We believe that a company’s remuneration policy should aim to attract, reward and retain competent executives, while incentivising alignment between these executives’ and shareholder interests. We realise that this is easily said, but can be difficult to implement. We aim to play a constructive role in this regard and frequently engage with company boards, particularly remuneration committee (remco) members, to encourage the adoption of executive incentive schemes that are aligned with shareholder interests and best practice standards.

Over the last year, dealing with the impact of COVID-19 has naturally been at the top of board agendas. For remcos, the focus has been on incentivising, compensating and retaining key talent in these turbulent times. We have spent a lot of time engaging on this matter, both internally and with company boards. Vuyo Mroxiso discusses the most prevalent engagement points and details some of our views, as shared with several boards and management teams of our investee companies.

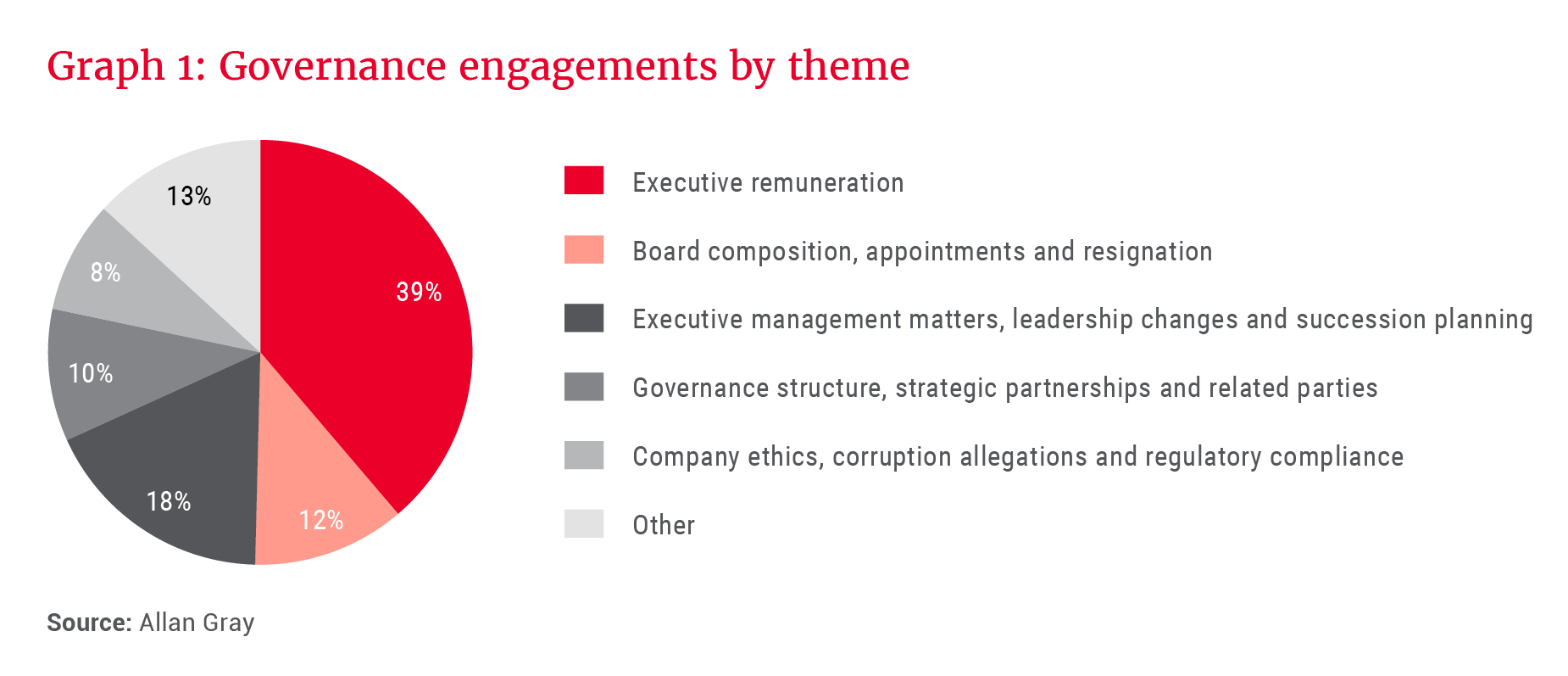

While the pandemic brought about some unique discussion points, executive remuneration remained our top corporate governance engagement theme in 2020, as shown in Graph 1. Many of our engagements centred around the impact of the pandemic on executive incentive schemes. Of specific focus was how boards should go about retaining and motivating key employees with long-term incentives (LTIs), having lost a significant portion of their value because of the pandemic; the use of discretion in adjusting performance targets that were set in a pre-COVID-19 world, and what remcos should consider in setting forward-looking performance targets when the future remains so uncertain.

Our overarching beliefs on executive remuneration remain unchanged: We advocate remuneration schemes that are closely aligned with shareholder interests, clearly linked to the strategic objectives and long-term performance of a company, and in line with best practice standards. However, we have aimed to be constructive during these extraordinary times and this has meant we have had to be reasonably flexible when evaluating remuneration schemes.

Retention of key talent

The pandemic resulted in many LTI awards being either underwater due to the COVID-19-induced sell-off in the first quarter of 2020, or highly unlikely to vest due to having unattainable targets (set pre COVID-19) attached to them. The prospect of LTIs not vesting for the next 12 to 24 months, or even longer, depending on how long it takes economies to recover, solely as a result of exogenous factors, has been cited as a significant retention risk by a number of boards and reward teams. We appreciate that this is a real risk and understand the importance of retaining key talent during these unprecedented times, yet we believe remcos should follow a pragmatic approach and only consider the introduction of retention schemes when it is deemed necessary. In our view, there is no “one size fits all” solution; rather, companies should consider the merits of introducing retention schemes in the context of their current remuneration structures.

