The prolonged stress of the pandemic has heightened many investors’ focus on the now, interfering with the ability to make sound decisions that improve the potential of achieving long-term personal financial goals and creating generational wealth. This has resulted in a behavioural penalty detracting from returns. It is very hard to remain rational in the face of volatility, but giving in to short-term impulses can be costly. Marise Bester and Daniella Bergman review behaviour and outcomes for the past two years across the broader industry, the Allan Gray Investment Platform and the Allan Gray Balanced Fund with the intention of showing that a longer-term outlook, so-called “cathedral thinking”, can help.

Over the past two years, many of us have fallen into the trap of making decisions aimed at alleviating our short-term worries, which as a result may work against our long-term interests. This is understandable – we have been navigating uncharted waters and operating in survival mode. Even as we begin to emerge from the pandemic, many of us are struggling to think more than five or 10 years ahead, putting our long-term needs and aspirations, including being able to retire and leave a legacy, at risk.

Cathedral thinking … can be used to describe activities that require vision, planning, and long-term commitment

According to behavioural scientists, we have a biological inclination to short-termism – making investing decisions to maximise short-term gains or minimise short-term losses without considering long-term financial consequences. While the mathematical side of our brain analyses risk and reward over time, the emotional side of our brain is activated during real-life risk and reward decisions. This more primitive system, driven by greed and fear, is less concerned with long-term consequences.

Short-termism is also reinforced by today’s 24-hour news cycle, which encourages immediate action, rather than patience. The information that dominates headlines is not designed to appeal to our rational, long-term thought processes, which are essential for investing. It is incredibly difficult to time market peaks and troughs, and investors who try to do this often end up locking in losses and missing out on the subsequent recovery. They also have to work much harder to get their plans back on track. Through this behaviour, many investors lost return value during the COVID-19-inspired crash of 2020.

So why do we behave like this when we know on a rational level that it is value-destructive? One explanation is that because the future is so unpredictable, we feel more secure when we take control of the near term. Added to this, because technology has fractioned time to an unreasonable degree, we have lost our ability to see time in its fullness. We have become used to and expect speed, convenience and instant gratification – including an immediate return on investment.

We perhaps need to take a few lessons from our medieval ancestors who initiated ambitious, carefully considered projects purely for the benefit of future generations. These were often grand buildings that would take hundreds of years to complete, such as cathedrals and community gathering spaces, leading to the coining of the term “cathedral thinking”, which is used today to describe a time frame that considers multiple generations.

Cathedral thinking is the opposite of short-termism. It can be used to describe activities that require vision, planning, and long-term commitment. Investing is a great example – but a look at recent behaviour of local investors shows just how hard it is to apply.

