We have always described ourselves as “contrarian” investors. While many of our best investment decisions on behalf of clients in the past have been at odds with market sentiment, we are also quick to point out that we are never contrarian for its own sake. Just like driving down the wrong side of the road is a bad idea, so too is blindly betting against the crowd. There are many nuances, and our degree of apparent “contrarian-ness” can vary over time.

Today there is little ambiguity. Each month, Bank of America Merrill Lynch publishes a survey of global fund managers. The survey asks more than 200 investment decision-makers who collectively manage more than US$500 billion to weigh in on the sectors, regions, and asset classes that they are favouring most (and least) in their portfolio decisions.

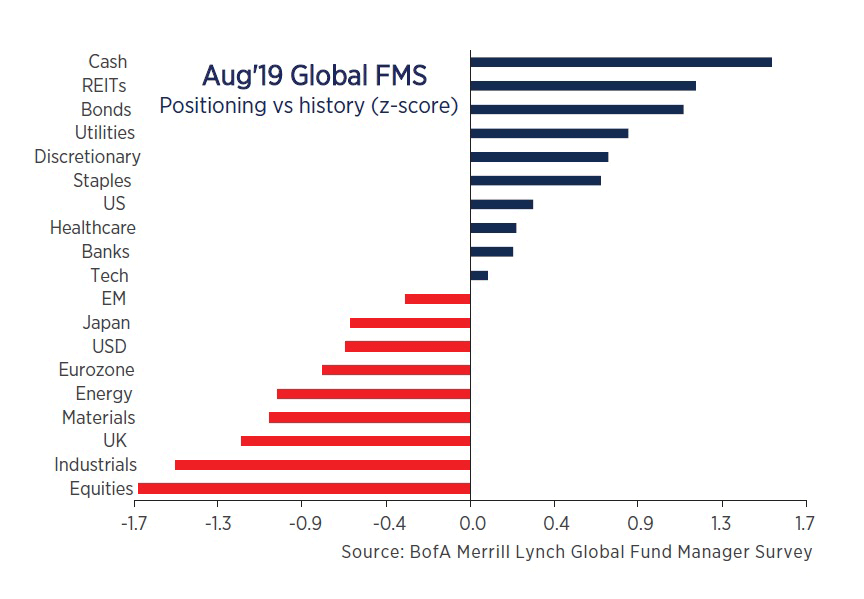

Graph 1 shows how the survey participants as a group are positioned today relative to history. Hold this graph up to a mirror and you will almost be able to see how the Orbis Funds are positioned today.

The consensus among survey participants favours cash and bonds from an asset class perspective, the discretionary and staples sectors, and the US from a regional perspective. In other words, all the areas where we’ve struggled to find much value. On the other hand, their positioning is lower in Emerging Markets, Japan and Europe and the Energy sector—all places where we are finding compelling value.

Of course, this is just one survey and not necessarily the opinion of “the market”. But it gives us a rough sense of current sentiment. On that basis, it is pretty clear that many of our current views are out of line with consensus thinking. That brings us to another key point about being contrarian: it’s easy to look foolish.

Try pulling up a chart of Coca-Cola shares since the start of 2019. Who needs a fund manager when you can make nearly 20% in just 8 months by buying shares of one of the world’s most famous brands? If you aren’t comfortable picking stocks, you could have just bought an S&P 500 index fund and made nearly 20% over that same period. Better yet, why not just lend money to Uncle Sam? 10-year US Treasury bonds have returned 13% year-to-date without any “risk”—at least according to the conventional definition of risk.

It’s easy to see why these assets have become so popular. But don’t be fooled by the smooth trajectory of their recent performance. The real risk with any investment is paying a higher price than it is worth and seeing your capital permanently impaired. From that perspective, the companies that have driven global equity returns of late carry much more risk than meets the eye.

Take Coke. The soft drink company’s shares trade at 33 times trailing 12-month earnings — well above their long-term historical average of 22 times. It is one thing to pay a premium multiple for a rapidly growing and highly profitable business or one with room to increase earnings. But with declining revenue growth in each of the past six calendar years and a debt load that has doubled since the start of the current decade, Coke appears to have dangerously high expectations built into its current share price.

Compare that with Tencent—a dominant internet company that reaches 96% of China’s online and mobile users through two messaging platforms (WeChat and QQ) as well as games, videos, music, news and other digital properties. Tencent trades at a similar multiple to Coke, but it is debt-free, revenue and earnings have grown rapidly over the past 10 years, and it still has many untapped growth opportunities ahead in areas such as payments, social advertising and cloud services. Best of all, we managed to get most of our exposure to Tencent at a substantial discount by purchasing shares of Naspers, a South African holding company that owns a majority stake in Tencent.

While these are just two examples of what we own and don’t own, we believe they are representative of a pattern that we see across the Orbis Funds. The common theme is that as the market continues to bifurcate, the portfolios increasingly represent areas of the market that are being shunned, while avoiding the parts that are loved. Importantly, this doesn’t mean we are being complacent about the associated risks such as the ongoing trade war between China and the US—we know things could get worse in the near term.

Going against the herd comes with its share of volatility, but in our experience it is often uncertainty itself that creates opportunity. We are willing to trade the near-term comfort of the herd for the potential to earn considerably more attractive future returns while protecting our clients’ capital over the long term