“Prediction is very difficult, especially about the future.” – Niels Bohr

In cyclical industries, understanding where we are in the cycle and acting counter-cyclically can both be helpful for making successful long-term investment decisions. Using commodities in general and three examples from Anglo American in particular, Rory Kutisker-Jacobson discusses.

In theory, the fair value of any company is the present value of future cash flows one expects the company to generate over its lifetime, discounted at an appropriate rate. For a mining company, this free cash flow is, simplistically, a function of commodity prices, volumes and costs. With analysis, one can get a reasonable degree of confidence around the volumes a mine is likely to produce and the costs it is likely to incur in doing so. No doubt the future will be different from one’s expectations, but it is rare that a mine has unexpected movements of 20% or more in its costs or volumes. In contrast, it is not uncommon for commodity prices to move by 50% or more in a single year.

As an example, let’s assume there is a mine producing 100 000 ounces of gold at an all-in cost of US$1 000 per ounce (/oz). With the gold price at US$1 300/oz, it is generating free cash flow of US$300/oz or US$30m in total, before tax. If the gold price suddenly rallies to US$1 900/oz, all else being equal, that same mine will be generating free cash flow of US$900/oz or US$90m in total before tax. This is a three-fold increase in free cash flow from just a 46% increase in the price.

Thus, when valuing a commodity business, the overriding determinant of fair value is the “normal” commodity price one assumes.

Being pro-cyclical can be damaging, whereas being counter-cyclical can be very financially rewarding.

But the future is inherently uncertain, and commodities tend to exhibit large and unexpected movements in their prices over relatively short periods of time. If one doesn’t know what the future holds, how does one know what commodity price to plug into one’s model?

In investing, when looking forward, it is helpful to look backwards

What we know from history is that commodity prices tend to move in cycles with a relatively recurring nature. That is not to say we can predict the magnitude of a cycle, or when the cycle is likely to turn, but we can have some degree of confidence as to where we are in a cycle. Knowing where we are in a cycle makes all the difference, as it allows us to make some assumptions about future prices, as cycles tend to be self-correcting.

A low commodity price:

- Induces people to consume more, increasing demand for that commodity.

- Negatively affects the supply for that commodity: current production falls as high-cost producers become loss-making and go out of business, while future production is curtailed as the economic incentive of exploring for and developing mines of that commodity declines.

As demand grows and supply shrinks – both as a result of low prices – demand begins to exceed the available supply at each level of cost, driving prices higher. Thus low prices create the environment that eventually leads to higher prices. The opposite is also true: increases in commodity prices reduce demand while they incentivise new production, increasing supply and leading to lower prices.

The memory of the average market participant tends to be short

Perhaps it is human nature, but we tend to be very poor at learning from history. When a recent trend persists, all too often one hears “this time it’s different”, and the market makes investment decisions based on the current trend persisting into perpetuity. Consequently, from time to time, situations arise where commodity companies are priced by the market as if high commodity prices and profits will persist forever and, conversely, at times they are priced as if prices and profits are likely to remain depressed forever. This is seldom true in either case. Thus, being pro-cyclical – i.e. buying when prices and expectations are high – can be damaging, whereas being counter-cyclical – i.e. buying when prices and expectations are low – can be very financially rewarding. This is true for both investors and the companies in which they invest.

Anglo American, a company whose history is intertwined with that of South Africa, celebrates its centenary this year. Here are some recent real-life examples of investment decisions made by Anglo, and how these decisions have impacted on the fortunes of the company and its shareholders.

