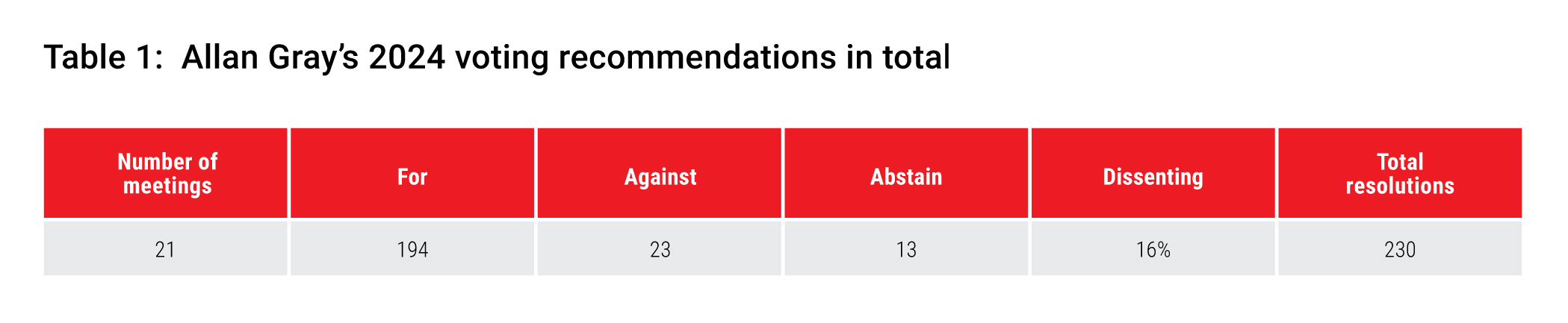

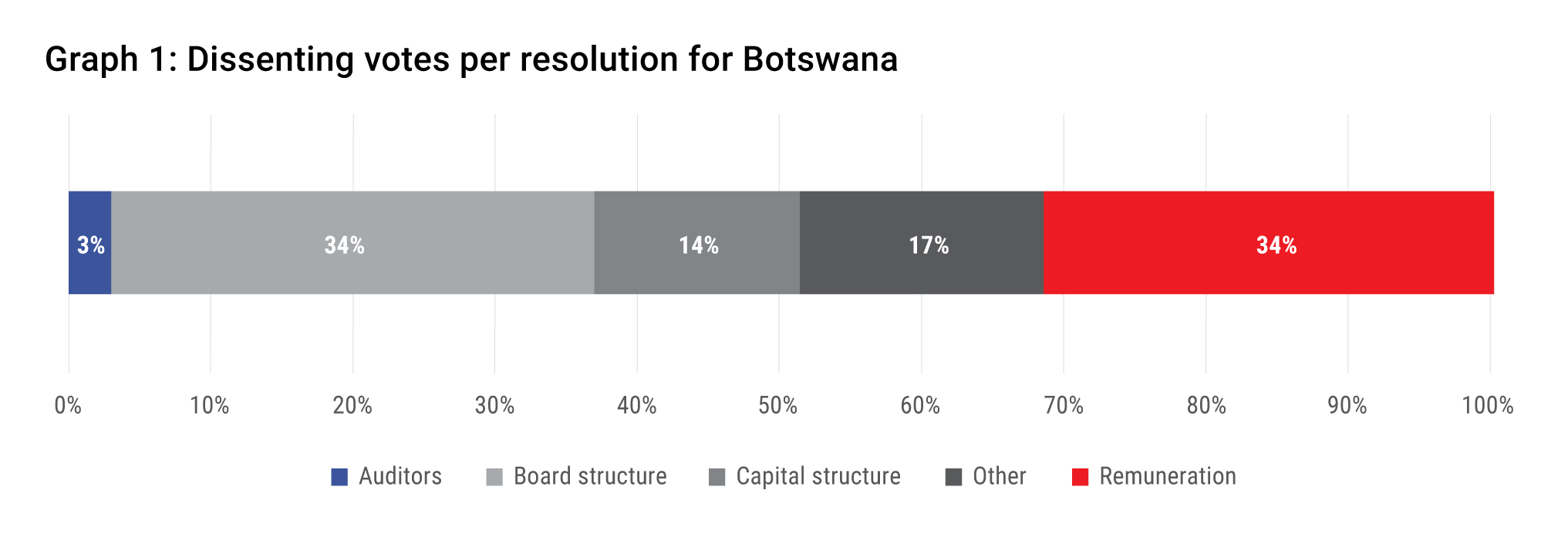

In 2024, we made voting recommendations on 230 resolutions tabled at shareholder meetings, as shown in Table 1, with 16% of these being dissenting votes. Dissenting votes are recommendations we make to our clients to either vote against a resolution or abstain from voting. We always share our rationale for recommending a dissenting vote with our clients. The first article in our Stewardship Report series described our voting recommendation process and in Graph 1 below, we categorise dissenting votes and offer some examples.

