As mentioned in Part 3 of our Offshore advice chapter, the Currency and Exchanges Manual for Authorised Dealers (“the Manual”) governs payments from South Africa to offshore bank accounts. This includes the payment of benefits to beneficiaries after the death of an investor, which differ depending on the investment product. In this article, legal adviser Alix Moreillon considers the payment of death benefits arising from different investments.

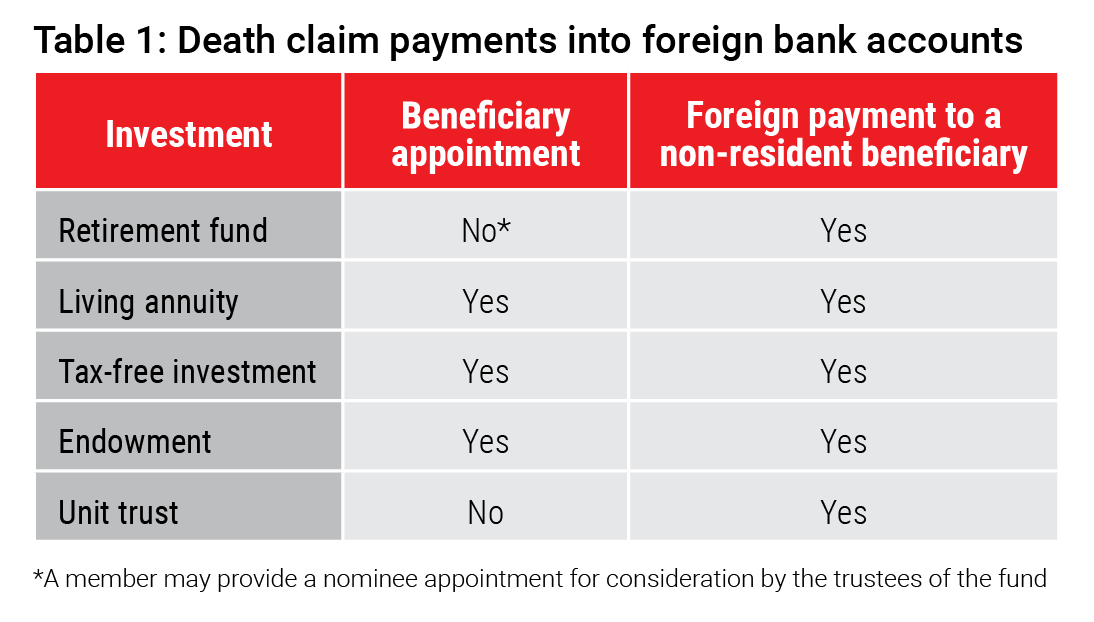

Rules around beneficiary nominations vary between investment products: You may nominate beneficiaries to receive the proceeds or take ownership of a long-term insurance policy, such as a living annuity, endowment or tax-free investment. This is not true for discretionary products, such as unit trust investments: these must be included in your will and will be administered by an executor. Meanwhile, although you can nominate beneficiaries to receive your retirement fund death benefits, these are ultimately allocated to your dependants and beneficiaries by the trustees of the retirement fund, as set out in Section 37c of the Pension Funds Act.

In all these cases, there are rules and requirements for payment of death benefits and inheritances to non-resident beneficiaries and foreign bank accounts – these are described below. In this context, a “non-resident” is defined in terms of the Manual (i.e. your normal place of residence is outside the Common Monetary Area). This would therefore also apply to an individual who is a beneficiary and ceased to be a South African tax resident at a date prior to the allocation of the death benefit.

The requirements are the same for retirement funds, living annuities, endowments and tax-free investment accounts. Payments of unit trust investments to non-resident beneficiaries are treated slightly differently.

