Nearly 18 million passenger electric vehicles were sold globally in 2024, up from just 2 million in 2019, and rising from 2.4% to 21% of market share. Can the electric vehicle transition continue unabated, or does a deep dive into the world’s largest car markets – and recent shake-ups within them – present a more nuanced picture? Raine Adams investigates.

Our thematic research into the pace of electric vehicle (EV) adoption globally feeds into our investment research for multiple affected sectors, including the platinum group metals (PGMs), oil and gas, and automakers themselves. While the headline growth in global EV sales to date has been impressive, regional disparities also came to the fore in 2024.

China is in a league of its own

China is dominating the EV transition, accounting for 66% of global EV sales in 2024. Nearly every second car sold in China in 2024 was electric, meaning it was either a battery electric vehicle (BEV), also known as a fully electric vehicle, or a plug-in hybrid electric vehicle (PHEV). The latter should not be confused with a traditional hybrid vehicle. While both have internal combustion engines (ICEs), a hybrid vehicle has a small battery and relies on regenerative braking to charge, whereas a PHEV has a larger battery that can be plugged into an external power source. China’s EV penetration is remarkable considering that they accounted for just 5% of domestic passenger vehicle sales in 2019.

China’s strategic thrust into clean energy technologies … and the benefits provided by its sheer scale have changed the game.

