At a recent investment update via Zoom webinar, Matthew Spencer and Stanley Lu, from our offshore partner, Orbis, reviewed the Orbis Global Equity Fund’s recent performance and discussed the pockets of value they are finding in global markets, with a specific focus on the investment landscape in China and emerging markets – key areas of interest for investors. Watch the 42-minute recording or read a summary of the key takeaways below. You can download the presentation slides here.

Performance highlights of the last 18 months

COVID-19 first appeared in November 2019, and since then, market fluctuations and share price decreases have followed COVID-19 cases and lockdowns. The Orbis Global Equity Fund has not been spared in the process. To follow the impact of COVID-19 on markets and the Fund, it helps to break the past 18 months into three distinct periods.

1 January 2020 – 31 March 2020

While COVID-19 first appeared in November 2019, the market broadly shrugged it off as just China’s problem. It wasn’t until February 2020, when the virus took root in the US, that the market responded to the situation. When the seriousness of COVID-19 became clear, the value of world stock markets decreased by 34% in less than a month. Value-oriented stocks were hit harder, with their prices crashing 38% over the same period while the prices of growth-oriented stocks fell 31%.

During this period, the share price of the Orbis Global Equity Fund fell too, but it fared no worse than the market, despite having a greater exposure to value-oriented stocks. This was largely a result of the portfolio’s 20% exposure to Chinese internet stocks, which the market correctly viewed as COVID-19 beneficiaries.

All market dips provide investors with opportunities and this one was no different. Accordingly, we sold some of our stocks with exposure to China which had provided a buffer during the initial crash and added to companies we felt were being unduly penalised as a result of the pandemic. The companies that we bought during this time broadly fell into two main “buckets” – 1) companies that had superior fundamentals than their peers, but which had fallen as much as if not more than the market, and 2) resilient cyclicals, which are economically sensitive companies that had stronger balance sheets than their peers, which meant they had time on their side should the recovery take longer than expected.

1 April 2020 – 31 May 2021

During this period, stock markets bounced back considerably, driven largely by vaccine news and the prospect of the world returning to “normal” sooner than expected. The Orbis Global Equity Fund outperformed the market during this period with many of the positions that we added to during the initial drawdown being some of the top contributors, validating our course of action in the aftermath of the initial market crash.

1 June 2021 – 30 September 2021

However, in the last four months, the Orbis Global Equity Fund has underperformed the market by 4%. There were two reasons for this – 1) the COVID-19 Delta variant caused markets to stall, especially value-oriented stocks, which the Fund was overweight, and 2) the Fund’s exposure to Chinese internet stocks. Normally in such an environment these stocks would outperform, but due to the Chinese government passing a number of regulations which affected the internet landscape, they significantly underperformed. In hindsight, we should have reduced the Fund’s exposure to China by more than we did following the initial outperformance in the aftermath of the COVID-19 crash.

Navigating the risks and rewards of Chinese stocks

Broadly speaking, companies in China typically fall into one of three buckets:

- State-owned entities

- Entities that are not state owned but cause us some concern due to poor governance or management

- Privately founded/owned businesses

Despite some bouts of volatility, the last group has been a healthy source of idiosyncratic alpha for the Orbis funds over our history. We have long been mindful of “China risk”, and in some ways, the regulatory changes in the last few months have not come as a surprise.

The regulatory changes over the past year have been a result of a combination of a move by the Chinese government to implement more robust, antitrust regulation and to increase protection for Chinese consumers and families. While the regulatory changes have not been surprising, their severity and the abrupt way they were announced have led us to conclude that regulatory risks are now higher than before.

So, while it is fair to say that the prices of our Chinese internet stocks have decreased more than the intrinsic value of the companies have been impaired, we have not added to the positions.