A breakdown of dissenting votes by category

Board structure (33%)

Our dissenting recommendations stem from concerns around director appointments or re-elections not being in the best interests of the company and its shareholders. As outsiders, we are not privy to the inner workings of the board. We, however, consider value creation or destruction in relation to the individual performance of directors, the composition and overall performance of the board, as well as other directorships each director may hold – past and present. We also consider whether any of the directors have previously been involved in fraudulent, corrupt or unethical activities. Below is an example of how we applied this approach in 2024.

Two of our dissenting recommendations related to individuals seeking re-election as non-executive directors. During their respective tenures, one supported a transaction which would have resulted in significant shareholder value destruction and the other chaired a board that allowed executive directors to be paid inordinately high sums of money for remuneration (including salaries, benefits and bonuses).

We evaluated each of their track records, considering the recency of their actions and their subsequent conduct. Based on our assessment, we recommended voting against their reappointment because we believed it would not be in the best interests of the companies and their shareholders for these individuals to serve as non-executive directors.

Capital structure (17%)

Capital structure garnered the second-largest portion of dissenting votes, driven by numerous routine annual general meeting (AGM) resolutions. This category includes resolutions to repurchase shares, which we generally support, and resolutions to increase the number of shares in issue, which we generally oppose, as they diminish the scarcity value of the shares our clients hold. We prefer that companies engage with shareholders first if they believe a share issue is necessary. These are our general positions; however, we examine each resolution on a case-by-case basis and consider company-specific contextual factors. Below are two examples of instances where the context justified a deviation from our typical stance.

- Example 1: The company proposed a resolution to repurchase ordinary shares, which we would generally support. However, considering the state of its balance sheet at the time of the AGM, we preferred that the available cash be allocated to debt repayment rather than share repurchases.

- Example 2: The company proposed an acquisition of a portfolio from its appointed asset and property management company. The company’s managing director is also a majority owner in the asset and property management company. The proposed acquisition envisaged issuing units to purchase the equity portion of the portfolio of properties and the debt associated with the portfolio was to be settled from the proceeds arising from a rights issuance. At the time of the proposed transaction, the company’s linked units were trading at a near 50% discount to their net asset value (book value). It was our view that the portfolio to be acquired was not priced at a discount to its intrinsic value, implying that it was overvalued. Issuing units to acquire an overpriced or overvalued property portfolio when the company is trading significantly below net asset value was not in the company’s best interests. Such an issuance would result in the material dilution of the existing capital structure, which is why we recommended that clients vote against the acquisition. The company eventually withdrew the proposal.

Remuneration (33%)

When assessing non-executive director fees, we consider both absolute terms and industry standards, as well as the specific context of each company. We recognise the importance of recruiting strong, high-calibre directors who understand the risks and responsibilities associated with serving as a non-executive director of a company listed on the Botswana Stock Exchange (BSE). We typically do not take issue with most non-executive directors’ pay; rather, our remuneration concerns stem most frequently from executive remuneration matters. There is often inadequate disclosure regarding how executive remuneration is earned, especially the incentive component.

Overall, we advocate for remuneration schemes that align executive pay with company performance. In reaching our recommendations, we perform an internal evaluation and apply our framework that considers quantum, structure and alignment, the quality of disclosure and the overall use of discretion. This is supported by various engagements with remuneration committees during the year. We aim for constructive engagements, where we are clear about our key concerns and share our practical recommendations for improvement. The below examples from 2024 demonstrate this approach.

- Example 1: Voting against remuneration resolutions

At times, we recommend dissenting votes when a company proposes a new remuneration structure that we believe is inferior to the existing one. This may result from significant changes taking place in the company, as in the case of one listed entity.

The company conducted a benchmarking exercise that led to executives being paid, in our opinion, exorbitantly high remuneration for a company of its size, complexities and geographical exposures. The targets set for executives are not disclosed to shareholders and the long-term incentive is based on a metric that we do not consider to be aligned with the shareholder experience.

- Example 2: Using abstentions for remuneration resolutions

Executive remuneration is granular and nuanced, and abstentions are often employed to prompt further improvements. In some cases, many of our recommendations were taken on board, indicating a positive trajectory, but the full extent of the improvements is still yet to be implemented. One of the listed companies in which our clients are shareholders is a case in point.

Alternatively, there may be disclosure omissions that need to be addressed. However, overall, we still consider the alignment between executive and shareholder outcomes to be sufficient, as demonstrated by another company locally.

Other (17%)

Other dissenting votes mostly related to changes in company constitutions, which we did not consider to be in the best interests of shareholders. In all arising matters, our recommended voting was informed by what we viewed as being more likely to result in positive outcomes for our clients. We assessed the specifics of each change in the constitution before making a recommendation, as demonstrated in the example below.

One company underwent an exercise to update its constitution and required input from shareholders and shareholder representatives. There were clauses that were amended in line with our suggestions. Some key clauses, however, were not amended and we could not recommend that our clients vote for the adoption of the constitution in its entirety.