The following two scenarios highlight some of the factors we typically consider when evaluating the merits of a retention scheme.

Companies A and B are comparable peers. They operate in the same industry and have a similar size, geographic footprint, scope and level of operational complexity. The remcos of companies A and B have proposed the same retention scheme: a restricted share plan (RSP) subject to a five-year continued employment condition, with cliff-vesting thereafter. There are no performance conditions attached to the award other than continued employment during the five-year period. The weighting of the RSP will be 30% of the total annual LTI award. The remaining 70% is a conditional share plan (CSP) that is subject to performance conditions at both company A and B.

In each case, how do we consider whether or not to support the retention scheme?

Company A

- Quantum of executive remuneration: Median of peer group

- History of pay-performance correlation: Strong positive relationship between executive pay and company performance

- Remuneration scheme structure: Pay mix is geared towards the long term; targets are sufficiently stretching

- Overall assessment: Good remuneration policy and implementation thereof; well aligned with shareholder interests

- Likelihood of us supporting the retention scheme: High

Company B

- Quantum of executive remuneration: Upper quartile of peer group

- History of pay-performance correlation: Weak positive relationship between executive pay and company performance

- Remuneration scheme structure: Pay mix is short-term-focused; targets are soft

- Overall assessment: Subpar remuneration policy; poorly aligned with shareholder interests

Likelihood of us supporting the retention scheme: Low

Companies X and Y are comparable peers. They operate in the same industry and have a similar size, geographic footprint, scope and level of operational complexity. Our overall assessment is that both companies have fair remuneration policies. However, we are generally concerned about the high quantum of executive remuneration in this industry. This is not a company-specific concern, but an industry-wide one.

In each case, how do we consider whether or not to support the retention scheme?

Company X

- Proposes a once-off retention award equivalent to 150% of total guaranteed pay for executives, vesting in equal tranches over three years following the grant date. This award is in addition to the normal LTI.

- Likelihood of us supporting the retention scheme: Low. Quantum of total pay is already high in absolute terms; we are therefore unlikely to support additional awards, especially when these awards are not subject to sufficiently stretching financial and strategic performance conditions.

