Remgro and Reinet are great examples of holding companies in our clients’ portfolios that trade at substantial discounts to the sum of their parts, for different reasons. Jonty Fish and Malwande Nkonyane share some insights into their investment theses.

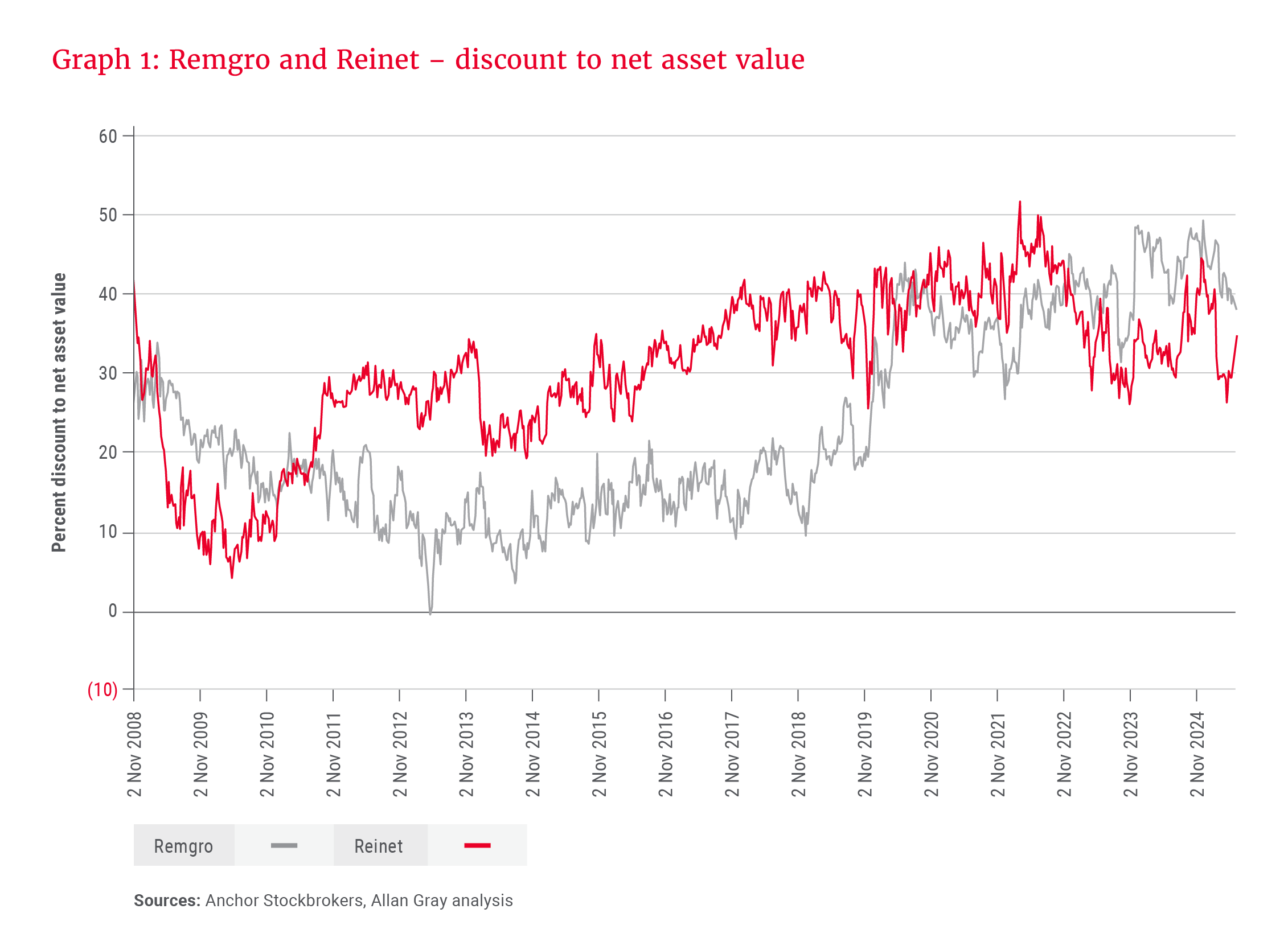

It is not unusual for holding companies to trade at a discount to the sum of their underlying investments. Tax, head office costs, management and performance fees, or lack of disclosure in investee companies are just a few examples of the different reasons investors may value a holding company below its net asset value (NAV). Graph 1 illustrates the discount to NAV over the years for Remgro and Reinet. The stories of the two groups are outlined below.

