History seemingly often repeats itself, but it might be dangerous to assume that the investing landscape over the next 20 years will be similar to that of the recent past. Alec Cutler, from our offshore partner, Orbis, walks us through the previous megacycle, touches on the current cycle and explains how Orbis is positioned to take advantage of the opportunities on offer.

The failure of Silicon Valley Bank (SVB) has made markets worry about banks everywhere. In the case of Credit Suisse, that worry was well founded. We believe it is unfounded for the Japanese, Korean and Irish banks we hold. We sold out of also-robust ING Groep, which we had been trimming anyway on valuation grounds, and rotated some of that capital into Korean banks at bombed-out valuations. The rest of the banks we hold continue to look compelling, and we continue to hold them.

But the slide in bank stocks was not the only – or even the biggest – market impact of the current panic. The panic in banks has led to a massive shift in the expected path of interest rates. A month ago, markets expected US interest rates to end the year at 5.5%. They now expect rates to end the year near 4%, well below current levels. In other words, the market now expects the Federal Reserve Board (the Fed) to cut rates, rather than persisting in its fight against inflation. That is no sure thing, but equity markets have responded as if we are heading back to the low-inflation, low-rates environment of the past 15 years, and investors seem all too happy to believe that the playbook of the last cycle will continue to produce wins. Growth stocks have enjoyed that shift – Silicon Valley’s stock index, the Nasdaq, is now up since things with SVB kicked off, and so is the broader S&P 500.

The panic in banks has led to a massive shift in the expected path of interest rates.

It’s worth putting the bond market moves in context. On the Monday after SVB failed, yields on two-year US Treasuries fell by 0.56% – more than on the day Lehman went bankrupt, or on the day markets reopened after 9/11. In March, we have seen two-year yields rise or fall by 0.2% almost every day since the panic. Set against the tranquillity of the last 15 years, those are four standard deviation moves (in other words, if yield changes were normally distributed, these would occur one trading day every century or so). But in the 1990s, such moves weren’t uncommon. In the 1980s, they were pedestrian. The suppressed volatility we have seen over this low-inflation, low-interest rates cycle is the exception, not the norm.

Against that backdrop, this banking “crisis” seems a tiny distraction, or perhaps a shot across the bow, warning of what’s to come with a period of powerful inflationary impulses.

The previous megacycle

Events long ago teed up a tremendous period for corporations and investors via seemingly ever-lower interest rates, lower labour costs, technology-led productivity, and a peace dividend, topped off in recent years by massive liquidity injections. It would be difficult to think of a better setup for financial assets, and long-duration investments in particular. How did this come about?

1981

After US inflation peaked at over 14%, short-term interest rates peak above 20%, and the 10-year US Treasury yield peaks at 15%. With Paul Volcker at the helm, the Fed eventually breaks inflation, starting a four-decade cycle of ever-lower bond yields and borrowing costs.

The same year, Ronald Reagan fires the striking air traffic controllers, starting a 40-year swing in power from labour to capital.

1985

Margaret Thatcher beats the coal miners’ union, setting the same pendulum swinging in the UK.

1989

The Berlin Wall falls, and for the next three decades, liberal democracies enjoy the peace dividend, with defence spending as a percent of gross domestic product dropping from above 2.5% to below 1.5% in many European countries by 2018.

1995

Windows computers, Intel processors, email and the early rise of the internet spark a productivity boom. The Age of the Semiconductor begins in earnest.

2001

China joins the World Trade Organization, accelerating a wave of globalisation that lasts until 2016. Offshoring suppresses inflation, boosts corporate profitability and weighs on labour power in the developed world.

2008

The global financial crisis sparks central banks to drive interest rates down to zero and beyond, culminating in over 20% of global bonds trading at negative yields in 2020. The Fed alone prints US$3tn, with the Bank of Japan, European Central Bank and Bank of England collectively printing trillions more.

2020

COVID-19 sparks another surge of liquidity from central banks. The Fed prints another US$5tn and, with a wink and a nod, encourages the government to launch fiscal stimulus. Politicians happily oblige, with US$6tn in stimulus spending from US Congress and another US$1tn from the administration.