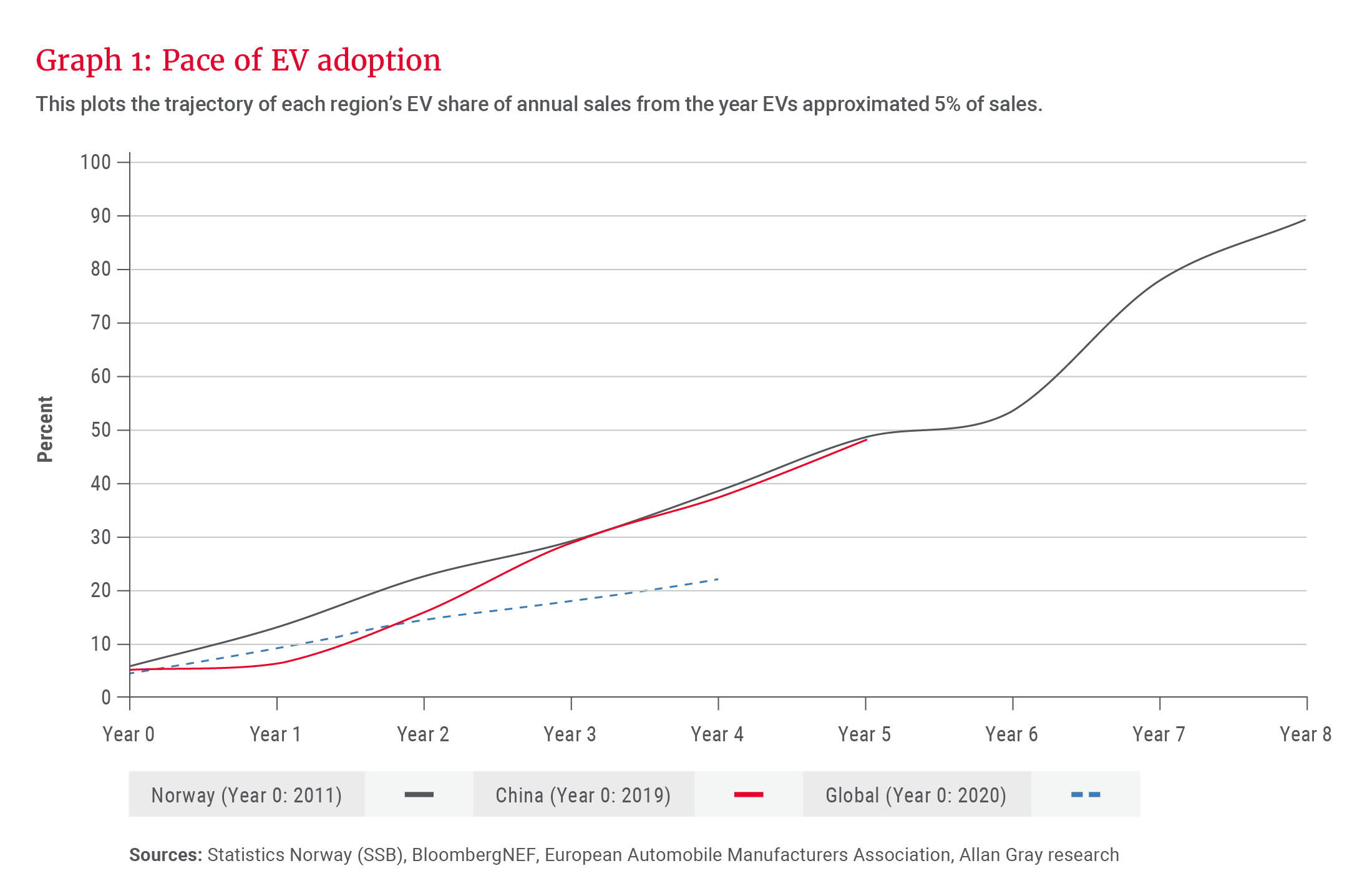

In Norway, the world’s EV front runner, BEVs have reached 90% of annual passenger vehicle sales. Many believed its speed of transition was something of an anomaly owing to its wealth (ironically, built on oil and gas) and the government’s significant incentive schemes for EV purchases. However, the Chinese government followed suit with strong subsidies and other supportive measures, and to date, EV sales in China are keeping pace with the Norwegian experience, as shown in Graph 1, despite a much lower GDP per capita.

China’s strategic thrust into clean energy technologies, meaning complete vertical integration in the EV supply chain, and the benefits provided by its sheer scale have changed the game. Its automakers have managed to produce a far greater range of affordable EVs than has been the case in Western countries, thereby appealing more to the mass market. These are spilling over into other countries, including large emerging car markets such as Brazil and Southeast Asia, and smaller markets like South Africa, which is discussed in more detail further on.

As part of the Chinese central government’s efforts to revitalise economic growth and reduce dependence on oil imports, it continues to support fuel-efficient vehicle sales, including via the recent extension of a 2024 trade-in scheme that offers up to RMB20 000 (US$2 730) when scrapping an old vehicle and purchasing a new EV. This is material considering the average RMB225 000 now paid for an EV in China, and should support domestic EV sales in 2025.