SA investors pick short-termism

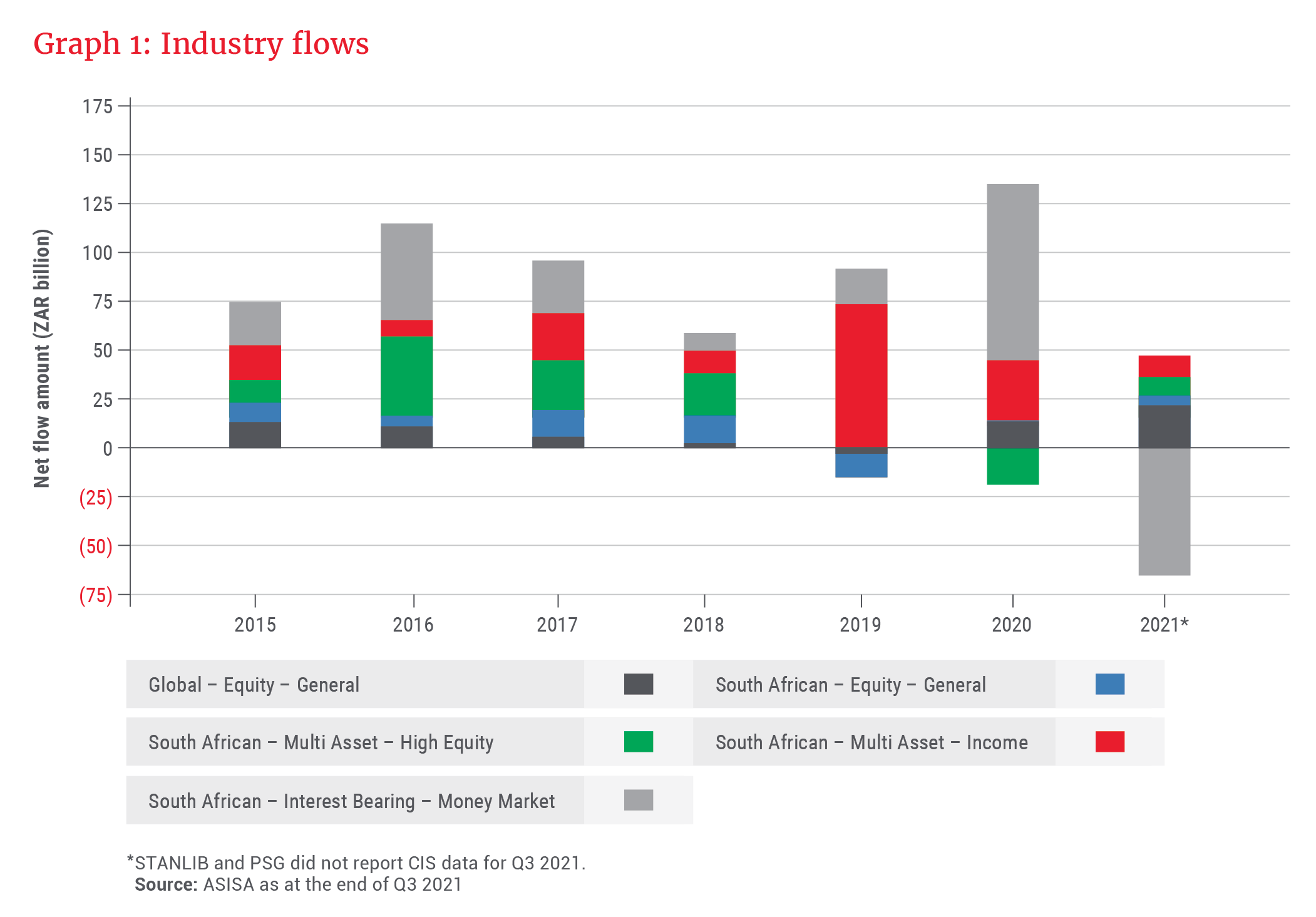

Investment flow statistics from the Association for Savings & Investment South Africa (ASISA), which reveal where investors are placing their money, indicate wide discrepancies across fund categories, as illustrated in Graph 1. These statistics suggest that investors are making decisions based on recent past performance.

In 2019, income funds took the lion’s share of the money, with a flatlining of equities and risk assets as the local equity market had traded sideways since 2014. In 2020, the appeal of interest-bearing assets kicked in, as equities plummeted, and investors hunted for the relative safety of cash. This trend started to reverse at the end of 2020, mostly after the market recovered, with flows draining out of the South African – Interest Bearing – Money Market category and making their way to higher-risk categories in 2021.

The trends described were mirrored on the Allan Gray Investment Platform, with sentiment-based switching decisions impacting investor returns. A look at our client data shows there were net outflows from South African Equity & Multi Asset – High Equity funds across the platform in 2019 and 2020. We believe this was largely influenced by the performance of these categories and the lacklustre performance, in particular from SA equities, in the period running up to 2019. From Q3 2020, the trend started to reverse, with a reasonable increase in flows back into the categories, however, the flows lagged the overall recovery in the market.

Investors who stayed invested in the Allan Gray Balanced Fund over the full two years would have earned a cumulative return of 24.6%. As we discussed in an article in October 2020 (see “Has your risk perception changed as a result of the market crisis?”), an investor who invested in the Balanced Fund in January 2020, switched from this high-equity fund to the Allan Gray Money Market Fund in March 2020 (when the FTSE/JSE All Share Index, or ALSI, was at its lowest) and then reinvested in the Balanced Fund in January 2021, would have earned 6.4% by December 2021. While this is a worst-case scenario, it illustrates how over the last two years, short-term decision-making may have resulted in a hefty behavioural penalty of 18.2% in this case.

Appetite for offshore investing also waxes and wanes, and it is sometimes difficult to pinpoint the drivers. We observed an increase in offshore flows – represented by high-equity offshore feeder funds as well as flows on our offshore platform – from the second quarter of 2020. Flows started to decline around a year later. It is not clear if the interest is structural or cyclical. Over the years we have witnessed increased interest in offshore investing when the rand weakens and/or when the local news flow is particularly negative. However, as we have said many times before, it is counter-intuitive to use a weak rand to buy expensive offshore assets. We encourage investors to utilise offshore exposure wisely and consistently for diversification purposes and not in an attempt to time the market.

How do our portfolio managers apply cathedral thinking?

