Shareholder voting on company resolutions can be a valuable tool for shareholders to attempt to influence positive change at a company. When it is in our clients’ best interests, we submit dissenting proxy votes on their behalf. Dissenting votes can either be an “against” vote or an “abstain” vote. The process resulting in a dissenting vote involves three parties: the investment analyst, the portfolio manager and company representative. The role of the company representative is to allow for meaningful and constructive engagement where shareholder concerns can be heard and addressed over time. When it comes to executive remuneration, our preference is to engage with the chairperson of the remuneration committee or an equivalent. Where there is no equivalent, the chairman of the board is approached.

Engagements are diverse and dynamic. Many span over numerous years and may include recommendations on how to implement or optimise a new policy, or how to improve an existing policy that has regressed. Dissenting votes are made only after engaging with the company and giving them the opportunity to bring matters into alignment with what we believe is in our clients’ best interests. Remuneration policies, which are better than peer or “acceptable industry standards”, may not be deemed sufficient to attain the positive outcomes desired for our clients. Broadly, the local standard of remuneration policies is not at our desired level due to the limited prescribed disclosure requirements. Engagements can therefore be protracted and may incorporate an educational aspect, which is meant to inform the directors of the levels expected of listed entities globally. Where necessary, examples from other markets are used to illustrate the standards expected.

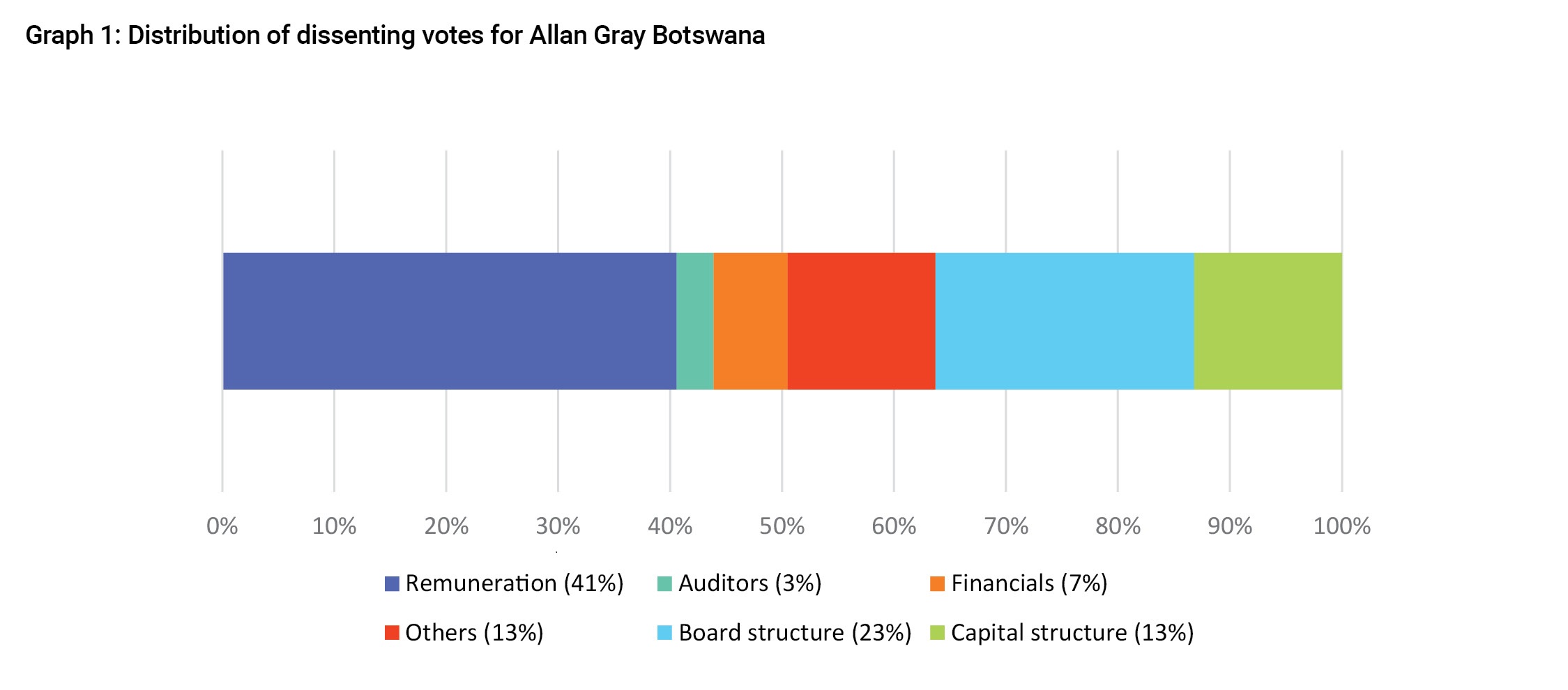

Frequent dissenting votes

The graph below illustrates the distribution of dissenting votes, followed by the rationales behind them.

Remuneration

Issues relating to the remuneration of executives accounted for most of the dissenting votes – 41% in this regard. Frequently, these issues stem from inadequate disclosure regarding how remuneration, especially the incentive component, is earned. Inadequate disclosure makes it difficult to assess whether the objectives of the directors have been sufficiently aligned with those of the shareholders. Disclosure should also be sufficient to allow judgement on whether the remuneration policy is adequate to attract, retain and motivate directors of a suitable calibre. It must be noted that discussions regarding remuneration quantum are not solely focused on reduction. There have been instances where we have recommended an increase in the level of remuneration to attain parity with peers at similar entities where underlying business performance warrants it. Dissention may also arise where our assessment reveals that the absolute quantum paid is too high relative to the business outcomes achieved and what is reasonable for the market.

Board structure

Our dissenting votes in this area are centred around our perceived suitability of specific individuals for board membership. Our views are informed by the expertise and experience brought to the board by the individual. The historic performance of the individual on the specific board (including at subcommittee level), among others, is also considered, as the desire for a board member is that they have a proven record of attaining positive outcomes for entities.

Capital structure

Dissention on the capital structure was due to the boards requiring dispensation to issue capital at a point in the future without shareholder approval. In our view, any capital issuances should be for specific uses that are communicated to and approved by the shareholders. This provides a level of oversight that we view as being necessary to safeguard the interests of our clients.

Auditors

Auditor issues centred around fees. We believe that audit fees must be reasonable and market based. They must be reflective of the size and complexity of the entity’s operations. Furthermore, in the absence of any material changes in the entity that affect these aspects, we do not expect the quantum of fees to increase materially year on year. Where this does occur, we would vote adversely after engagement with the company to ascertain that there are no conditions of which we are aware that could have necessitated a justifiable increase.

Financials

There were two instances where we recommended to “abstain” from voting for the audited financials. One occurrence is sufficiently rare that it warrants a mention. Choppies, the entity in question, previously had financials that were qualified due to irregularities in its inventory figures, among others. The entity then changed its auditors to Mazars. The resolution of the matters that had led to the previous qualified financials was never adequately explained, yet the financial statements for the year were unqualified. It is, therefore, our view that the financials may still be misstated. We will consider future developments in this regard prior to making our recommendation. The other entity which we abstained from voting for is a holding company that has insufficient disclosure on its key investments.

Others

Other issues on which we dissented ranged from disclosures regarding donations to climate policies, to the migration of operations and the registration of particular entities. In all arising matters, our voting recommendations will be informed by what we view as being most likely to result in positive outcomes for our clients. We assess the specifics of each resolution before making a recommendation.