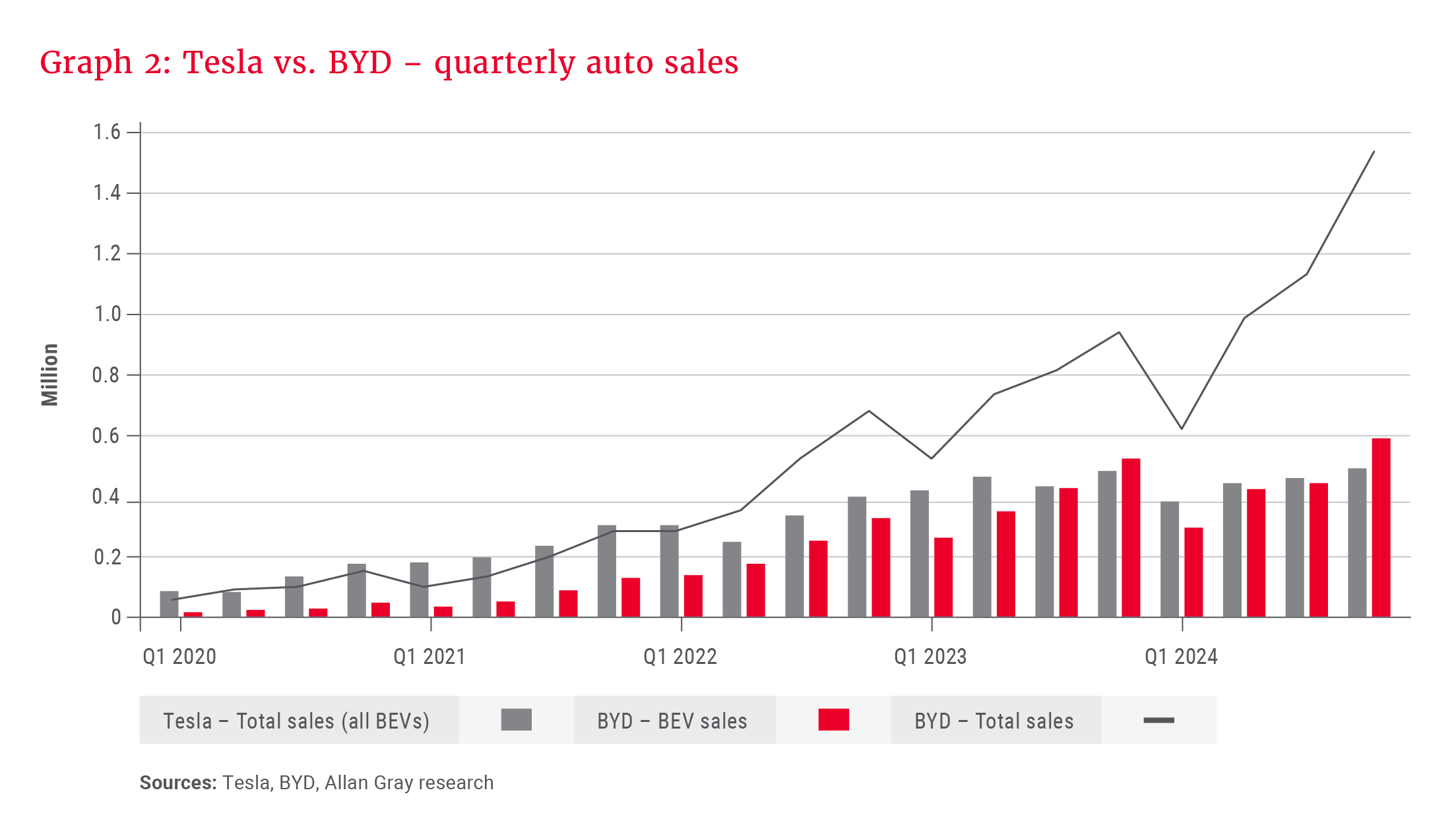

One cannot write about China’s EV market today without mentioning its champion manufacturer, BYD. BYD listed on the Hong Kong Stock Exchange as a battery manufacturer in 2002, but subsequently moved into auto manufacturing. It launched its first PHEV and BEV models in 2008 and 2009 respectively, and discontinued its production of ICE vehicles in 2022 to focus purely on EVs.

While much of the world’s attention has been on US-listed Tesla, whose performance is increasingly challenged by peers, BYD has quietly grown into a formidable contender – if not the market leader. In 2024, it surpassed Tesla’s reported group revenue of US$98bn and the US$100bn mark for the first time, with reported sales of US$107bn. While Tesla sold 1.8 million BEVs, BYD sold 1.8 million BEVs and a further 2.5 million PHEVs and other commercial vehicles, as can be seen in Graph 2, indicative of its lower average price tag per vehicle.