Minas-Rio

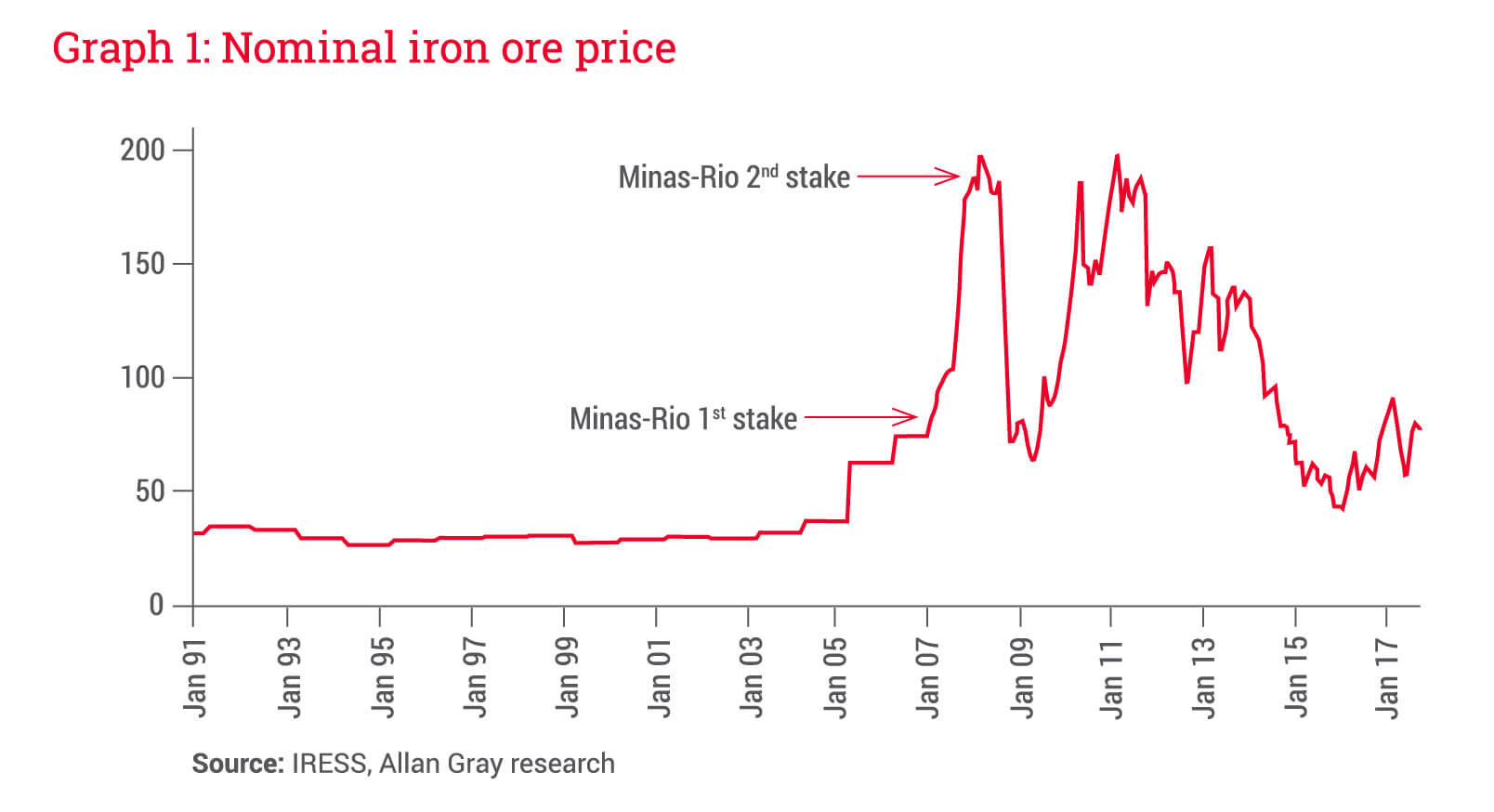

Anglo’s foray into Brazilian iron ore is an example of the dangers of being pro-cyclical. For a long period of time up until the end of 2003, the seaborne iron ore price traded at around US$30 per tonne (/t). Thereafter, the price began to rise appreciably, primarily as a result of seemingly insatiable demand out of China.

By December 2006, the price had more than doubled to US$80/t. With prices and profits rapidly rising, iron ore mining became a very attractive proposition.

By April 2007, Anglo could no longer resist the temptation and made its first investment in Brazil, acquiring 49% of an iron ore deposit called Minas-Rio for US$1.15bn. Situated some 525 km from the port, Minas-Rio was expected to begin production by late 2009 after a further capital investment of US$2.35bn. It was envisaged that it would produce 26.5 million tonnes (mt) of iron ore per annum, with optionality to expand this to 90 mt per annum over time.

Perhaps it is human nature, but we tend to be very poor at learning from history.