Remgro: From tobacco roots to diversified holdings

Remgro’s history dates back to the 1940s, when the founder, Dr. Anton Rupert, established a tobacco company that would later become Rembrandt. Over the years, Rembrandt’s tobacco interests grew significantly, first through the consolidation of its holdings with Rothmans International, the world’s fourth-largest cigarette manufacturer at the time, and later merging those interests with British American Tobacco (BAT), the world’s second-largest cigarette producer. Rembrandt also expanded beyond tobacco into sectors such as wine and spirits, financial services, mining, printing and packaging, medical services, engineering and food – although tobacco continued to underpin most of the group’s value.

In the early 2000s, Rembrandt was restructured to form Remgro and VenFin, with Remgro housing the tobacco, financial services, mining and industrial interests, and VenFin housing the telecommunications and technology interests. Remgro remained a predominantly tobacco play until 2008, when BAT was unbundled.

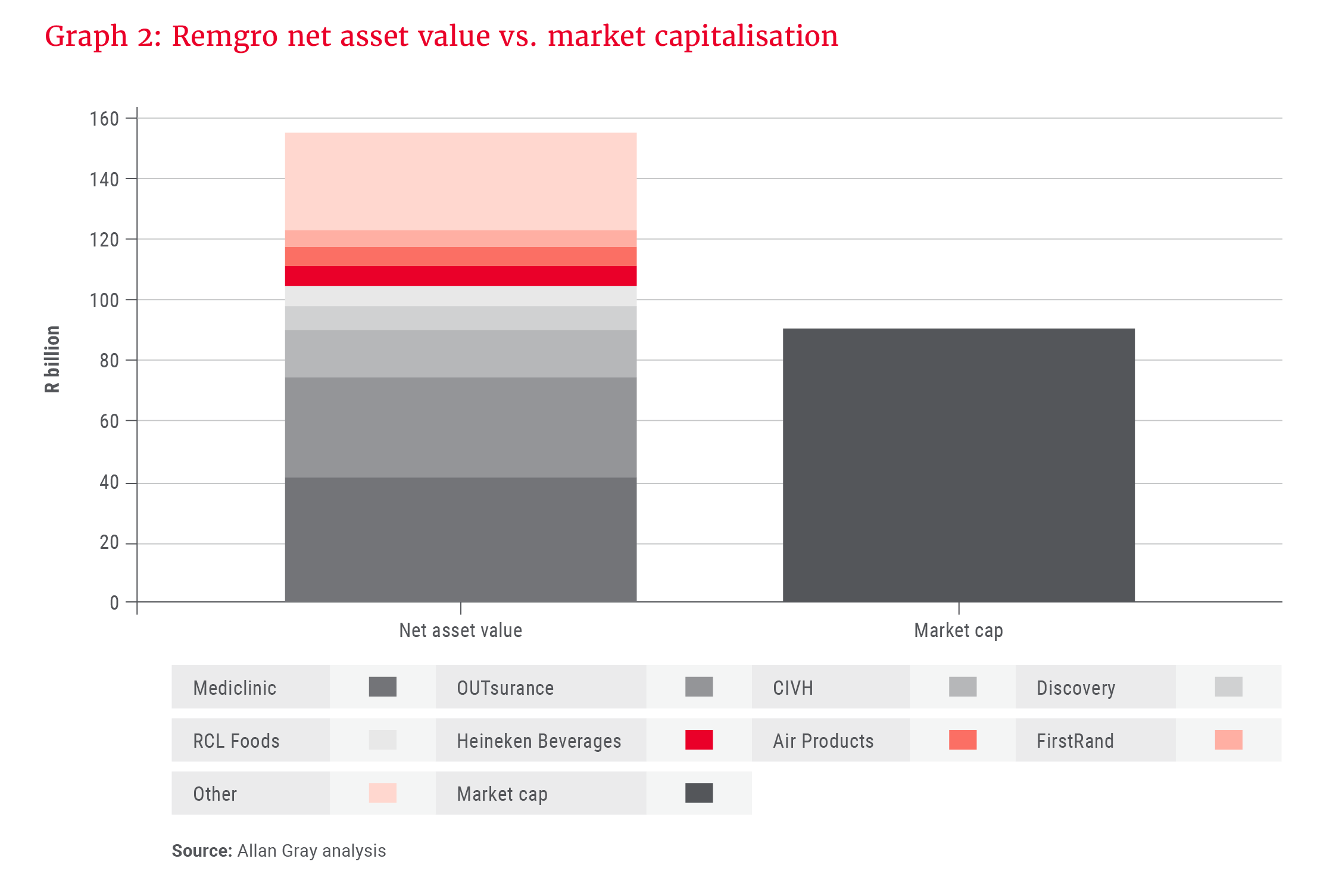

Today, Remgro is a diversified investment holding company, with over 20 underlying investee companies, spanning many sectors, including consumer products, infrastructure, financial services and healthcare – to name a few. The top five investments make up close to 70% of NAV, as shown in Graph 2. If you drink Heineken beer, Savanna or Amarula, use Flora margarine, eat Yum Yum peanut butter, are insured by OUTsurance or Discovery, bank with FNB, or have visited a loved one at a Mediclinic hospital, you have interacted with one of Remgro’s many investee companies.

Perhaps less familiar are Remgro’s industrial assets. One example is Air Products South Africa, which manufactures and distributes industrial and specialty gas products in the Southern African region. It has managed to grow its topline at faster than 10% per year for the last decade – an incredibly rare achievement for an SA-based business. Globally, listed peers trade on very high price-to-earnings multiples (>20 times), given their high quality and defensive nature.

Historically, Remgro has traded at an average discount to its NAV of around 20%, with narrower periods of less than 10% and recent extremes reaching close to 50%. At the time of writing, Remgro’s discount to NAV is close to 40%, well above the long-term average. A delayed deal between Vodacom and South Africa’s largest fibre operator, Maziv – a subsidiary of Community Investment Ventures Holdings (CIVH), which is majority-owned by Remgro, integration issues at Heineken Beverages, and earnings pressure at Mediclinic Switzerland have soured investor sentiment. Despite acknowledging that some of the market’s concerns are valid, we think prevailing pessimism is overdone, especially since quantifiable reasons for the discount (tax and head office costs) justify a discount less than 10%.

