Uncertainty abounds at present. Equity returns for the past few years have been underwhelming, political upheaval locally and internationally is causing waves, and there seems to simply be no sure bet. So what should investors do? Andrew Lapping takes a look at the context in which we must invest, explains why he believes that uncertainty presents opportunity and reminds us of the essence of the Allan Gray investment philosophy: valuations matter.

Understand the South African context

South Africa and the UK have roughly the same number of people – in the region of 60 million. The key difference is the number of employed individuals – over 30 million are in formal jobs in the UK versus around 10.4 million in South Africa. Most of those formally employed in the UK pay tax. Not so in SA, where this is true for only around 4.5 million individuals, according to SARS, and close to 75% of the personal income tax is collected from just 1 million people. This narrow base makes increasing tax revenue difficult and illustrates the challenges the government faces in providing services to 59 million South Africans. The budget deficit of 4.5% of GDP may not sound that bad. However, if you think of the government as a company, and look at the government expenses, including SOEs' funding requirements, compared to government revenue, you are left with an operating margin of minus 24%. The government is spending 24% more than the revenue received. Put differently, for every R100 the government receives, it spends R124.

It is very difficult to manage this imbalance. The tools in the government’s kit include reducing spending – which is not popular, and given the dire need of many South Africans probably not a good idea, or increasing tax collection, which is also not a great solution. The “Laffer” curve suggests that you can only increase taxes so much before collections start to fall – i.e. you get to a point where tax payers get fed up and start looking for ways to avoid paying. In addition, demand for goods and services falls as tax rates rise.

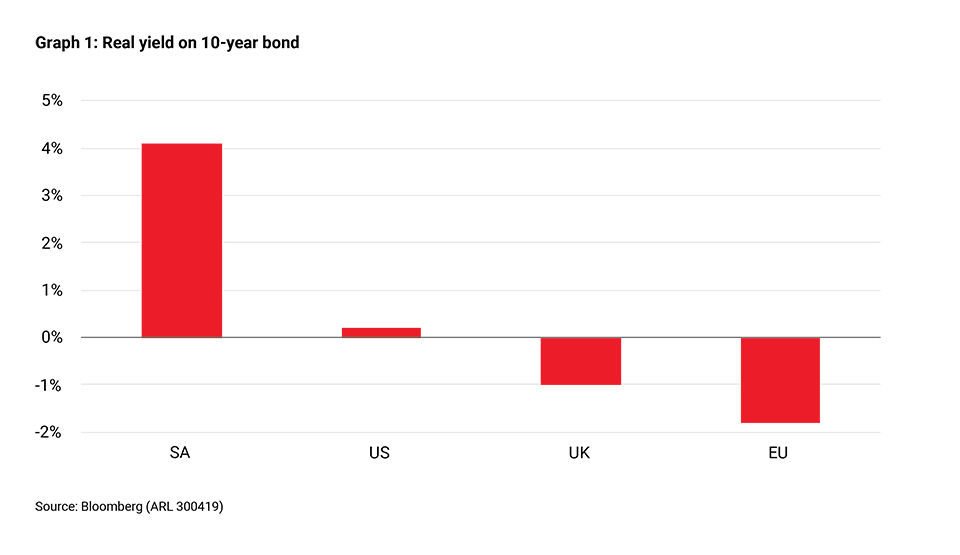

Funding this government deficit, which is linked to the current account deficit, needs to come from investors. If foreign investors don’t continue to fund the deficit the rand will weaken. Luckily, global investors are attracted to the high real interest rates offered in South Africa – unusual in a global context, as shown in Graph 1. Savers in Europe are experiencing negative real interest rates, which effectively means they are losing money by keeping their money in the bank or buying government bonds. This is why they are attracted to South Africa.

So, should all my money be in South Africa?

While putting your money in the South African money market means you can benefit from decent interest rates, historically cash investments have not been the best way to protect and grow the purchasing power of your money and the future may take a path where cash assets do a poor job of protecting your money. For this reason diversification is key.

The trade deficit has narrowed, because of weak domestic demand and terms of trade moving in our favour. We think the rand is currently at about fair value. But if investor sentiment changes for the worse, the rand may depreciate sharply. Issues that may change investor thinking towards South Africa could be a lack of reform or an Eskom funding crisis. Events in Argentina have illustrated that political and economic concerns can batter an emerging market currency, with the peso sliding from ARS15 to around ARS45/US$ over the last two years.