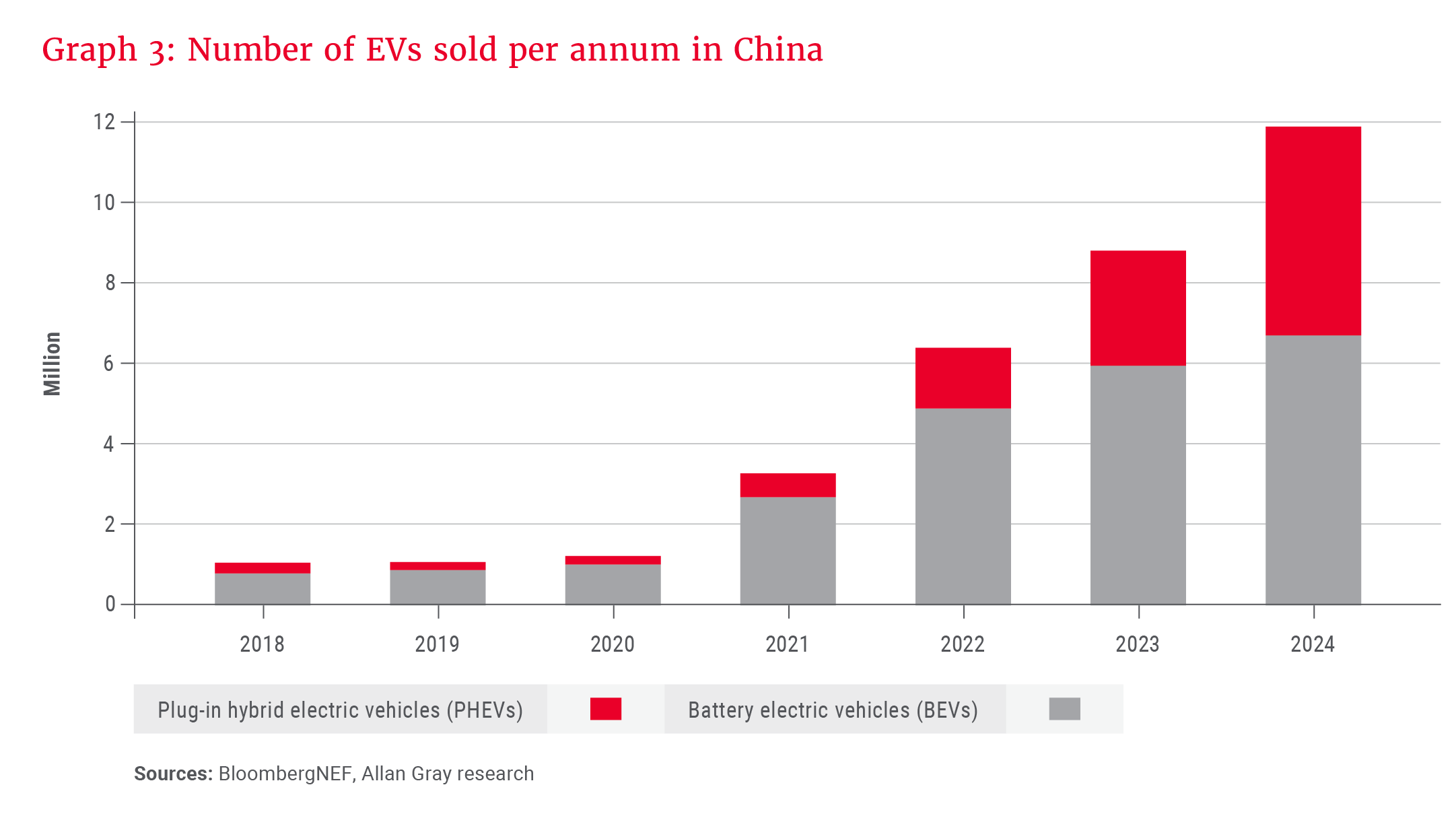

BYD has been instrumental in the rise of PHEVs in China, with these vehicles growing in popularity from 18% of EV sales in 2019 to 44% today (see Graph 3). The rise in demand for extended-range electric vehicles has also played a role – and is something to watch – but these are yet to work their way meaningfully into Western markets.