What makes Reinet’s valuation particularly compelling is that its market capitalisation is now lower than the combined value of its net cash and Pension Insurance Corporation sale proceeds …

To put the current discount into context, at today’s price, you can get Remgro’s share in OUTsurance + 75% of their stake in Mediclinic + their share of CIVH + the cash Remgro holds for a value close to the current market capitalisation. In other words, we think the market is placing a nil value on a large portion of Remgro’s investments.

While the exercise above is not necessarily the best way to think about the discount, it does highlight the value currently being left on the table.

These initiatives highlight Remgro management’s focus on unlocking the discount and creating value for shareholders. We think that makes for a compelling investment case.

Recent positive developments also point towards a higher probability of the discount narrowing. These include:

- The recent approval of the Vodacom/Maziv deal with updated terms valuing Maziv at a large premium to management’s value. Not only does this affirm Maziv’s value, but it also highlights Remgro’s tendency to value its unlisted investee companies conservatively.

- Heineken Beverages overcoming its integration issues, allowing the business to focus on reigniting growth. We think this business could be worth more than Remgro management’s current valuation.

- Good execution of cost control initiatives at Mediclinic Switzerland, combined with lower Swiss interest rates, that should be a tailwind for earnings.

- Unbundlings and restructurings, which have unlocked value for shareholders. Over the last few years, investment holding company RMH, logistics company Grindrod and, more recently, eMedia Holdings have been unbundled. Rand Merchant Investment Holdings’ structure was simplified, which led to serious value unlock for shareholders in relation to the direct OUTsurance listing. RCL Foods also sold Vector Logistics and unbundled Rainbow Chicken to create more disciplined focus within each of the businesses.

These initiatives highlight Remgro management’s focus on unlocking the discount and creating value for shareholders. We think that makes for a compelling investment case.

Reinet: A deep-value opportunity hidden in plain sight

Reinet also has its origins in the Rupert family’s business interests. In 2008, Richemont spun off its stake in BAT into a newly listed Luxembourg-based investment vehicle called Reinet Investments, following changes in Luxembourg tax laws. Since then, Reinet has evolved into a diversified investment holding company, with a focus on long-term value creation through a mix of listed and unlisted assets.