Contrarian: Be cautious when things are great

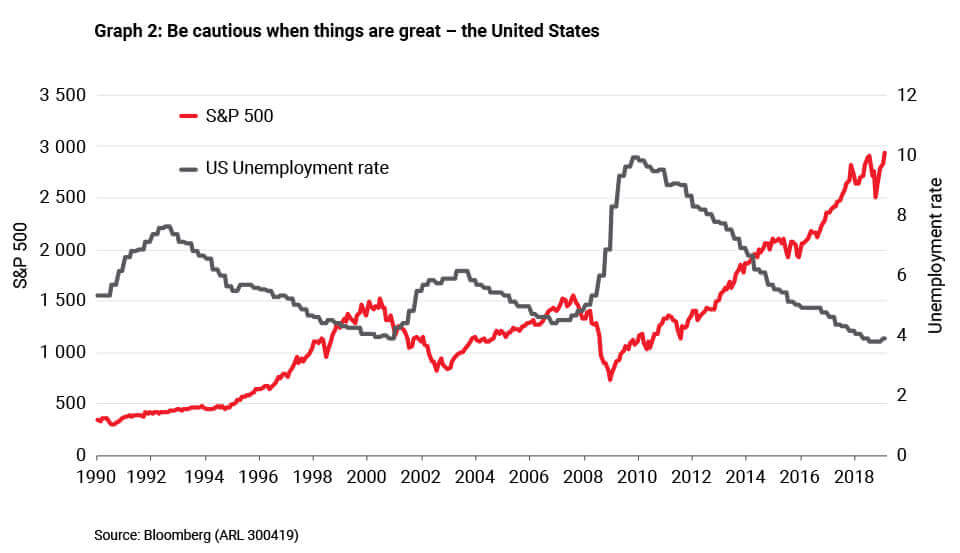

Being contrarian is not just about taking a different view for the sake of it; it is about seeing opportunity when others can't see beyond the negative. It is about leaning against the crowd. Consider US market returns and unemployment rates, as shown in Graph 2. When unemployment has peaked in the US and the country has been in recession, investors have tended to flee from the market. They are forecasting the future based on these negative factors. While it can be hard to see beyond the negativity, it in fact presents great opportunity for future returns. The converse is also true: When the economy is booming and employment is full, investors discount this state of affairs into stock prices, as was the case in 2000, 2007 and possibly 2018.

What is the potential for local returns for the foreseeable future?

Stock market returns are driven by three factors:

- Earnings growth

- Dividends

- Re-rating

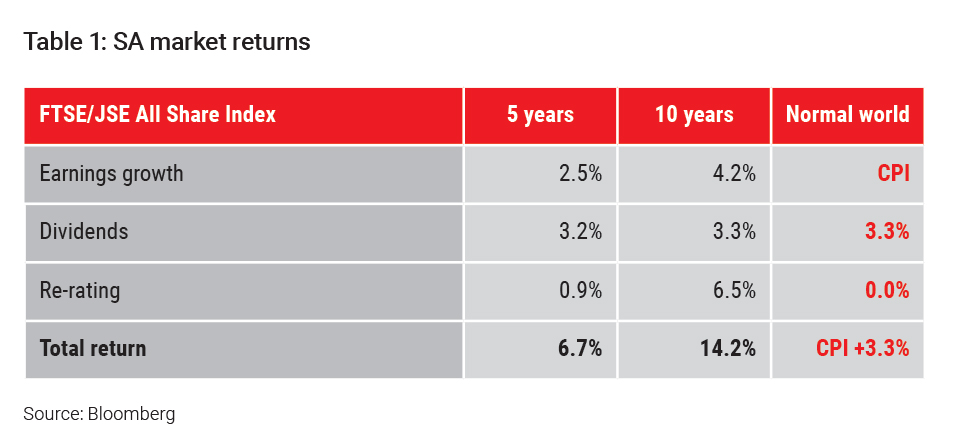

Over the last 10 years earnings growth has been below inflation. However with a 3.3% dividend yield and a strong re-rating from the depths of the financial crisis, returns have been in the region of 14%, as shown in Table 1. But this level of re-rating is not likely to be repeated, and we need think about how we would define “normal” levels by looking at the average over a longer period of time. Over the last 50 years the average JSE listed company grew earnings at 2.3% above inflation, with some companies experiencing unusually high levels of growth due to limited foreign competition. More recently competition has intensified, and the share of the pie going to management has increased drastically, putting a drag on returns. Real earnings growth from here is likely to be closer to inflation or a little above, which is more in line with global norms. Long-term market return expectations could be closer to inflation plus 3.5%.

We aim to deliver real returns in excess of the market through superior stock selection. There is some value out there – you just need to look carefully to find it.