By January of 2008, the iron ore price had again more than doubled to around US$180/t and Anglo decided to acquire the remaining 51% of Minas-Rio, announcing the remaining stake would cost a significantly higher US$5.5bn. While the outlook for increased demand from China continued to be rosy, at this stage, two things were certain: the price of iron ore and industry profitability were both very high relative to history.

Shortly thereafter the first bad news emerged when it was announced that the capital expenditure required had been increased to US$3.6bn and, due to issues with environmental licensing and access to land, first production had been pushed out to early 2012. This was a sign of things to come. It slowly began to emerge that in its desire to acquire Brazilian iron ore exposure, Anglo had overlooked the technical and licensing challenges facing the project.

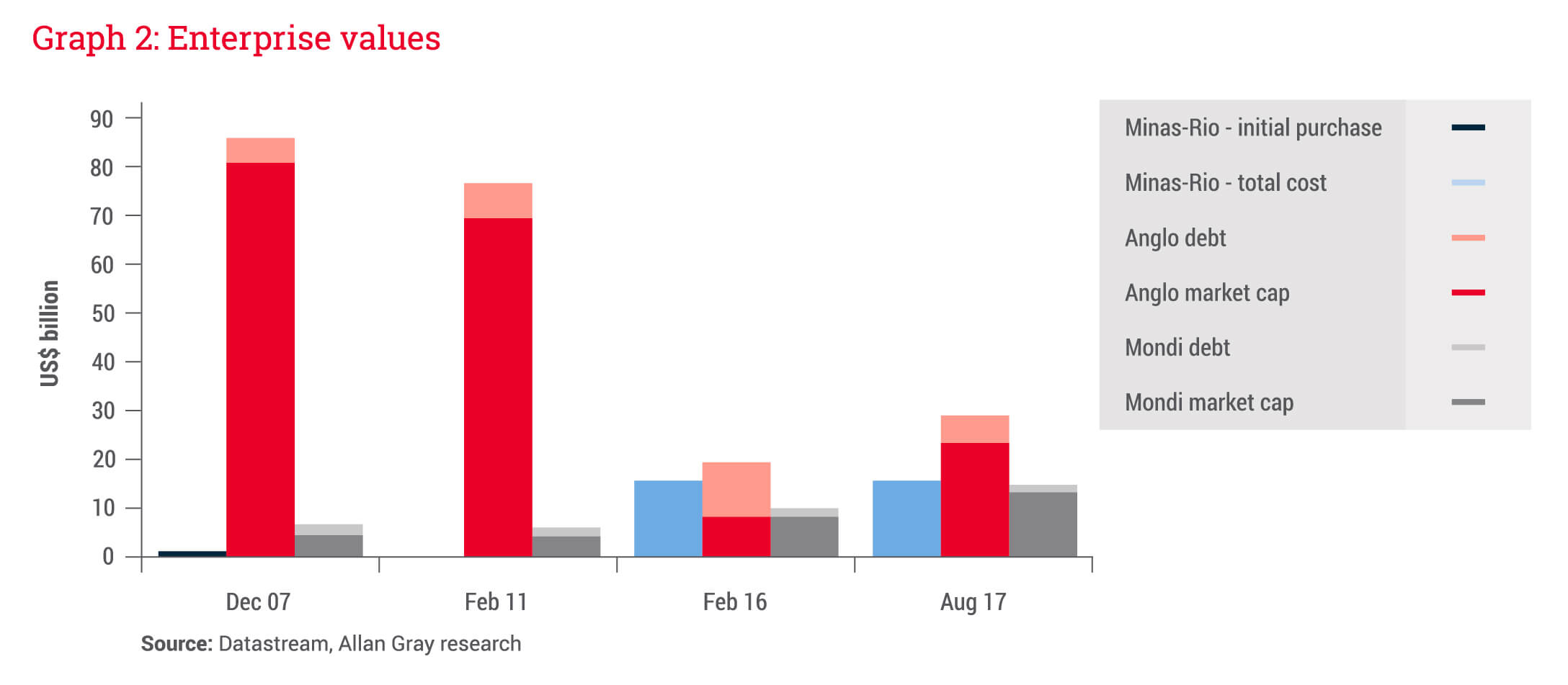

Fast-forward to today, and the company has spent US$8.4bn in capex to bring Minas-Rio online. While the mine is now operational, it is producing only between 16 mt and 18 mt per annum. At the same time, the iron ore price is now less than US$70/t; still high relative to history, but a far cry from the heady heights of 2007 to 2011. As Graph 1 shows, Anglo timed the peak of the market almost perfectly when it announced the acquisition of the remaining stake.

