As we celebrate our 50th anniversary, we are mindful of the collective efforts of teams, past and present, in building our long-term track record. Fascinatingly, achieving a long-term track record in investing has much in common with achieving success in professional tennis. In comparing the two disciplines, Radhesen Naidoo was excited to discover how meaningful a difference of 1% is to long-term success. Naidoo serves up some thought-provoking takeaways.

In 2022, all-time tennis great Roger Federer laid down his racquet, sending shockwaves through his fanbase. For over 20 years, this precision shotmaker redefined the game for generations to come. As investment managers, we are intrigued by stories hidden in data; it was therefore serendipitous to find a connection to investment management when crunching the numbers and underlying data of Federer’s success on the tennis court.

Sport analogies are powerful in understanding what is needed to achieve success. Professional tennis and investment management both require a long-term mindset. Both disciplines are about patience, hard work and commitment to hone your skill, as well as resisting the urge to make rash decisions.

In tennis, a match may last for two to three hours, and a tournament lasts for two weeks, but a career, multiple years. To play exceptionally well consistently is difficult. Similarly, many investment managers may achieve stellar investment returns over one quarter or a year, but over decades and through different market cycles, outperformance becomes challenging. Adhering to a tried-and-tested investment philosophy is key, as is being adaptable, as the investment environment is constantly evolving. Likewise, in tennis, professional players use strategies that enhance their strengths, but as their opponents and the playing conditions change, these need to be tweaked to win.

As an active investment manager, we recognise the compounding power of doing even slightly better than the market over time …

While these concepts are shared by multiple disciplines, an interesting aspect about professional sport is the margins by which you win. Being marginally better can translate into substantial advantages – and is particularly relevant when thinking about what we aim to do as investment managers.

What is the difference between a good and a great tennis player?

