If the value associated with a holding company is less than the sum of its parts, is it a worthwhile investment? Kamal Govan looks at the drivers of holding company discounts, reflecting on the risk and the opportunity.

Most investment-related debates these days are incomplete without a discussion of holding company discounts. Locally, the poster child for this topic is Naspers, with the discount to its underlying investments and the various opinions that investors have about how best to narrow this discount.

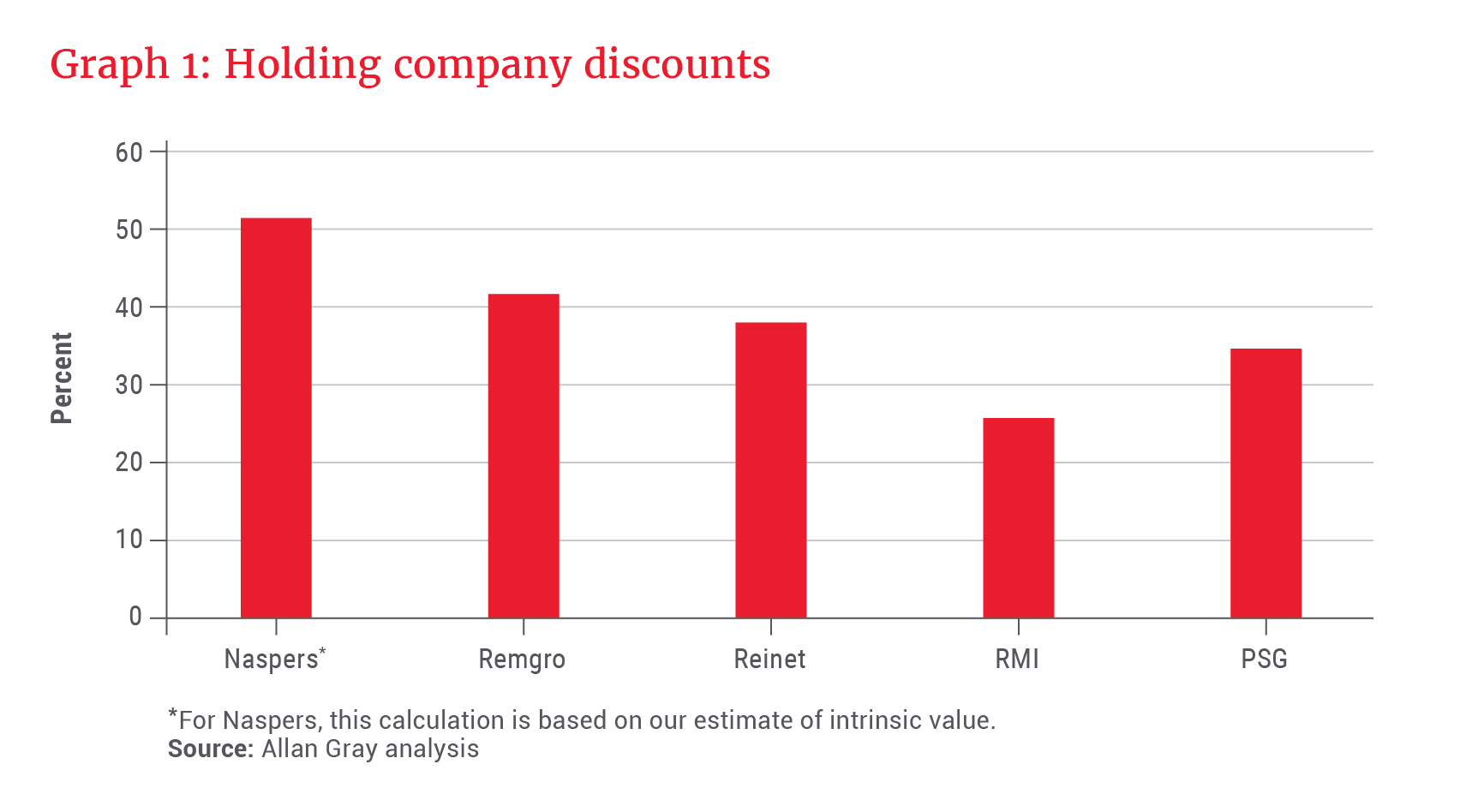

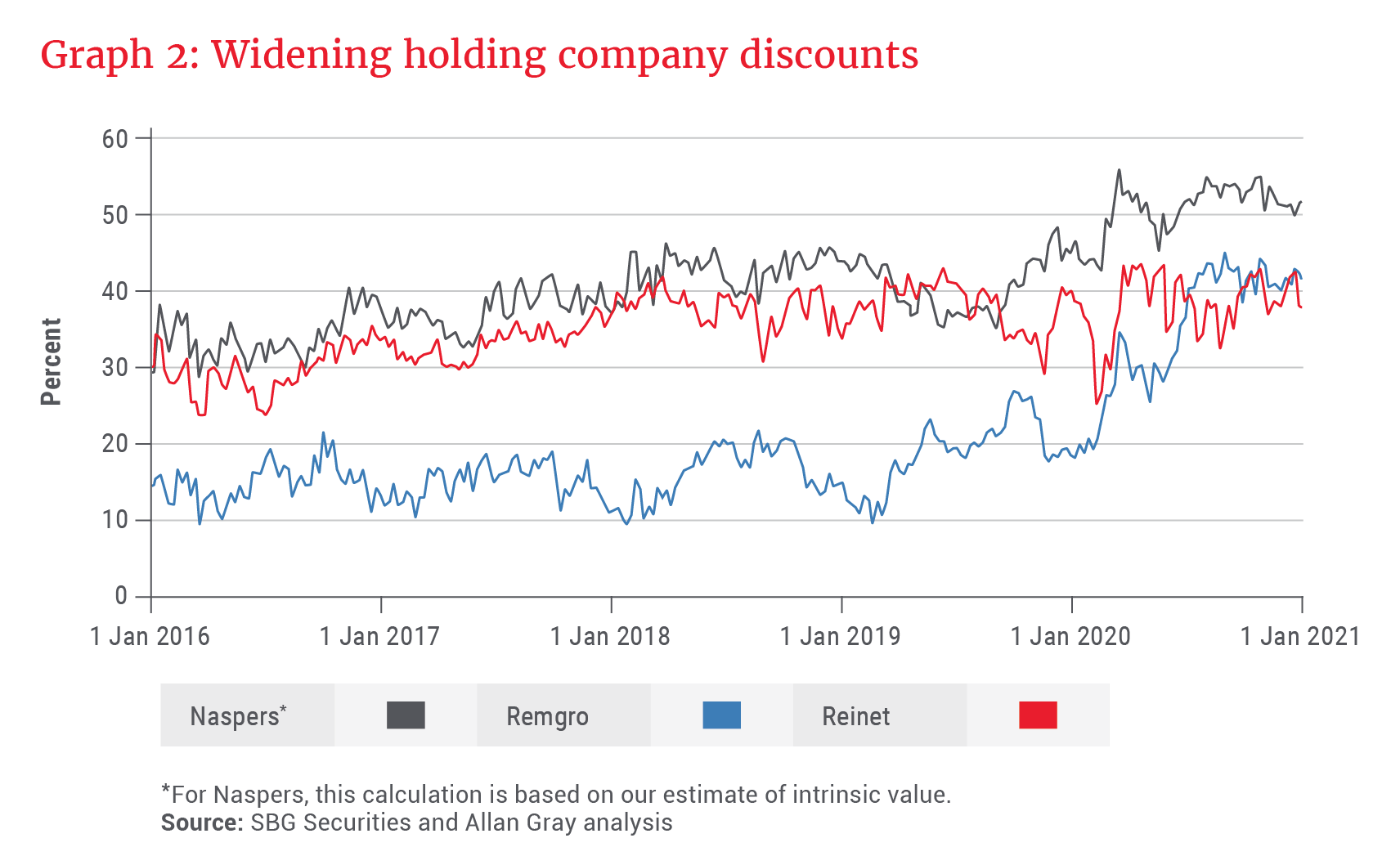

Holding company discounts are a common feature within our portfolio. Naspers, Prosus, Remgro and Reinet all trade at substantial discounts to their spot book values per share. Graph 1 shows the level of discount for a few example holding companies as at 31 December 2020. Holding company discounts have widened over the past few years – see Graph 2 for three examples.

This raises the following questions:

- What drives holding company discounts?

- Do wider discounts present attractive investment opportunities, or do they reflect heightened risk of these investment vehicles?

Key drivers of holding company discounts

Pinpointing the exact reasons for holding company discounts is notoriously difficult. Complicating matters is the fact that holding companies come in various forms and sizes. Some are large, others small; some have many underlying investments, others are concentrated; some hold listed investments, others focus on unlisted investments. What applies in one case, does not necessarily apply in the next. Nevertheless, there are several drivers of holding company discounts that may apply in a given situation. These are discussed in the following section.

Costs

Costs incurred by an investment holding company detract from its value and should be considered by investors.

No two holding companies are the same, and the costs of sustaining each therefore vary. There are different types of costs, including:

▪ Operating costs: Examples include management and director remuneration, head office overheads and audit fees. Sometimes these costs are offset by income earned by the holding company from things like the provision of central services or from passive income sources.

