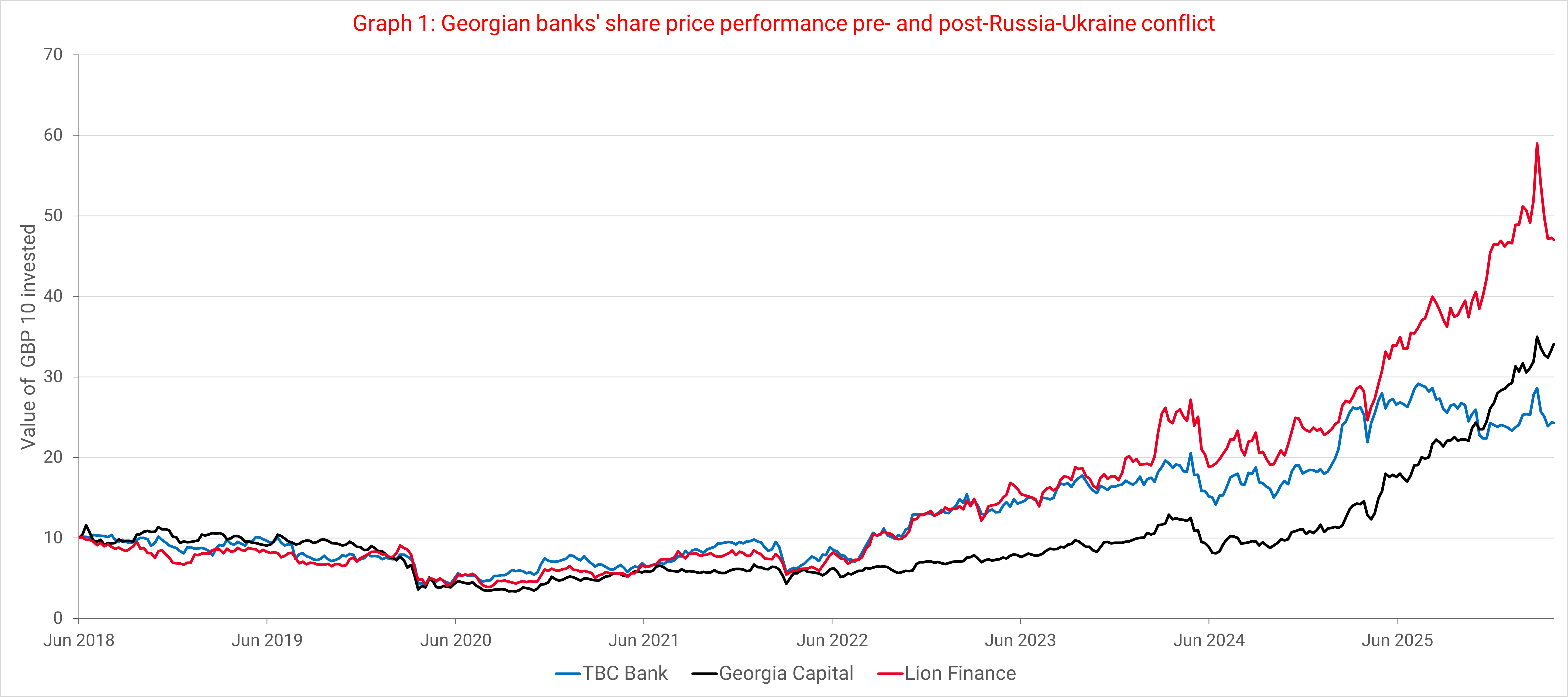

The experience of Georgian banks following Russia’s invasion of Ukraine in 2022 illustrates how quickly market narratives can diverge from fundamentals.

At the time, the prevailing sentiment was that regional instability would escalate and neighbouring economies, such as Georgia, would be directly affected. As a result, shares in Georgian banks sold off sharply as investors reduced exposure to assets perceived as carrying elevated geopolitical risk. At the trough, some of these businesses traded at less than three times earnings, suggesting a material deterioration in their future earnings power.