All in, Anglo has spent over US$15.5bn on Minas-Rio, a project that is likely to generate marginal returns from here. To put that in context, the total current market value for the whole of Anglo is around US$22.6bn.

Metallurgical coal

More recently, Anglo’s metallurgical (met) coal business is an example of the benefits of making counter-cyclical decisions. Just 18 months ago, Anglo looked to be in dire straits. Commodity prices across the board had fallen materially and, as a result of overburdening the company with debt during the good times, it appeared that Anglo would need to sell assets or have a rights issue to strengthen its balance sheet.

One asset earmarked for disposal was Anglo’s met coal business. From a peak of around US$300/t in 2011, the met coal price had fallen consistently since to around US$80/t by February 2016. With costs at a similar level, the division was barely breaking even. Coal in general had become a four-letter word and, despite Anglo having world-class assets, arguments abounded as to why the division would never again earn a decent return on capital.

Anglo entered discussions to dispose of the met coal division with various parties and, by July of that year, was said to be close to finalising a deal, with press reports suggesting Anglo would receive between US$1.3bn and US$1.5bn for the division. To its credit, throughout this process Anglo was adamant it would not dispose of any asset below its estimate of fair value.

Before a deal could be concluded, the met coal price began to rally, and by year-end, it was back at around US$200/t. The long-term met coal business hadn’t changed at all, but because the commodity price cycle had turned in the short term, it was suddenly a much more attractive prospect. For the 12 months to June 2017, the met coal division earned US$1.1bn. Fortuitously for shareholders, Anglo never sold. It now looks likely that Anglo will earn more in 18 months than what the market anticipated it would get for selling the entire division. Perhaps management was lucky, but credit must go to them for holding out for a higher price and the subsequent outcome.

Mondi

Anglo’s unbundling of Mondi in July 2007 demonstrates a third point: shareholders can benefit from making up their own minds about commodity cycles. Anglo unbundled the paper and packaging group to shareholders, transferring the active decision of staying invested or divesting to each shareholder, rather than making that decision on their behalf. In effect, the transaction gave shareholders 91 Anglo shares and 35 Mondi shares1 for every 100 Anglo shares held.

Assuming shareholders stayed fully invested in these two shares, they had three options:

- Option One: Do nothing, i.e. retain Anglo and Mondi shares.

- Option Two: Sell Mondi shares and invest the proceeds in Anglo.

- Option Three: Sell Anglo shares and invest the proceeds in Mondi.

What was the right investment decision?

For those shareholders who pursued Option One and did nothing, for every R100 invested on 2 July 2007, they would have R103 today. Hardly an optimal outcome, when to just keep pace with inflation one’s investment would need to be worth R181 today. Those who pursued Option Two and invested solely in Anglo, would have fared even worse, with an investment worth a meagre R66 today. That’s a negative return in nominal terms over 10 years! Finally, those who invested solely in Mondi would have an investment valued at R754 today.

As Graph 2 suggests, the largest cause of such a wide disparity in outcomes was the starting valuation. At the time, Anglo was priced for perfection, with investors extrapolating that high commodity prices would persist into perpetuity, whereas questions were being asked about what an increasingly digital world meant for paper consumption in the long term.

Anglo’s remaining diversified mining businesses were at the top of their cycles, trading on 19 times historic earnings, despite those earnings being at a record high. Mondi traded on just 11 times earnings, despite 2006 reported earnings being 36% below that achieved in 2003. A decade later, Mondi trades on 19 times earnings, that are materially higher, whereas Anglo trades on just 8 times historic earnings, despite commodity prices generally being lower today than they were at the peak. There were other factors at play, but counter-cyclical investors were well rewarded and they would not have had the chance to benefit without Anglo’s decision to unbundle.

In conclusion, while we believe that it is always important to take a long-term view in investing, this is particularly true in cyclical industries, where overreacting to short-term noise can mean missing out on opportunities or making costly mistakes.