Current alpha opportunity

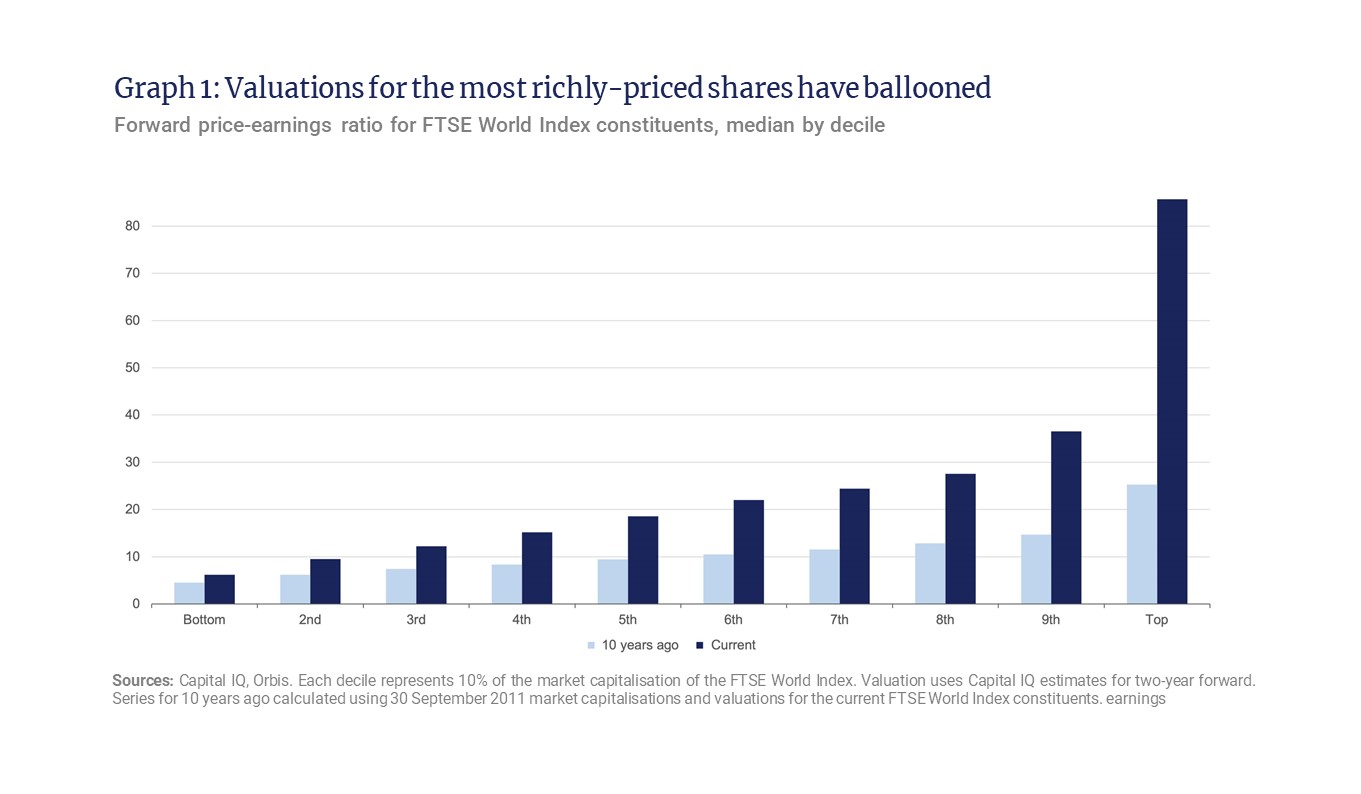

Any way you look at the data, global stock markets are expensive in aggregate. While we agree with this, there is a wide dispersion in valuations, meaning the expensive part of the market is pulling the average up. But if you have the time and resources to sift through the opportunity set, there are still bargains to be found in the cheaper and middle part of the market as illustrated in Graph 1 below.