When investing with the long term in mind, it is critical to pick businesses that will endure. Sustainability is therefore a key part of the Allan Gray investment philosophy. Our investment analysts spend the majority of their time trying to work out the sustainable earnings level of the businesses we analyse. We value businesses based on the sustainable or normal earnings level rather than the earnings at any one point in time. By its nature, this approach considers the long term.

We also consider many other factors when determining the sustainability of a business. These include the level of competition, whether capital is entering or leaving the industry, technological obsolescence, and how the business behaves regarding environmental, social and governance (ESG) considerations. Some may consider ESG factors as separate from the investment process, but for us they are integral. If a business does not operate in a sustainable manner, it may find itself in a position where it is unable to operate profitably.

When it comes to constructing portfolios, our investment team carefully considers which assets they believe are priced below their true value and likely to deliver returns over the long term. Sometimes an idea can take years to play out, and it is important that portfolio managers have high conviction so that they can hold firm in the face of short-term market movements that may be contrary to a longer-term thesis.

Allan Gray’s philosophy is to not take a top-down view of where markets are heading, but rather conduct bottom-up research on individual companies. As we have discussed previously, prior to the onset of COVID-19, our equity portfolios were positioned to take advantage of what we believed were undervalued South African shares. COVID-19 hit, and many of these shares fell further. But as things stabilised, many of these share prices rose. We would have missed out on the correction if we had irrationally responded to the dip; instead, we benefited from adding assets we regarded as cheap. As always, it is a question of price: How much am I paying? How large is my margin of safety? And to what degree am I being compensated for the downside risks?

Our approach currently reveals more than enough attractive opportunities, which makes us cautiously optimistic about medium-term returns. Of course, there are many risks from the global and SA macroeconomic environments. One such an example is the overvaluation of the US market and how local assets would perform in a scenario where that overvaluation suddenly corrected. These risks are balanced by the low prices at which many businesses are trading: Locally, overall valuation levels are not high compared to history and we continue to find value in both local equities and bonds.

We are also cognisant of the environment in which we invest so that we can be on the right side of long-term trends, which is why we position our funds to perform well in a variety of scenarios. An example of this is the changing inflationary environment. We continue to tilt our portfolios to protect against the increased probability of higher inflation through exposure to precious metal exchange-traded funds (ETFs) and increased positions in gold-mining companies. A higher inflation and interest rate world should favour SA equities, which are more value-like in nature compared to the large growth technology shares, which dominate the US market.

Cathedral thinking on an individual level

Equity market collapses, such as what we experienced during the early stages of the pandemic, are often relatively short when considering a multidecade investment journey. However, making permanent decisions based on temporary emotions, either because of fear of loss or fear of missing out, has very real consequences over time.

But in an environment in which the default setting is living for the now, applying cathedral thinking is tough. It takes a considered shift in how we view the world, with an emphasis on the future. There are some inspiring examples of projects underway that exemplify this approach. One is the Svalbard Global Seed Vault, a safety deposit of millions of seeds on a Norwegian island in the Arctic Circle, designed to preserve the world’s crop diversity for future generations.

The question is: How can we apply this in our own investment journey?

One factor that ensures we focus on the long term is our attitude toward risk. To achieve real returns, we need to take on some risk, which introduces volatility. Over a short period of time, there could be a large variance in return, which can lead to discomfort, as we have experienced recently. However, volatility should smooth out over time. Labourers who worked on cathedrals encountered many setbacks, yet they persevered.

making permanent decisions based on temporary emotions … has very real consequences over time

Neha Aggarwal, a member of Orbis’ European investment team, phrased it very well in her recent video, “Taming turbulence”. She says that the longer your time horizon, the more the impact of volatility and the probability of an extreme outcome diminish. She aptly notes that an hour of turbulence would define the comfort of a flight between London and Paris, for example, but is much less of an issue if you’re on your way to Australia.

We have recently written about forming a picture in your mind about your future self in a bid to relate more to the person you are investing for, to make saving for retirement less painful. In his book The Good Ancestor: How to Think Long Term in a Short-Term World, Australian-born writer and philosopher Roman Krznaric takes this a step further. He describes the “grandmother effect” – a concept from evolutionary psychology that relates to the way we as human beings are situated in multigenerational groups: A child has parents and grandparents. When that child grows up, they may have their own children and grandchildren, and so on.

Our investment goals may be more easily achieved if they are deeply rooted in a purpose

Krznaric encourages us to push our thinking of the future beyond our future self, to imagine our children’s ageing children, and focus on their potential needs. This should give us a sense of how to apply this cathedral thinking concept to our investments: to be focused on leaving a legacy for generations to come. Our investment goals may be more easily achieved if they are deeply rooted in a purpose.