Allan Gray Balanced Fund performance attribution

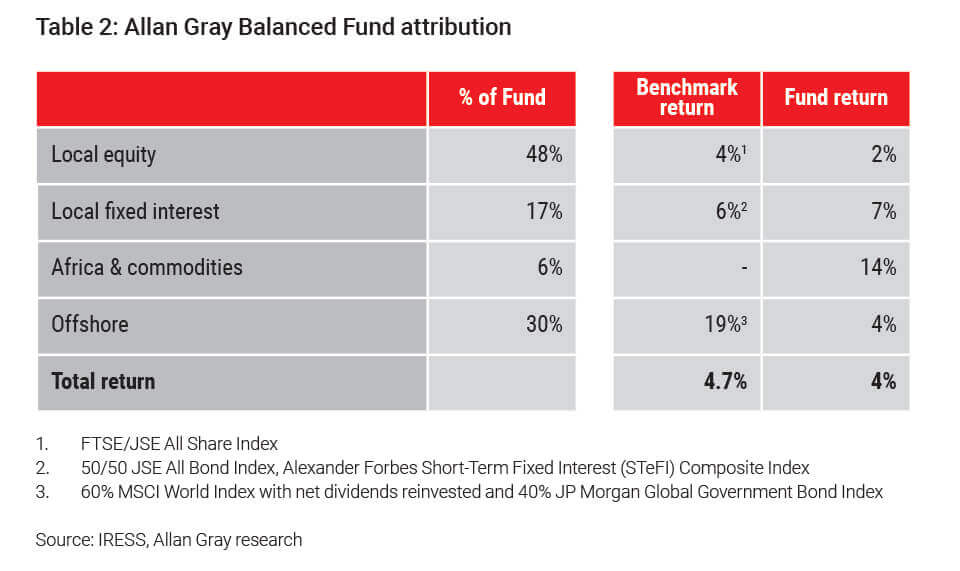

To get a sense of how the Balanced Fund has performed over the past 12 months (to end April) one can look at the different components compared to their benchmarks or the index. The asset classes that contributed positively were the African assets and the fixed interest holdings, while the offshore component managed by Orbis was the main relative detractor, as shown in Table 2. Orbis, like Allan Gray, is a contrarian value manager, which means that short-term performance is often volatile. The Orbis holding could well be the biggest contributor in the next 12 months.

Drilling down into the share component, Naspers, Sasol and Impala all contributed positively to the Fund’s performance, while British American Tobacco, Woolworths and Remgro detracted. While the detractors weighed on performance, their underperformance provided a further buying opportunity.

Of course what we don’t own also has a bearing on relative performance: We missed out by not owning BHP Billiton and Anglo, which did unexpectedly well thanks to the 50% increase in the iron ore price on the back of the Brazilian Vale dam disaster. However, while the share prices of these companies have gone up, the underlying value has not increased to the same degree, in our view.

The absolute return mindset: Allan Gray Stable Fund

The Allan Gray Stable Fund is suitable for clients who have a long time horizon but want to avoid excessive volatility. The Fund aims to provide a high degree of capital stability and to minimise the risk of loss over any two-year period, while producing long-term returns that are superior to bank deposits. Every asset included in the Stable Fund is hand-picked and examined for its return potential and potential drawdown. Every asset is compared to cash and the risk/reward profile is examined. The key questions we ask are: 1) How much is the asset likely to return compared to cash? and 2) How volatile is the return likely to be?

Nerves of steel

When assessing an asset it is important to look at the long-term outlook when determining the normal earnings. Steel consumption and iron ore are a case in point. Chinese steel consumption has followed a very similar trend to that of Japan in the post-World War II era of rapid economic development, where demand grew rapidly to 1972 before plateauing. Looking at Japan’s stable steel demand, the natural assumption is that iron ore demand is also stable. However, this does not consider recycling. While demand for steel in Japan has remained stable the demand for iron ore has slowed drastically as the vast majority of steel is now sourced from recycled material rather than iron ore. If China follows a similar path, as we expect it will, the long-term outlook for iron ore will not be as good, as an ever-increasing share of Chinese steel demand is sourced from recycled material. This is just one factor that informs our view of the long-term iron ore price, which is a crucial assumption when valuing BHP or Anglo American.

The investment case for Glencore

Glencore’s lack of exposure to iron ore is one of the factors that attracts us to the company and makes it our preferred commodity investment. But it is not a company without controversy.

What we like about the share is that management owns 20% of the company, and is therefore aligned with other shareholders. Glencore is highly cash flow generative and management is applying the cash wisely to pay down debt, buy back shares and pay a very healthy dividend. On the negative side, the company has been impacted by the Chinese commodity cycle and trade concerns, it operates in the DRC and Zambia, which are very difficult jurisdictions, and it is under investigation by the US Department of Justice (DoJ). The biggest concern is the DoJ and related investigations. In our view, management is doing the right thing and has changed its policies and procedures to avoid a recurrence of the transactions that led to the DoJ investigation.

Whenever we invest we weigh up the risks and the potential rewards. In the case of Glencore we think the market has overreacted to the risks and this has given us the opportunity to buy the company at a substantial discount to fair value.

The price you pay counts

At the end of the day, it is important to have a consistent strategy and stick to it through the cycle. We are a contrarian value manager. For us the valuation is key and we constantly strive to find assets trading at a discount to their underlying value that will allow our investors to reap superior returns.