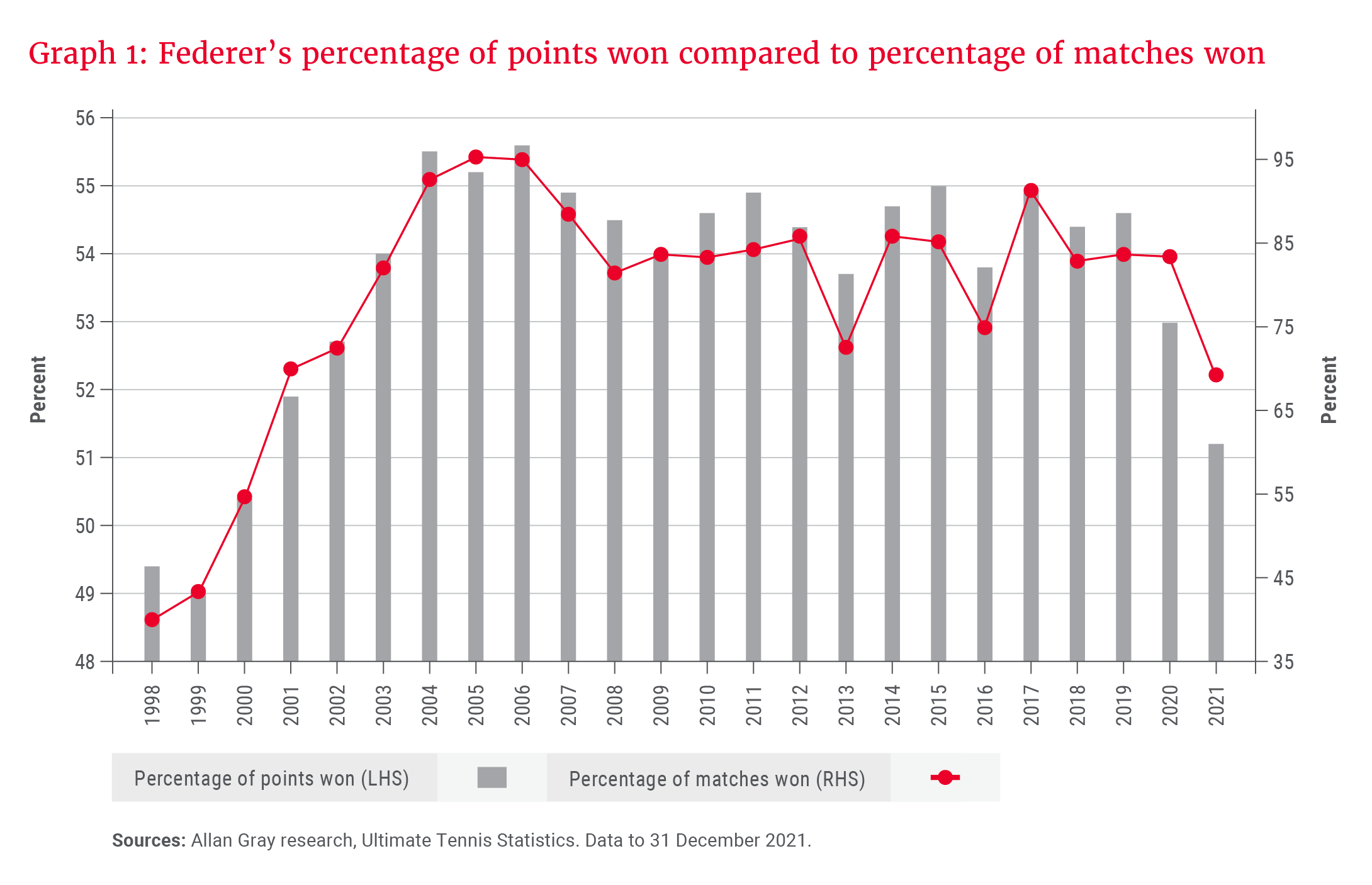

There are numerous data points available for professional tennis players, but one that stands out and is easy to interpret is the percentage of points won compared to the percentage of matches won. Graph 1 plots this data for each calendar year that Federer played professional tennis – from 1998 until 2021. The results are rather striking.

In 1999, Federer started the year ranked outside the top 100. He won 49% of all points played, and 43% of all his matches in that year. During 2001, he was in the top 50 ranked players, winning 52% of all points, and 70% of his matches. In 2005, when he was world number one and dominated the game, he won an incredible 95% of his matches. However, surprisingly, he won only 55% of all points played. Put differently, he was still losing 45% of the points played – but the marginal change in points won had an exponential impact on the number of matches won. What is more remarkable is that he continued to play at this level for the rest of his career, highlighting his ability to consistently improve his game as the competition grew.

… staying the course to realise the longer-term returns means not getting distracted by the short-term noise …