▪ Management and performance fees: In some instances, like in that of Reinet, shareholders incur management and performance fees for investing in the company. Management fees are generally a function of the net asset value of the company, recur annually and can be estimated reliably. Performance fees are based on shareholder returns over a period of time and are therefore complex to estimate.

▪ Taxes: The sale or unbundling of investments by holding companies may trigger capital gains tax (CGT) and/or dividend withholding tax (DWT) in South Africa. Tax considerations are unique to each holding company’s circumstances and depend on various factors, such as its legal domicile, ownership stakes in investments, and chosen modes of disposal. Tax regulations can be amended, which can change the discount applicable to a holding company.

Remgro provides good tax-related examples:

They disclose their estimate of the CGT liability that would be incurred if the company were to restructure in the most tax-efficient manner. Practically, the recent unbundling of their RMH stake was sequenced to maximise tax relief.

▪ Other: Sometimes it is important to consider costs that might be incurred in the future. Investors form a view on how holding companies can best unlock value for shareholders and estimate the costs associated with this. Examples include the transaction costs of selling investments or winding up a holding company structure. By their very nature, these costs can be difficult to estimate.

Well-managed holding companies can be wonderful to own for shareholders

Valuation complications and differences

The starting point for most holding company valuations is a sum-of-the-parts schedule. However, this is probably where the homogeneity ends. Investors need to form an opinion on and assign an intrinsic value to each investment on the schedule.

Valuing listed investments within holding companies is often easier than valuing unlisted investments. Listed companies publish vast amounts of financial and other information that informs investors’ valuations. Investors can compare their intrinsic value to the market price or the book value and adjust as required.

For unlisted investments, disclosure is usually very limited and comparable data may not be available. Investors often find it difficult to assign an accurate value to these investments. It is therefore not uncommon for investors to discount management’s disclosed values for unlisted investments, especially smaller ones. This is not to say that this is always correct, as sometimes these investments turn out to be multibaggers. Naspers’ investment in Tencent in the early 2000s is arguably the best example of this.

Further complications arise with the treatment of control premiums (the amount a buyer is willing to pay above fair market value to gain a controlling ownership interest), and this is another area without a common valuation approach. Examples where control premiums may apply include Remgro’s interests in Distell and RCL Foods, RMI’s interest in OUTsurance, and potentially even Reinet’s 49.5% interest in Pension Insurance Corporation Group (PICG).

Capital allocation

A holding company discount can reflect the market’s perception of a steward’s capital allocation ability and/or track record. By investing in a holding company, investors are outsourcing the responsibility to invest capital among businesses and sectors. If done poorly, or if investors are doubtful, they will demand a wider discount. Conversely, certain holding companies have traded at a premium to the book value per share (e.g. Brait at its peak), as investors have had a positive view on their ability to allocate capital or looked favourably on their track record.

It is not uncommon for the free cash flow generated by valuable investments to be deployed to subsidise inefficient businesses by an investment holding company. Such inefficiencies may arise as management teams fund budding new ventures (e.g. Reinet using British American Tobacco dividends or share sales to fund PICG), or attempt to turn around poorly performing businesses. Shareholders sometimes penalise holding companies for this type of capital allocation as they signal their belief that they can allocate that capital more effectively.

Investors wanting pure-play investments will often demand a discount to invest via a holding company structure.

Illiquidity of underlying investments

Unlisted investments especially are usually illiquid, and investors often apply an illiquidity discount. This is grounded in corporate finance theory, as selling these investments often requires a discounted price, and the process can be complicated, costly and time-consuming. Reinet is explicit in applying an illiquidity discount to its investment in PICG.

Governance

Analysing corporate governance is an important consideration in valuing holding company investments, as some structures are flawed to the detriment of minority shareholders. High-voting right share classes (e.g. Remgro and Reinet) or the extraction of value by related parties may be red flags worth considering.

Another consideration is the natural limits on one management team or board of directors adding value to a large and diverse set of holdings. It can be that managers are too thinly stretched, and this can be detrimental for shareholders.

So how does it all fit together?