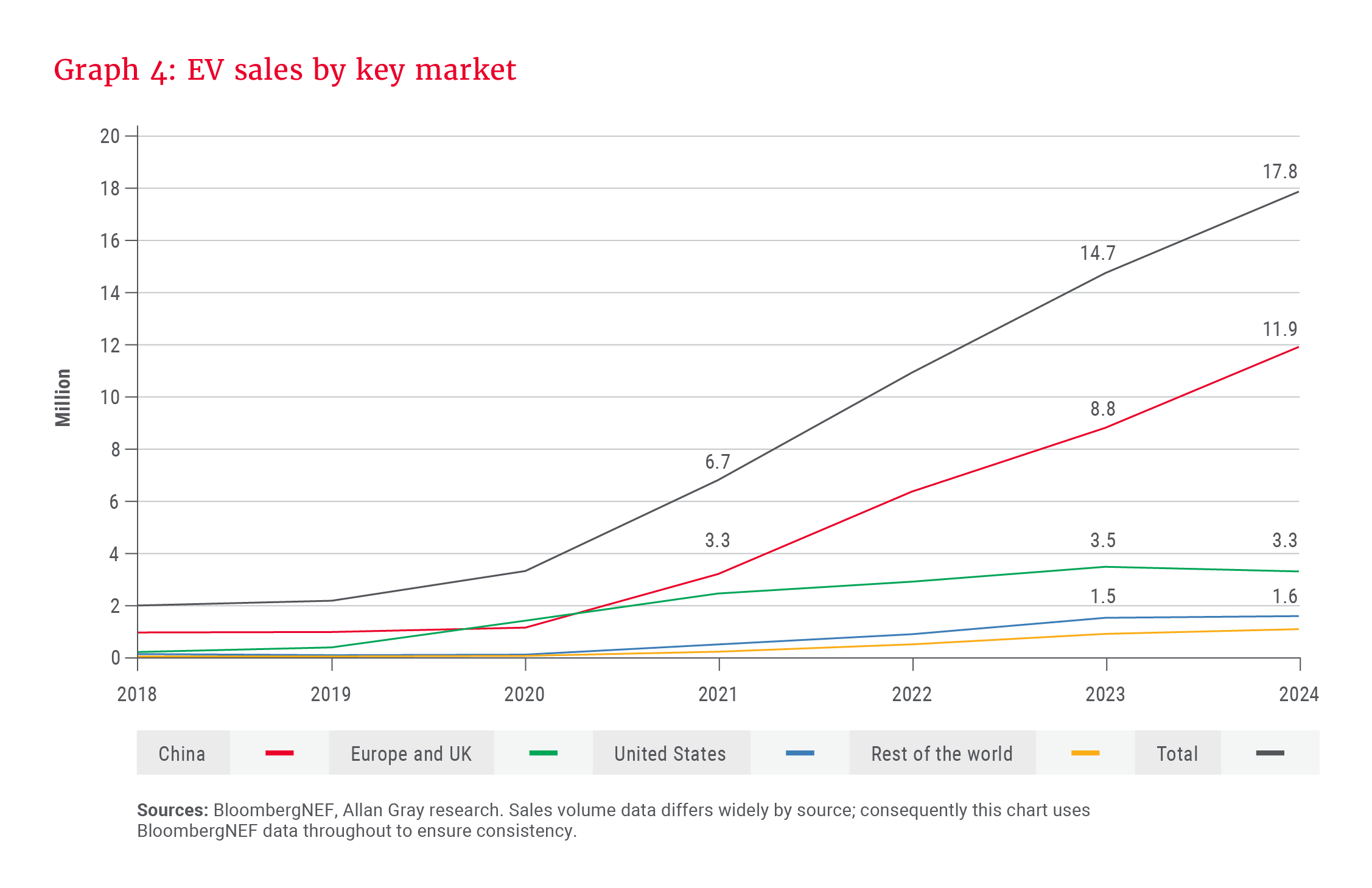

As reflected in Graph 4, while China forged ahead in 2024, the world’s second- and third-largest car markets, the US and Europe, slowed or even declined due to various factors denting consumer demand. These included subsidy changes in several countries, price consciousness considering the higher price points of Western EVs versus ICE vehicles, charging infrastructure accessibility, range anxiety, and residual value concerns. Policy risk was highlighted in Germany, where EV sales plunged 27% in 2024 after government subsidies were abruptly ended due to budget constraints. The key question is whether these are temporary blips in an inevitably fast-paced transition, or indicative of a structural slowdown.

The United States is experiencing a historic disruption

President Donald Trump’s return to the Oval Office promised a global shake-up in 2025, but even so has been surprising in its magnitude. In March, Trump announced imminent 25% tariffs on all cars and car parts shipped to the United States. While Trump’s longer-term goal is to shift more auto production to the US, this is a material disruption for the sector that will increase US vehicle prices and likely dampen new vehicle purchases (despite a short-term spike in sales ahead of the tariffs coming into effect).

Adding to this, Trump’s subsequently announced tariff plans on “Liberation Day” saw trade tensions reach boiling point and have stoked fears of a global recession. While the US “reciprocal” tariffs were not intended to be added to the auto sector’s 25% tariff, the broader impacts of such tariffs could fundamentally reshape the global auto industry and the trajectory of global sales. At the time of writing, Trump had announced a 90-day pause on reciprocal tariffs for all countries except China, for which tariffs were instead significantly hiked – in turn triggering retaliatory duties from the Chinese government. The global macroeconomic outlook remains highly uncertain as the world’s two biggest powers escalate into a trade war (see Sandy McGregor’s piece for a deep dive into tariffs).

… with ongoing EV charging and battery innovations … and significant investments already made in EV manufacturing globally, we do not foresee a fundamental U-turn in the global EV transition.

On EVs specifically, Trump has revoked an executive order signed by former president Biden to target 50% EV sales in the US by 2030, is considering a revocation of EV tax credits approved under the Biden administration’s Inflation Reduction Act (IRA), and has instructed the Environmental Protection Agency to reconsider rules on greenhouse gas emissions, including those passed in 2024 that would require two-thirds of US car sales in 2032 to be EVs or face heavy penalties. It is reasonable to predict a slowdown in EV adoption as the US policy environment shifts. Notably, however, many Republican states have benefited from EV factory investments, and a recent survey showed that most Republicans now support IRA-based EV incentives, so an abandonment of the EV transition is unlikely.