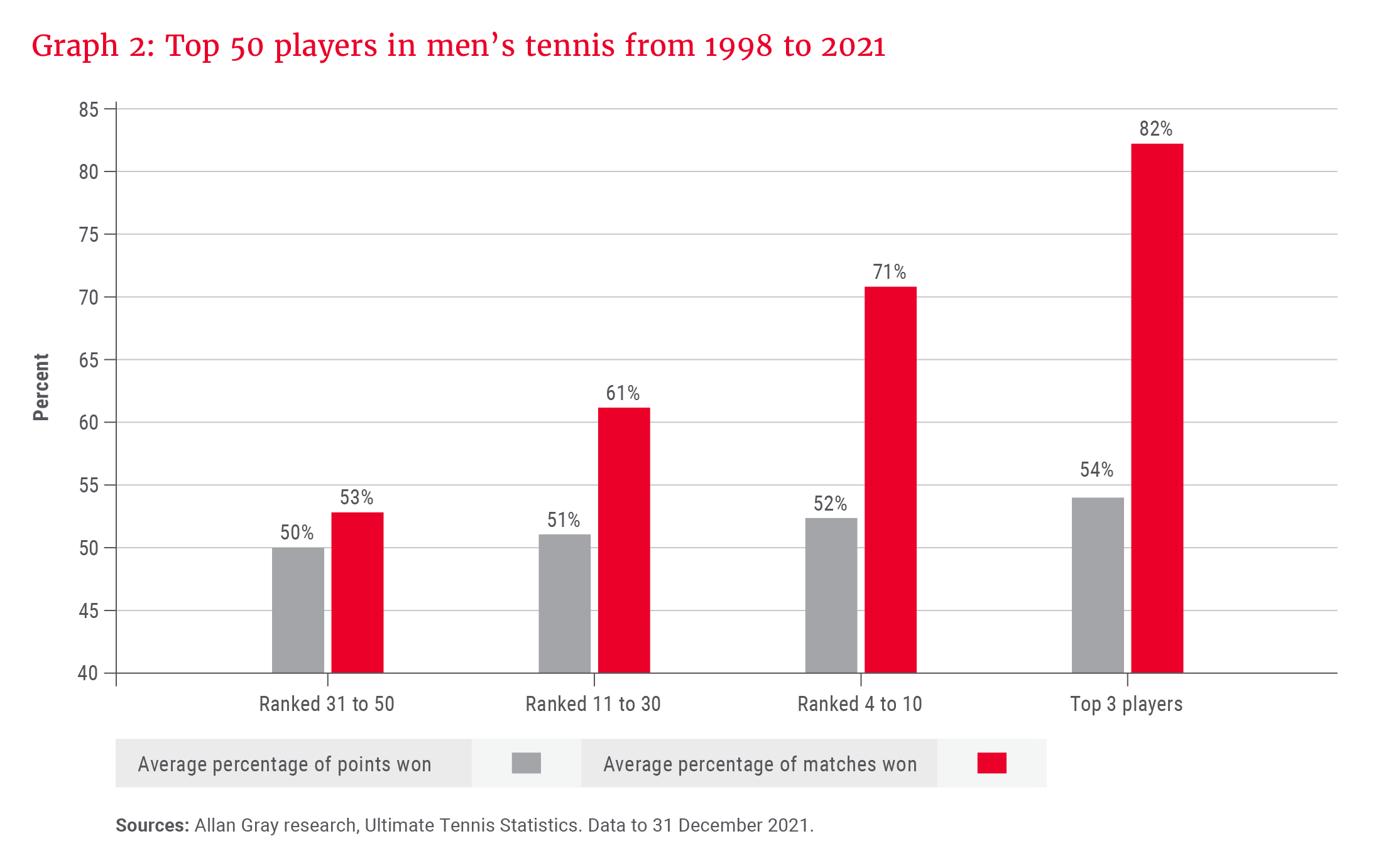

The same data for the top 50 men’s tennis players in the world each year from 1998 to 2021 presents a similar pattern. We divided the players into four groups based on their ranking: the top three players given the success of Federer, Rafael Nadal and Novak Djokovic over the period, the next seven best players (ranked 4-10), the next 20 (ranked 11-30), and the bottom 20 players (ranked 31-50). Graph 2 plots the average percentage of points won against the average percentage of matches won for each group over the 24-year period. The results are similar – winning more points generally means winning more matches.

However, look closely and you will notice that while each group improved their points won by roughly 1-2%, the matches won increased by about 10%. The players ranked 31-50 won 50% of their points but only 53% of their matches, while the top three players won just 54% of their points, but over 80% of their matches. We could therefore say it is merely 1% that separates the good from the great in professional tennis. However, it could be more apt to conclude that achieving and maintaining that 1% gap over your peers – which requires tremendous skill and effort – is the mark of a champion.

1% differences matter over the long term

There are several conclusions one can draw when pitting this analysis against investment management. Let’s start with the idea of the 1% difference, or what we will refer to as “marginal improvement”.

At Allan Gray and Orbis, while our investment philosophy has remained the same since inception, our investment process has evolved. Our aim is to be marginally better each day in our efforts to deliver long-term outperformance. This could involve reflecting on past decisions, investing in better technology, drawing on different research – there isn’t a silver bullet to success in this regard. As an active investment manager, we recognise the compounding power of doing even slightly better than the market over time and therefore continuously interrogate where we can make subtle adjustments to gain a slight edge. This matters a great deal to long-term outcomes.

… every 1% return we can add makes a meaningful difference to the long-term rand outcomes that our clients experience.