(As an aside, the word “trillion” – 1 000 000 000 000 – has become so commonplace in finance that we have completely lost our sense of its scale. A trillion seconds ago was 30 000 BC – before all recorded human history. A trillion is a lot!)

This cycle

All good things must come to an end, and so it looks to be with the backdrop for corporations and long-duration investments. More recent events point to reversals of the various tailwind-generating trends of the past.

2012

Facebook acquires Instagram, cementing the rise of social media and smartphones, and perhaps marking the point where the Age of the Semiconductor tips away from increasing society’s productivity.

2018

The US puts tariffs on imports from China, a death knell for the trend of ever-increasing globalisation, removing a powerful disinflationary force on the global economy.

2019

Major countries sign on to the Paris Climate Accords and start pressuring those who have not, kicking off the mega wave that is the electrification of the global economy. According to the investor Jeremy Grantham, an avowed global warming warrior, decarbonising the global economy could cost US$100tn over the next several decades, in today’s money. Barring a miracle, this will be nearly completely unproductive so far as costs are concerned. Rather than optimising the energy system for cost, we are now optimising it for a balance of cost and carbon. Similar to defence spending, if carbon dioxide is indeed the enemy, then this US$100tn is just a cost of societal survival. It is, thus, inflationary.

2021

Inflation breaches 7% in the US, with inflation in Europe, the UK and even Japan rising shortly behind.

The portion of the US workforce represented by unions hits a new low. Yet now, polls show public support for unionisation to be rising to levels not seen since 1965. This should drive labour costs higher, turbocharged by super-low unemployment (itself a reflection of labour costs that got too low). This pushes consumer prices up and corporate margins down.

COVID-19 has shown China, whose labour rates had already been driving towards the global average, to be a less ideal outsourcing partner than the profit-seeking capitalists thought, and focus has toggled to supply security. That means higher inventories, more local production and more redundant supply chains, all of which are inflationary.

2022

Russia invades Ukraine, again. After over three decades of a perceived peace dividend, people are slowly coming around to the notion that the Cold War has resumed. Spending on defence is required to ensure society has the ability to be productive, but that spending is itself unproductive, and either takes away from more productive uses (education, infrastructure, healthcare) or increases tax burdens, or both. Both are inflationary.

Central banks start raising rates and pulling liquidity from the system after finally admitting that inflationary pressures aren’t just transitory.

How we’re positioned

So much has changed from the last cycle, but many assets that were forgotten in the last cycle continue to trade at attractive valuations.

We start with inflation-protected bonds. We can currently lock in an inflation-protected yield of 1.4% in US Treasury Inflation Protected Securities (TIPS), set against market expectations of close to 2% inflation over any long horizon. In other words, despite all that’s changed, the market expects central banks to get inflation right where they want it. That means we don’t have to pay over the odds for inflation protection. Locking in a 1.4% increase in purchasing power looks reasonable, so we own TIPS.

So much has changed from the last cycle, but many assets that were forgotten in the last cycle continue to trade at attractive valuations.

TIPS also set a good bar. To earn a place in the portfolio, everything else must do better than a 1.4% real yield. And they can do better. A lot better.

In credit, we can now get yields of 7-9% lending to good, profitable businesses and getting the money back in a few years. That looks attractive.