Death benefits from retirement funds, living annuities, life policies and endowments

The Manual specifically states that proceeds of a death benefit from a retirement fund, as well as insurance policies, such as a living annuity, endowment and life policy (including the Allan Gray Tax-Free Investment Account), may be paid to a non-resident beneficiary once the exchange control (“excon”) requirements have been met. The excon requirements include presenting the death certificate and documentary evidence from the relevant institution administering the death benefit that confirms the full names of the beneficiary and the amount due to the beneficiary.

As a result, where a non-resident beneficiary is allocated a death benefit from these types of investments, any cash lump sum that this beneficiary chooses to receive may be paid directly to their foreign bank account. Allan Gray will apply for a tax directive (not applicable for tax-free investments) from the South African Revenue Service (SARS), pay any tax due and then pay the balance into the beneficiary’s foreign bank account.

Death benefits from unit trusts

Unit trusts form part of the deceased’s estate and fall under the control of the executor, who will need to administer the estate according to the investor’s will.

If you leave the assets in a unit trust account to a non-resident beneficiary in your will, the units may be transferred to an investment account in the name of the beneficiary or liquidated and paid to the beneficiary in cash. This will be subject to the administration of the deceased estate by the executor.

The Manual permits payment to a non-resident beneficiary if the liquidation and distribution account (“L&D account”) has been reviewed by the provider's authorised dealer (i.e. the bank appointed to control the flow of funds offshore), which is a requirement where the estate is valued at more than R250 000. If the estate is valued at less than this amount, then only the last will and testament of the deceased investor, along with the letters of executorship, are required to be viewed.

When it comes to Allan Gray investments, Allan Gray will act on the instructions of the duly authorised executor of the deceased client’s estate. Although payments into third-party bank accounts are not permitted, once the executor has received the proceeds of the unit trust account into the estate late bank account, payment may be made to a foreign bank account held in the name of the beneficiary.

Death benefits from foreign assets

Benefit from a South African estate to a non-resident beneficiary

According to the Manual, where a South African estate holds an authorised foreign asset (i.e. an asset acquired with funds legally transferred offshore), this may be distributed to a non-resident beneficiary, provided that all foreign administrative and related costs have been met from the foreign portion of the estate.

Therefore, if a South African investor holds an offshore investment, such as an Allan Gray Offshore Investment Account, the proceeds of this account may be retained offshore by a non-resident beneficiary.

Benefit from a South African estate to a South African beneficiary

The Manual also permits foreign assets inherited by a South African beneficiary from a South African estate to be retained without approval from the South African Reserve Bank (SARB), subject to tax compliance and disclosure to SARS. However, this benefit had to accrue to the beneficiary after 23 February 2022. When the benefit “accrues” may be determined as the date on which the benefit became unconditionally due to the beneficiary.

By way of example, Mr X died on 1 November 2021 and was a South African resident on the date of his death. At the date of his death, Mr X held units in various unit trusts in an Allan Gray Offshore Investment Account. In his will, he left the total value of this account (i.e. the offshore assets) to his daughter, Ms Y, who is also a South African resident. However, in our view, the benefit only accrues to the beneficiary once the L&D account prepared by the executor of Mr X’s estate has been approved by the Master of the High Court.

Therefore, if the L&D account was approved by the Master after 23 February 2022, then Ms Y would not require approval from the SARB to retain the units or the proceeds thereof offshore. However, she would still be required to comply with SARS tax disclosure and compliance requirements.

On the other hand, if the L&D account was approved by the Master before 23 February 2022, then approval from the SARB would be required to retain the assets offshore.

Benefit from a non-resident estate to a South African beneficiary

The Manual permits resident beneficiaries to retain a foreign asset that was held by a non-resident estate without this asset having to be declared to the SARB.

Familiarise yourself with the requirements

Payment of benefits to either South African or non-resident beneficiaries may require additional information and will be subject to your financial service provider’s processing requirements. Table 1 provides a high-level summary.

It is important to ensure that your beneficiary appointments are kept up to date. Please talk to your independent financial adviser about this and keep your beneficiaries for your Allan Gray investments updated via Allan Gray Online.

This article is part of our Offshore advice chapter. You can access the full series here.