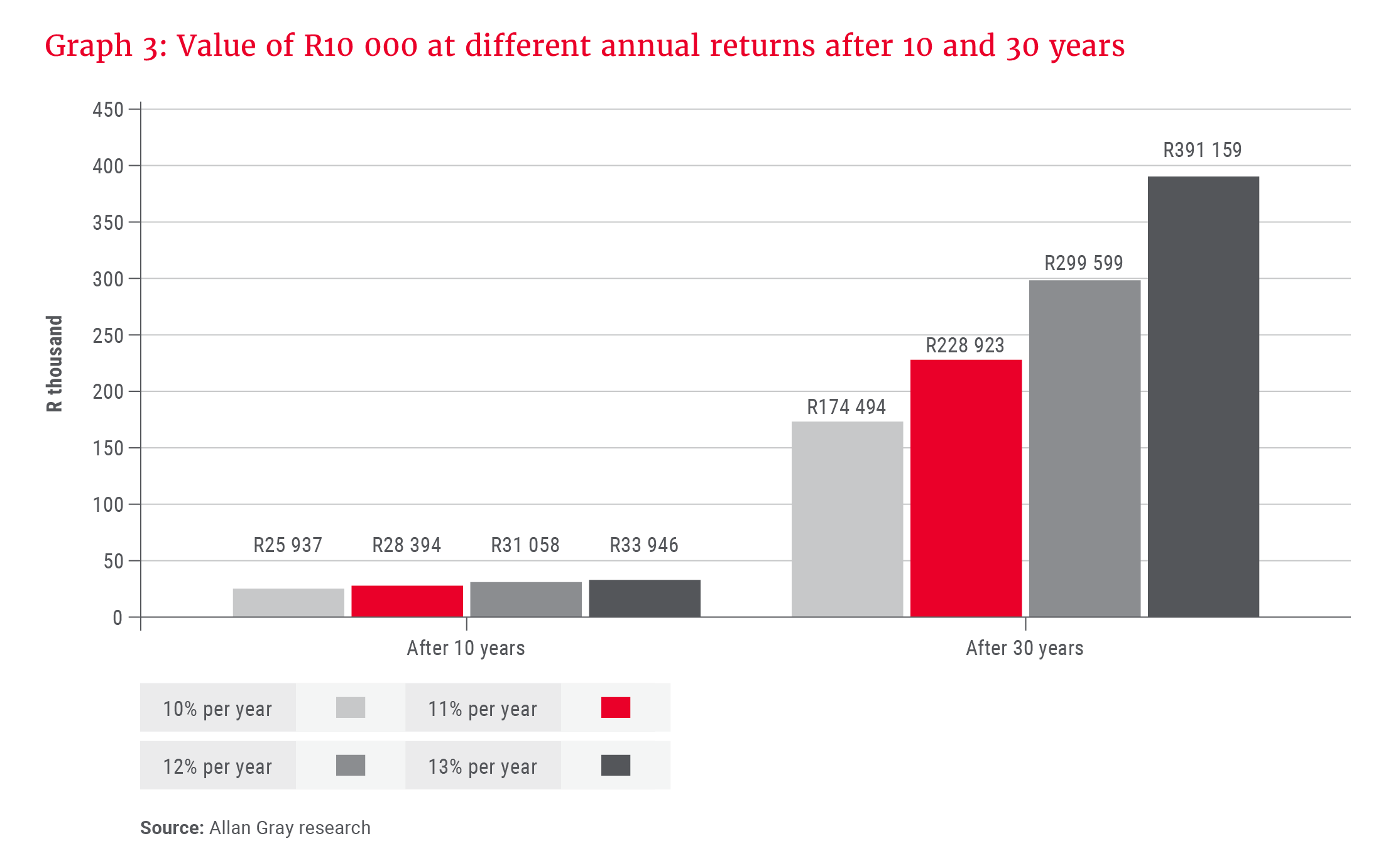

The 1% difference is more simply illustrated with a practical example. Assume you invest R10 000 in a fund and expect an average return of 10% per year. Over the next 10 years, achieving this outcome would mean your money has more than doubled to R25 937. However, if the fund delivered 11% per year rather than 10%, the investment would be worth R28 394, or about 10% more. After 30 years, the difference in outcomes is more pronounced because of compounding, and you would have about 30% more, as shown in Graph 3.

As an investment manager who aims to outperform our peers and benchmarks, it is rewarding – and humbling – to recognise that every 1% return we can add makes a meaningful difference to the long-term rand outcomes that our clients experience.

Picking your moments; you don’t need to get every decision correct

We often say to our clients that achieving a long-term track record does not mean getting every decision correct. What is interesting, though, is that our success rate in choosing shares that outperform is roughly comparable to the percentage of points won by the top tennis players. As shown in Graph 2, the top three tennis players won about 54% of their points – which also means they were still losing 46% of their points. In tennis, a match is often decided by a few key points, and the top players succeed by investing their energy in those decisive moments, reducing unforced errors, and not getting distracted by mistakes when they happen.