Graph 1 shows the subsequent performance of three Georgian banks, TBC Bank, Lion Finance and Georgia Capital, held within the Allan Gray Frontier Markets Equity Fund following the invasion.

The sharp initial decline reflects the market’s reaction to the geopolitical shock. However, the trajectory that followed the sell-off illustrates how outcomes can diverge significantly from expectations.

Instead of declining, the Georgian economy strengthened as individuals and businesses relocated from Russia and neighbouring countries. Additionally, it benefited from shifts in regional trade routes, as goods and services were redirected through the country.

These developments led to stronger-than-expected economic growth and, importantly, resulted in significantly higher earnings for the local banking sector. Initially, the market had priced this as a deterioration in fundamentals, but in practice, it proved to be an environment of improving profitability. As the gap between perception and reality narrowed, share prices recovered sharply. From their lows in early 2022 to recent highs, the three holdings saw their share prices increase by five, 10 and 12 times respectively.

The opportunity arose because the dominant narrative, while plausible, proved incomplete. Acting on that insight required a willingness to look beyond prevailing sentiment, assess the underlying fundamentals independently, and remain invested while the narrative still appeared overwhelmingly negative.

Environments like these rarely feel comfortable in real time. Even when a meaningful amount of bad news has been priced in, markets can become more pessimistic before fundamentals assert themselves. This reinforces the importance of valuation discipline, patience and maintaining an appropriate margin of safety in the face of uncertainty.

AI and the danger of pricing perfection

The current AI investment cycle presents a different but equally important challenge for long-term investors. While it is clear that AI has the potential to reshape significant sectors of the global economy over time, its technological importance does not automatically make it an attractive investment.

History shows that periods of significant innovation, from railroads to telecommunications and the early internet, often create substantial value for society, but far less predictable outcomes for the companies involved. In many cases, intense competition, high capital requirements and optimistic expectations mean that much of the economic benefit accrues to users rather than shareholders.

From a valuation perspective, the key question isn’t whether AI matters, but whether current prices already discount outcomes closer to perfection than probability. This matters in an environment where parts of the market appear increasingly willing to pay exceptionally high prices for future growth prospects. For valuation-driven investors, the challenge is distinguishing between businesses with durable long-term earnings potential and those where enthusiasm may have run materially ahead of intrinsic value. At the same time, elevated valuations and market concentration in parts of the global equity market may be creating opportunities in areas where sentiment remains far more subdued.

Building portfolios for a world that is unpredictable

We focus on creating diversified portfolios that can thrive in various scenarios. An example is the Allan Gray Balanced Fund, where the objective is not to maximise returns under one specific outcome, but to build a resilient portfolio that can manage downside risk, while still participating meaningfully in long-term growth opportunities.

This is particularly important in an environment where parts of the market appear increasingly concentrated and expensive. While equities are a key source of long-term growth, maintaining diversification and appropriate downside protection remains essential. Diversification can feel least comfortable when concentrated investments seem to be performing well. However, this is exactly why diversification is so important.

A margin of safety is essential for evaluating individual investments and the prevailing sentiment in portfolio positioning. By insisting on conservative assumptions and avoiding excessive reliance on optimistic outcomes, we seek to reduce the risk of permanent capital loss, while maintaining exposure to attractive long-term opportunities.

This approach also allows us to remain patient and flexible when opportunities emerge. Market dislocations can create opportunities to allocate capital to high-quality businesses and assets at significantly more attractive valuations than would typically be available during periods of optimism.

The difficulty of staying disciplined

To quote author Morgan Housel: “All past declines look like an opportunity. All future declines look like a risk.”

The implication is clear – the moments that look obvious in hindsight rarely feel that way at the time. For valuation-driven investors, the lesson is not simply to stay invested regardless of valuation. It is to remain disciplined when market stress creates better prospective returns, rather than allowing short-term narratives to dictate portfolio decisions.

At Allan Gray, we focus on understanding the long-term fundamentals of businesses and identifying opportunities where market sentiment may have diverged materially from intrinsic value.

Over time, the evidence consistently reinforces a simple point: While uncertainty is ever-present, disciplined investors who focus on fundamentals rather than narratives are more likely to be rewarded.