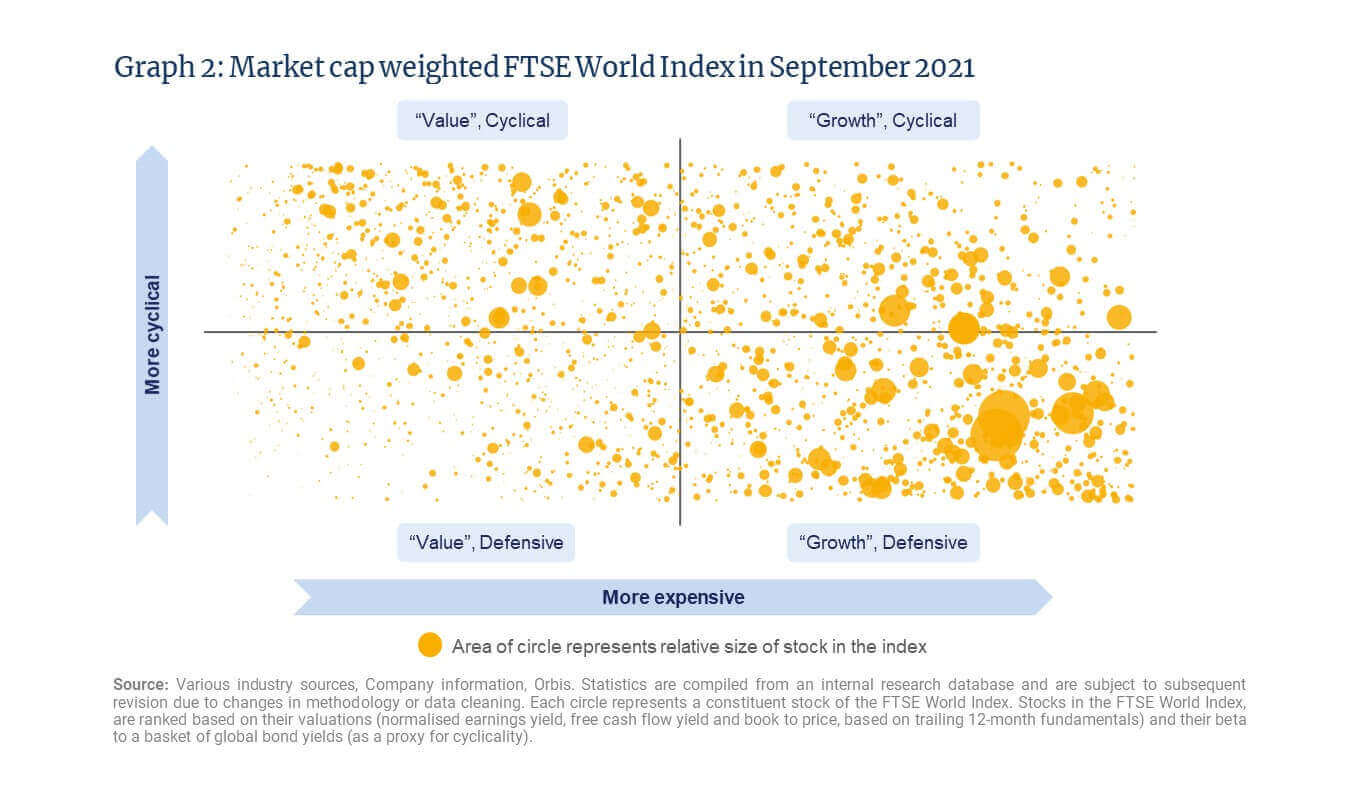

If you represented all the 3 100 companies in the FTSE World Index by a yellow dot and ranked them by two criteria – 1) expensiveness and 2) economic sensitivity; you would get the four quadrants below (see Graph 2). After adjusting the size of each dot to reflect the size of the company’s market capitalisation, it is interesting to see how the world’s capital has congregated in the bottom right-hand quadrant (“growth” defensives) which are largely US mega-tech companies.

Why has this happened? Because the last decade has been the perfect environment for growth-oriented stocks. The combination of limited economic growth and central bank intervention to keep interest rates low has been a tailwind for these stocks. The icing on the cake was the COVID-19 pandemic, which saw many of these stocks benefit from prolonged lockdowns and the stimulus in the US, much of which was sent directly to individuals in the form of stimulus cheques who then invested in the stock markets, favouring these large tech companies.

We aren't making predictions about the future, but we must acknowledge how good the broader environment has been for growth-oriented stocks and how different today's starting point is from that of 10 years ago, making it less likely that their performance over the next decade will be a repeat of the previous one.

If you perform the same exercise for the Orbis Global Equity Fund, you will notice that its holdings (represented by the blue dots in Graph 3 below) are more evenly dispersed across the quadrants. We are staying away from the expensive part of the market and are excited about the idiosyncratic opportunities we are finding, including value companies in Japan (especially the Japan trading companies), value stocks in Europe, companies in "the boring middle" in the US and selected shares in emerging markets (including China).

When compared to the averages of their World Index peers, the companies held in the Orbis Global Equity Fund are growing faster and yet trade at significantly lower valuations.

Importantly, from a fundamental perspective, these businesses are completely uncorrelated and we are optimistic about what this means for the portfolio’s performance over the long term.