With the cost of education soaring, relying purely on your salary to finance your children’s education is becoming increasingly difficult. Consider saving for education to relieve the future pressure.

As the public education system deteriorates, the cost of a good education is exponentially increasing. A three-year BCom degree at the University of Cape Town costs about R169 000 at current prices (excluding additional expenses). Assuming an education inflation rate of 9%, university education for a child five years away from studying could cost anything from R260 000 and one ten years away will cost R400 000.

Why your salary might not be enough

The problem with relying on your salary for education costs is that the cost of education grows at a higher rate than the average salary (and inflation in general). Over time, this difference effectively means that more and more of your salary will have to be set aside for your children’s education. While your children are still young, your salary is like the hare speeding away at the start of the race, but over time the tortoise of education inflation slowly catches up. In some instances, by the time your children are at university, education could take up a third or more of the combined salary of two parents. Two or more children can be prohibitively expensive to maintain if you take a wait-and-pay approach to funding their education.

You might disregard this if you are a high-income earner, but the tortoise and hare are just bigger for you – higher income just means you are likely to have higher education costs. The principle holds regardless of your level of income.

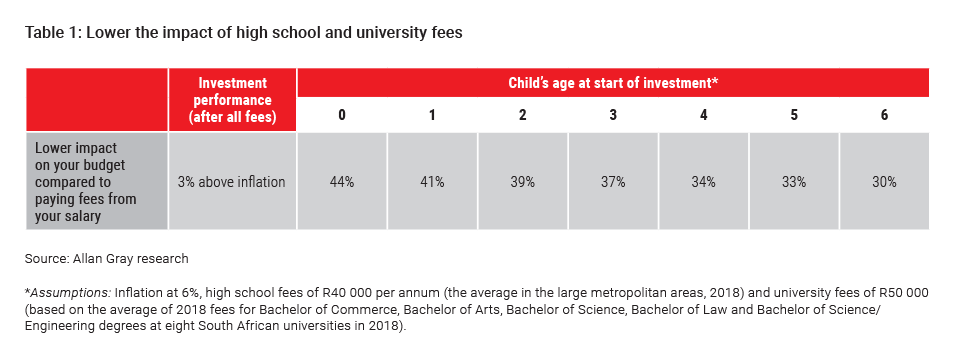

Investing can help you over the long term

The growth you earn on an investment can significantly lower the impact of education costs on your budget, even if you miss the opportunity of starting your investment at the birth of your baby. Table 1 illustrates the breathing space you can create in the future by getting your investment started today. By investing R2 100 every month from when your child is born, and only withdrawing from the investment when they start high school, you could reduce the impact of high school and university education costs by 40%. Even if you start contributing slightly more (R2 500) a few years later when your child is six years old, you would still enjoy significant savings.

There are various different products available to help you achieve your long-term goals. They have different benefits and restrictions and it’s important to understand the detail so that you can make appropriate choices – these are outlined below. There are additional considerations if you want to send your children to university overseas. We will discuss these considerations in Part 4.

Saving for education using an education policy

The traditional tool for saving for education is an education policy with an insurer. You pay a certain amount of money per month in a strict policy structure that promises a steady output at a predetermined time for you to use to pay school or university fees. The benefit of schemes like this is that there are guarantees that the insurer agrees to and you are locked into the policy, and some include an insurance component that ensures that education costs are covered even if you should pass away. The former is also a reason to be wary. Guarantees sometimes come with penalties for missing payments or changing the amount you pay. Some of these products also have opaque fee structures that are difficult to understand.

Saving for education using an endowment

The alternatives offer varying degrees of freedom, but also have downsides you should consider carefully. On one end of the scale you have endowments, which have a structure – but not as restrictive as most education policies. The key thing to know about endowments is that they are most effective if you are in the higher tax brackets, as the income tax rate is fixed at 30% for individuals. If your income tax rate is less than this, then you may be better off in other products.

The catch with endowments is that you may only make one withdrawal in the first five years of your investment. This means that if you are saving for education costs within this period, you may run into some difficulty. They are better suited to saving for tertiary education if your child is in primary school or just starting high school. They will not work for short-term needs and they can be complex to manage.

Saving for education using a tax-free investment

Tax-free investments (TFIs) occupy the middle ground: You are hemmed in with limits on how much you can invest, but there are no taxes on returns you make. The contribution limits are:

- R500 000 invested over a lifetime

- R36 000 invested in a tax year

These limits apply collectively to all TFIs in your name.

If you can live with these limitations, TFIs can be a useful tool to use. The important question becomes whose limits you choose to use. You can open a TFI in your own name or open one in your child’s name. If you use up your own contribution limits, you will not be able to use TFIs for another purpose in your own capacity. If you use your child’s name, then they will not be able to use TFIs in the future if you exhaust their contribution limits. Also, you cannot make a withdrawal from a TFI in your child’s name into your own bank account; it must go into the child’s bank account. Note that not all TFIs are the same. Some banks offer TFIs linked to money market accounts – these may be good for your short-term needs, but for the purposes of investing for the medium to long term, look for a TFI that allows you to invest a portion in equities.

Like the endowment, you may want to consider reserving TFIs for medium- and long-term needs as you want to give your TFI time to grow and allow yourself to enjoy the full benefit of earning returns free of tax. If you are constantly withdrawing from your TFI, you may find that you make losses. You also cannot replace money you have withdrawn from the TFI due to the lifetime contribution limits that apply.

Saving for education using unit trusts

Unit trusts offer the most flexibility. You can invest as much as you want, when you want and withdraw when you need to. For these privileges you lose the tax benefits of TFIs and endowments. And, importantly, you lose the guaranteed returns of education policies. The beauty of unit trusts is that you can use them for both long-term and shorter-term needs. If your child is three years away from matriculating, you can use a unit trust to help with the costs of university. The after-tax returns may be milder than the longer-term products, but every little bit you get will help you.

The three options outlined above offer you varying degrees of freedom in how much you want to invest and when you can withdraw, but more freedom may be a bad thing if you are not disciplined. While an education policy comes with a pre-defined plan, you will need to come up with a plan if you invest in endowments, TFIs and unit trusts. How much you invest, and the underlying unit trusts you invest into, will depend on how much you need and the time you have. You also need to be patient enough to wait for returns as they are not guaranteed like they are in most education policies.

Read how a couple from Johannesburg is successfully investing in unit trusts to save for their children’s education.

Credit – avoid it if you can

The repercussions of not investing for the long term may be that you are forced to use credit to finance your children’s education. Although the power of compound interest works in your favour when you invest, the same mechanism works against you when you borrow and makes credit the most expensive option – especially if you are making use of an unsecured personal loan.

As always, aligning your goals and timeframes with your product choices is an important component of making sure your decisions are fit for purpose. Consulting with a financial adviser may be the best first step to making the right plan and using the right tools.

Read more about saving for education in our five-part series.