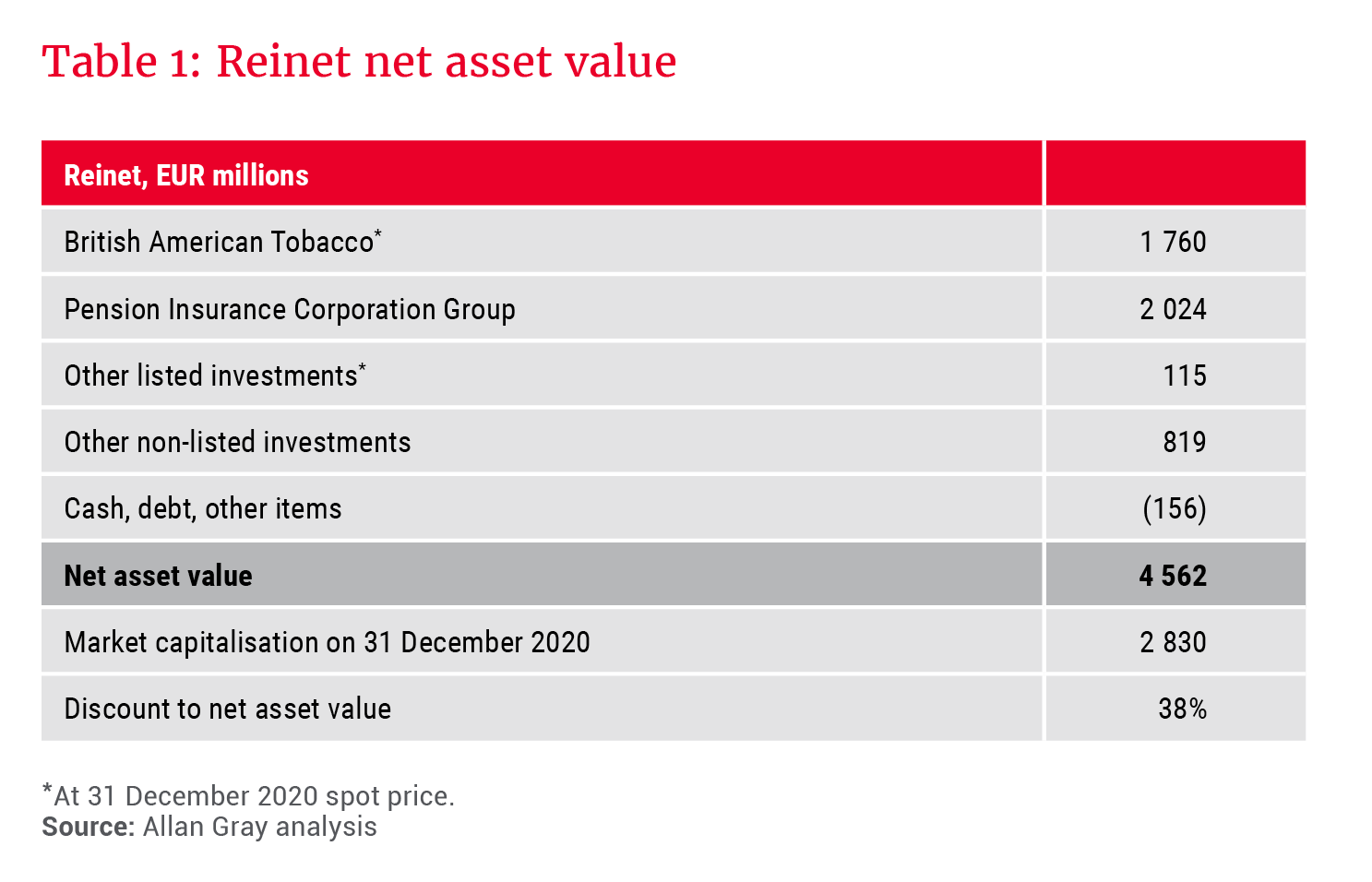

Using Reinet as an example, Table 1 provides a simplified snapshot of its net asset value as at 31 December 2020.

In short, we think a 38% discount for Reinet presents a favourable proposition. We think both British American Tobacco (at its listed price) and PICG (at management’s valuation) are attractive opportunities given their fundamentals. We acknowledge that it is difficult to gain comfort on the portfolio of unlisted investments but think that the discount affords a sufficient margin of safety if we are wrong.

Finally, Reinet’s underlying fee structure means that some discount is justified, but we think this is more than reflected in the current discount.

Why own investment holding companies?

Well-managed holding companies can be wonderful to own for shareholders. Berkshire Hathaway is a great example.

So, what are some of the characteristics of a good holding company investment?

- A portfolio of sound businesses, the majority of which are good investments in their own right

- Capital allocators who are sound stewards of capital and have a long track record of compounding intrinsic value

- Controlling shareholders or managers who are aligned with minority interests

- Abnormally wide discounts, especially when management is taking actions that may narrow the discount or increase the intrinsic value per share (e.g. through share buybacks)

- The ability to access unique investment opportunities or networks that are otherwise unavailable to investors

We continually assess the risk and return profile of each holding company investment in our portfolio. We monitor the level of the holding company discounts, as these discounts potentially add to the margin of safety within our portfolio.