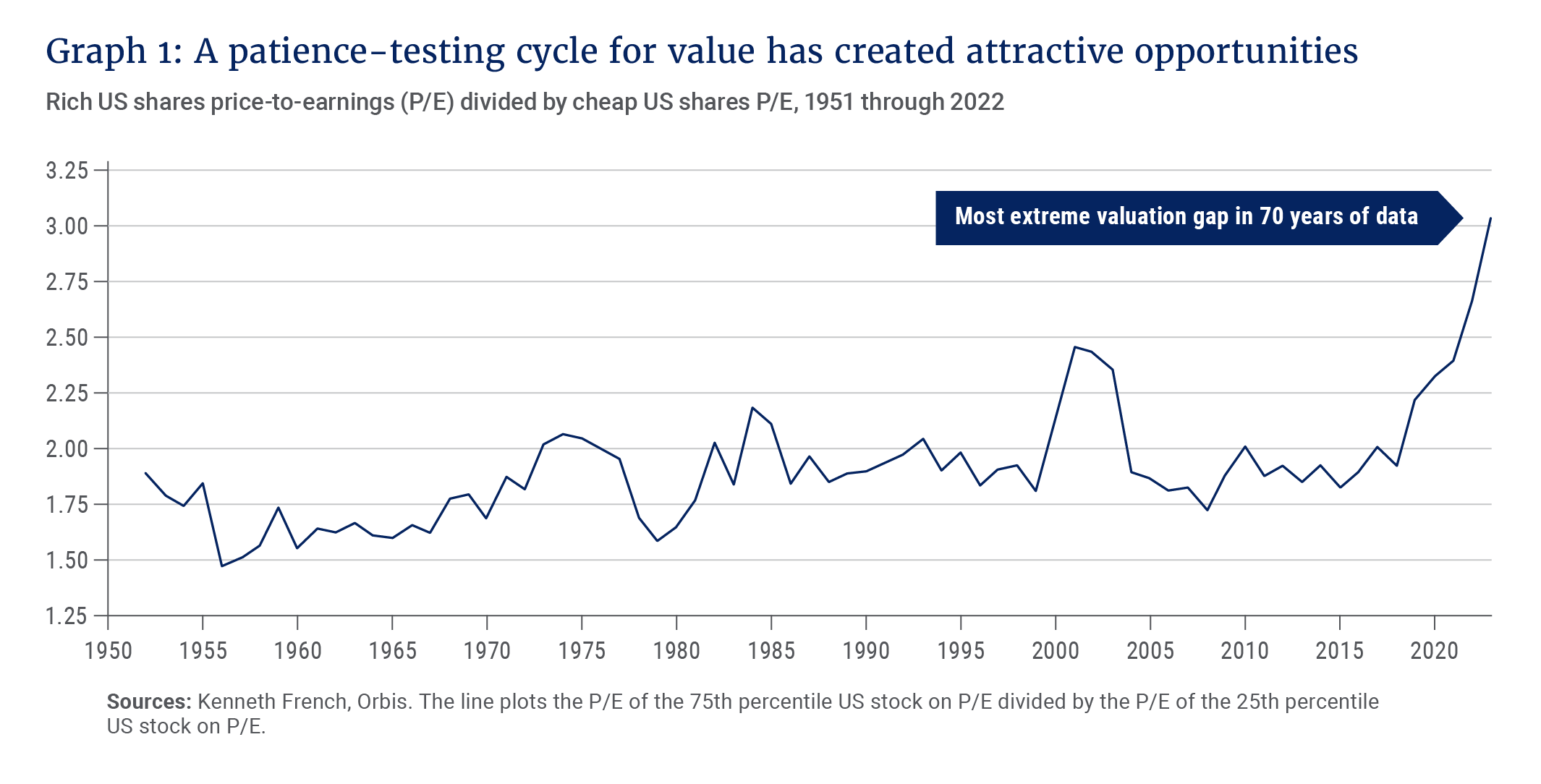

In equities, bottom-up opportunities abound, because the valuation gap between fundamentally cheap and expensive businesses remains extraordinarily wide. Using the US for its longer data history, Graph 1 shows that the gap in price-to-earnings valuations between cheaply and richly priced shares ended 2022 at its widest level in 70 years. While low-multiple shares have outperformed on price over the last 18 months, they have also outperformed on earnings, so on price-to-earnings, the valuation gap did not close.

Selected companies in defence, energy infrastructure, semiconductors, and oil and gas services provide things the world needs, and which are in short supply. Yet we have found several such businesses trading for less than 10 times our assessment of their sustainable free cash flows. Better still, in many cases those cash flows are either explicitly protected against inflation, or should be able to grow with inflation as supply shortages bite.

Who knows how history will unfold, but life from here could look incredibly different from the last megacycle. That could prove challenging for investors sticking to the last cycle’s playbook. But if valuations are any indication, it is an exciting time to be a contrarian.