Reinet’s most significant investment was in 2012, with an initial GBP400m (around R5bn at the time) stake in Pension Insurance Corporation, a specialist insurer focused on taking over defined benefit pension liabilities from UK corporates. Pension Insurance Corporation’s clients include the pension schemes of multinational corporations such as Rolls-Royce and TotalEnergies. This investment has grown substantially over the years, benefiting from structural tailwinds as employers sought to de-risk their defined benefit pension obligations, combined with excellent execution from a highly skilled management team.

In our view, patience is not just a virtue here – it is likely to be rewarded.

By the end of 2021, Reinet had raised its stake in Pension Insurance Corporation to 49.5%, with the investment growing to account for nearly half of Reinet’s NAV. To date, we have estimated the internal rate of return (IRR) of this investment to be 13% per year in British pounds (GBP). Over the same period (2012-2025), the FTSE/JSE All Share Index (ALSI) returned just 2.2% per year in GBP terms.

Unlocking the value

In January 2025, Reinet announced the full disposal of its BAT stake, raising approximately R31.6bn in cash. This move significantly increased the company’s liquid assets and marked a strategic pivot away from its legacy holdings.

Just six months later, Reinet revealed that Pension Insurance Corporation shareholders and Athora, a European retirement and savings firm backed by Apollo Global Management, had agreed to a sale of Pension Insurance Corporation to Athora for GBP5.9bn (after dividend entitlements). This transaction further bolsters Reinet’s balance sheet and unlocks substantial value from its largest unlisted holding.