Company Y

- Proposes a once-off retention award equivalent to 150% of total guaranteed pay for executives, vesting in equal tranches over three years following the grant date. This award will only kick in if Company Y’s in-flight LTI awards do not vest due to COVID-19-related impacts.

- Likelihood of us supporting the retention scheme: Medium. Quantum of total pay is already high in absolute terms, so even though these aren’t “additional awards” per se, we would strictly assess whether the COVID-19 retention award is warranted. This assessment would primarily be done as the retention/in-flight award vests over the three years under review.

Use of remco discretion

In principle, we are not opposed to the application of remco discretion. We understand that setting performance targets and evaluating outcomes in an uncertain environment are not easy tasks. However, discretion can be misused as a tool to inappropriately reward executives in periods of underperformance, a practice we think undermines the concept of “pay for performance”. As a result, we usually discourage the use of discretion and instead encourage companies to provide clear disclosure of how executives performed against preset performance targets. This level of transparency enables us to assess whether executives are being incentivised to act in shareholders’ best interests, and to determine whether a reasonable relationship exists between executive pay and company performance.

[we] encourage companies to provide clear disclosure of how executives performed against preset performance targets

However, we also realise that a completely formulaic approach to determining pay outcomes might not be the right solution for incentivising and retaining competent executives in this climate: Management teams may have been working hard, but their efforts are not being reflected in financial results due to the impact of COVID-19. With this in mind, we do not oppose remcos using their discretion to adjust performance targets to ensure that incentives adequately motivate and fairly reward executives, however, this discretion should be exercised in a manner that is consistent with management’s performance and aligned with the best interests of shareholders. We think the remuneration outcomes of the next few years will truly highlight good versus “average” remcos.

Limiting the upside of executive remuneration

We recognise that there will probably always be some element of chance in share-based remuneration. We encourage companies to attempt to control this where possible. In line with best practice standards, we advocate regular and consistent granting of share-linked awards, as opposed to large ad hoc/once-off awards. We believe this reduces the risk of unjustified windfalls. Even with all our attempts at being forward-looking, the COVID-19 crisis and the magnitude of its impact on stock markets and economies worldwide have shown that not everything can be foreseen. And, while we still believe that there is merit in regular and consistent awards, we realise that this might result in undue windfalls if awards were allocated when share prices were at historic lows.

We therefore urge remcos to follow a pragmatic approach and put measures in place to ensure that awards which eventually vest are reasonable. This can be done either at the time of granting the awards or at the end of the performance/vesting periods. Examples of measures that can be taken include introducing a cap to the value of LTI awards that stand to vest, reducing the quantum of allocations at grant date, or applying remco discretion to reduce the value of the vested awards if they are unreasonable.

Transparency is key

Where discretion is applied to either allow for the vesting of awards where performance targets are not met, or adjust the value of vested awards, we encourage remcos to provide a clear indication and adequate justification of how they arrived at the adjusted outcomes. This disclosure should be made available to all shareholders via annual reports. This level of transparency enables shareholders to adequately assess the appropriateness of the discretion and to determine whether it has been duly exercised.

Our stewardship activities include proxy voting

In addition to engaging on issues such as executive remuneration, we think critically about how we recommend our clients vote their shares at company meetings. The JSE Listings Requirements make it mandatory for a company with a primary listing on the JSE to table separate non-binding advisory votes on the executive remuneration policy and implementation report at the company AGM. These are important resolutions as they provide shareholders with a direct say on pay.

our views are solely driven by what we believe to be in the best interests of our clients

The key factors we consider when evaluating remuneration schemes include quantum of pay, how well aligned the remuneration scheme is with shareholder interests, the strength of the pay-performance correlation, the extent to which executives, in their personal capacity, are invested in the companies they manage (“skin in the game”), and whether the remuneration policy and implementation report are transparent enough to enable shareholders to make adequate assessments of the scheme.

By recommending a vote against a company’s remuneration policy and/or its implementation report, we are not necessarily suggesting that we lack confidence in the company’s executive directors; our views are solely driven by what we believe to be in the best interests of our clients, and we recognise that these may differ from those of other shareholders.