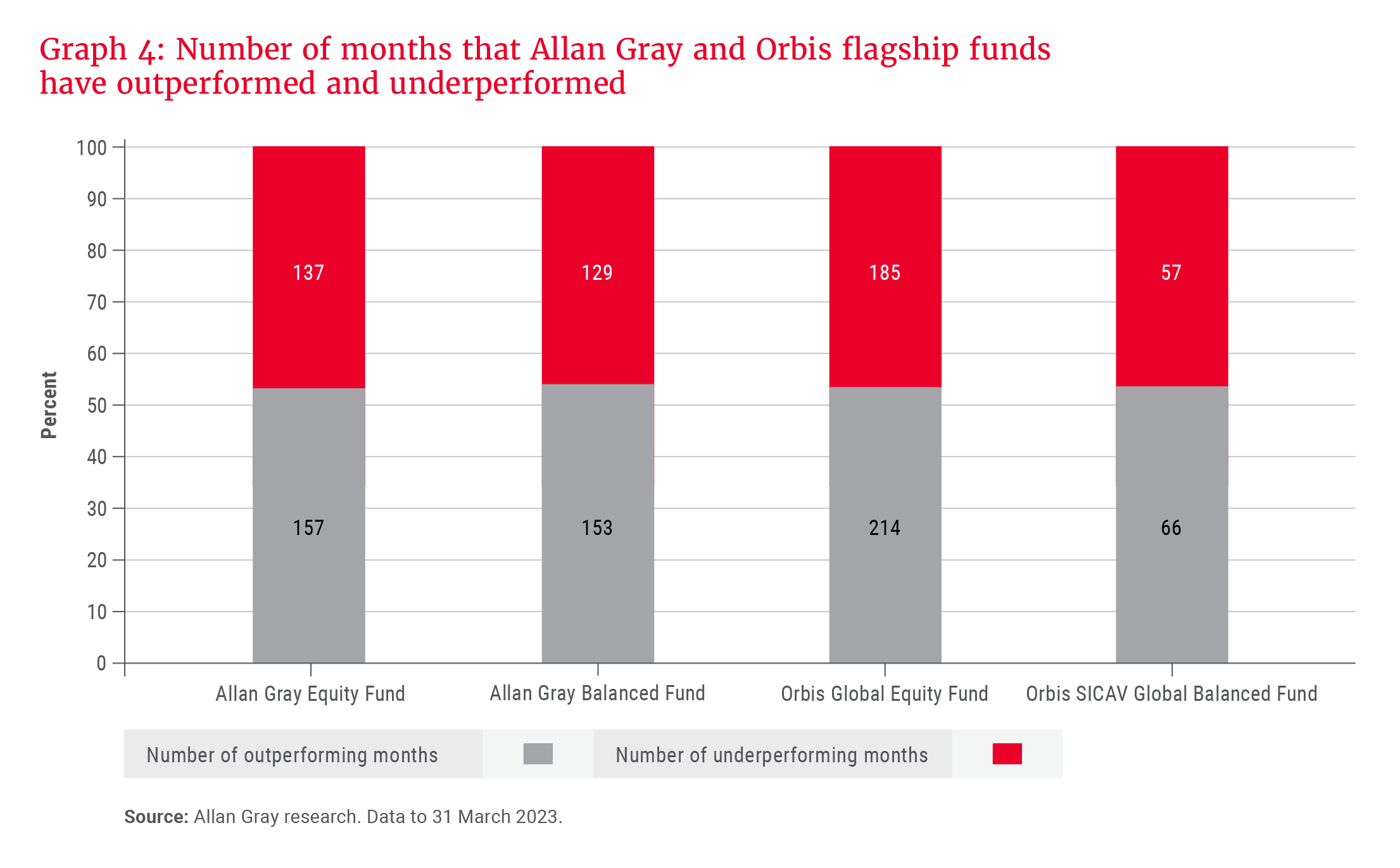

Looking at the monthly returns of the flagship Allan Gray and Orbis funds since their respective inception dates, as shown in Graph 4, it is surprising to learn that these funds have outperformed their respective benchmarks in 53-54% of all months. While outperforming in 54% of the months may not sound like a lot, historically this outperformance has occurred during periods when the market has fallen and our funds have held up better – 2022 was an example of this. By minimising the impact of market drawdowns, the Allan Gray Balanced Fund has delivered returns of 15.1% per year since its inception in 1999 versus the peer benchmark of 11.4%.

From a client perspective, staying the course to realise the longer-term returns means not getting distracted by the short-term noise that occurs when individual shares, and our funds themselves, underperform. Given our contrarian investment approach, this is inevitable as we are typically attracted to securities that are out of favour with the broader market, and it can take time for the market to recognise their true worth.

Marginal improvement tips the scales

In reflecting on the analysis of tennis and investment management, there are many parallels. In the pursuit of becoming a great tennis player and improving the odds of success over a career, 1% is a substantial advantage. As an investment manager, we know that in the pursuit of generating long-term returns for clients, there will be periods of shorter-term pain. Similar to top tennis players not winning every single point, we won’t outperform in every single month or year. What enables long-term success is staying true to our investment philosophy through different market cycles – and being mindful of marginal improvements to our investment process. Over the long term, 1% makes a powerful difference.