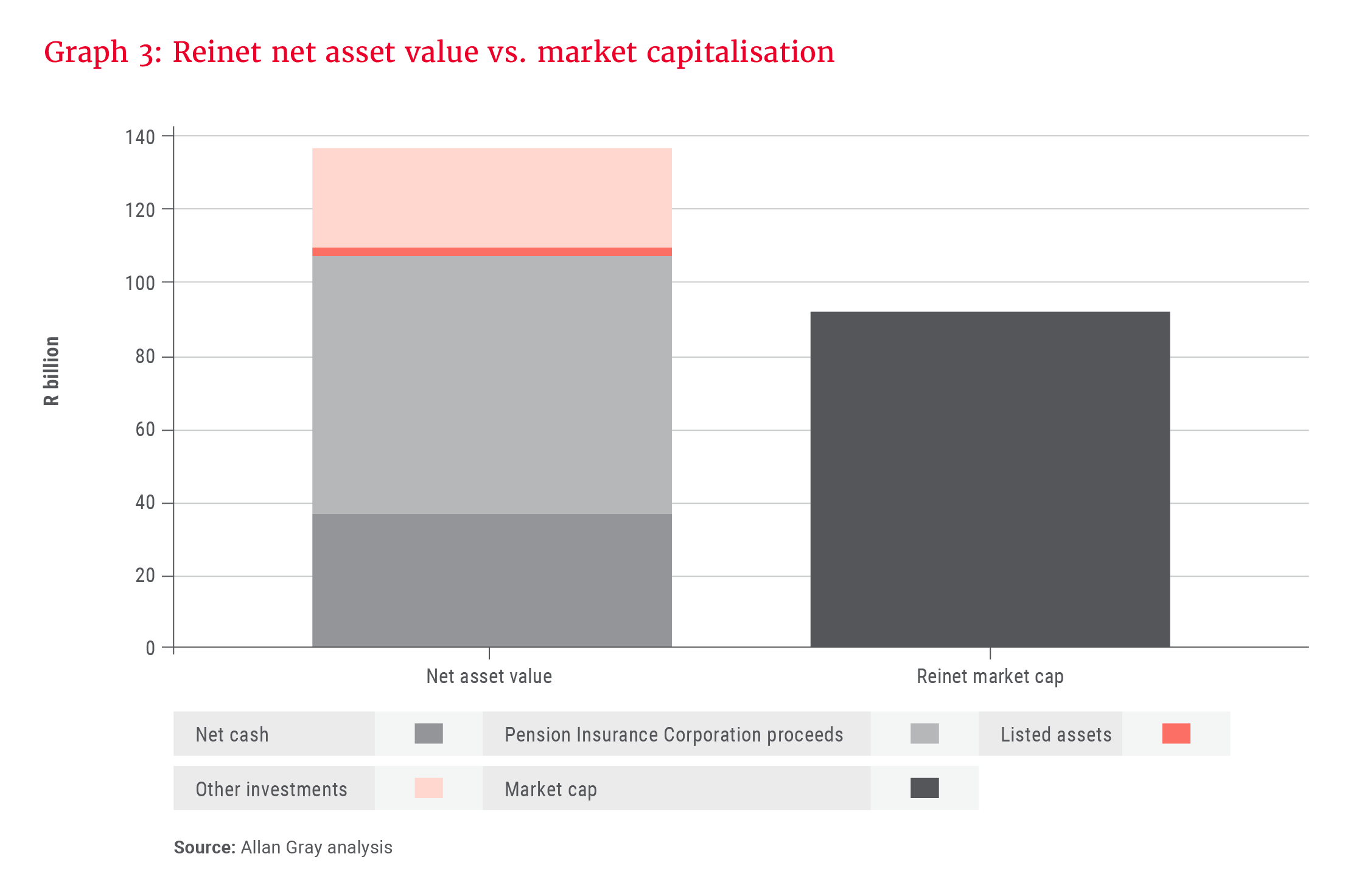

What makes Reinet’s valuation particularly compelling is that its market capitalisation is now lower than the combined value of its net cash and Pension Insurance Corporation sale proceeds, as shown in Graph 3.

Of course, with any investment opportunity that appears to be attractive at first glance, one has to further investigate any underlying risks. For Reinet, our main considerations are:

Fee structure

Reinet’s assets are managed by its general partner, Reinet Investments Manager (the “Investment Manager”). The Investment Manager charges shareholders a fixed annual management fee based on NAV and a performance fee based on total shareholder return over a one-year period. These fees can erode shareholder value over time, particularly in periods of underperformance. We have made provisions for fees payable to Reinet in our valuation.

Private equity valuations

Reinet has R14bn in outstanding commitments to private equity funds. Due to limited disclosure, these assets are often difficult to value independently and are therefore subject to valuation discounts by the market. The current 33% discount to NAV already reflects investor scepticism regarding the private equity holdings. In fact, the market is effectively assigning zero value to these assets. This creates a margin of safety: If the private equity funds deliver even modest returns, they could add upside without requiring a rerating of the rest of the portfolio.

Capital allocation uncertainty: The biggest unknown

What could truly unlock value for shareholders is thoughtful capital allocation. Reinet has multiple strategic options:

- Return capital to shareholders via buybacks or special dividends. Reinet’s management has shown a willingness to act when discounts become excessive: Most recently in 2022, the discount narrowed from 50% to 27% following a buyback programme. The current set-up, where the market capitalisation is below the value of liquid assets, creates a strong incentive for management to act again.

- Wind down the structure, distributing assets directly. Reinet may opt to wind down its structure and distribute assets directly, as the Investment Manager earns lower management fees on cash holdings and no fees on most private equity assets. This reduces the financial incentive for the Investment Manager to maintain the current structure, making a wind-down more appealing from its perspective.

- Reinvest selectively. Reinet also has the option to invest in more transparent or liquid assets. By taking a long-term approach and identifying companies experiencing structural tailwinds, such as the case of Pension Insurance Corporation in 2012, Reinet could generate value for shareholders.

Patience pays off

Recent actions and momentum at both Remgro and Reinet suggest that there is a high probability of the discounts unlocking over time. For long-term investors, these discounts provide both a meaningful margin of safety and potential upside. In our view, patience is not just a virtue here – it is likely to be rewarded.

Explore more insights from our Q3 2025 Quarterly Commentary:

- 2025 Q3 Comments from the Chief Operating Officer by Mahesh Cooper

- How Booking.com changed the way we travel by Thalia Petousis

- Orbis Global Equity: Biotech breakthroughs in a crowded market by Graeme Forster and Mo Zhao

- How to unlock value through offshore investing by Horacia Naidoo-McCarthy and Radhesen Naidoo

- The ALSI's evolution in a changing economy by Matthew Patterson

- How to safeguard your investments by Twanji Kalula

To view our latest Quarterly Commentary or browse previous editions, click here.