Europe reckons with its embattled auto sector

In Europe, 2025 was anticipated to be a strong rebound year for EV sales as vehicle emission standards tightened significantly. However, the domestic automotive industry has come under severe pressure due to the growing cost of doing business as a result of rising energy and regulatory costs, a slow roll-out of EV charging infrastructure dampening consumer EV demand despite automaker investments therein, and fewer mass-market EV options, meaning that they have lost ground to Chinese EVs both locally and abroad.

In the second quarter of 2024, Chinese brands’ share of EV sales in the EU had risen to 14% from just 2% in 2020. The auto sector received last-minute, albeit temporary, breathing room in March as the EU permitted an extension of the compliance period for vehicle emission targets from a one-year to a three-year average from 2025 to 2027. This is likely to slow short-term EV sales, but currently, the broad policy direction for the EV transition remains intact.

Chinese imports remain the key channel to watch, particularly as price wars have intensified competition and should lead to industry consolidation. Increasingly protectionist stances in the West, however, mean that, in the short term at least, Chinese EV imports are less likely to accelerate their transitions. In 2024, the US quadrupled the tariff rate on Chinese EVs to 100%, a move that was followed by Canada to protect their domestic industries.

The EU has imposed tariffs on China-made BEVs ranging from 8% to 35%, on top of its standard car import duty of 10%, after an investigation found that China’s heavy state support for EV manufacturing created an unfair playing field. Chinese automakers responded by exporting more PHEVs to the region (which are not currently included under the scheme), leading to the EU and Chinese government recently agreeing to reopen tariff negotiations.

South Africa: What is happening at home?

As developed markets seek to curtail Chinese EV imports, emerging markets with less onerous regulations become the next growth avenue for Chinese automakers. South Africa is a much smaller vehicle market than those above, accounting for around 0.6% of global sales. Of the 515 712 new vehicles sold in 2024, just 0.4% were BEVs or PHEVs, while hybrids accounted for a more sizeable 2.6% (dominated by Toyota’s Corolla Cross) and ICE vehicles for the remaining 97%. Nevertheless, the EV market is growing, with BEVs up 35% year-on-year to 1 257 vehicles sold, and PHEVs doubling to reach 728 – potentially indicative of a similar trend to that seen in China.

In the pickup truck segment, which is very popular in South Africa, the recently launched BYD Shark became our first PHEV bakkie, with other launches imminent.

BMW and Volvo currently dominate EV sales, which have focused on the premium market, but Chinese EV launches are growing and opening competition at the lower end. In the pickup truck segment, which is very popular in South Africa, the recently launched BYD Shark became our first PHEV bakkie, with other launches imminent.

EVs and sectoral impacts

2025 is set to be a noisy and disruptive year. Our view is that Western developed market EV sales growth will likely be challenged in the shorter term, particularly depending on how trade wars play out. Slow supporting infrastructure roll-out may also see slower growth in emerging markets outside China. However, with ongoing EV charging and battery innovations (particularly from China) and significant investments already made in EV manufacturing globally, we do not foresee a fundamental U-turn in the global EV transition. We have long believed that, rather than a winner-takes-all environment where BEVs dominate, the transition will take the shape of a multiproduct portfolio, including PHEVs and hybrids. This is starting to play out as Western policymakers shift to a transition approach of “pragmatism and flexibility”.

From a sectoral perspective, the impact of the transition on PGMs and PGM miners is likely front of mind for South Africans, being close to home. Catalytic converters in ICE vehicles consume around 85% of palladium, 90% of rhodium and 45% of platinum demand, meaning that PGM miners are directly negatively impacted by declining ICE sales. While this is an undisputed risk and important consideration in our investment research, again there are nuances. For example, hybrids and PHEVs have similar or slightly higher PGM loadings than ICE vehicles and are on the rise. On the supply side, the weak PGM price environment and future demand uncertainty are curbing investment in production in South Africa, which accounts for over 50% of global primary (i.e. mined) supply, and prompting restructuring considerations. These mines also remain vulnerable to a constrained energy environment and decaying water infrastructure.

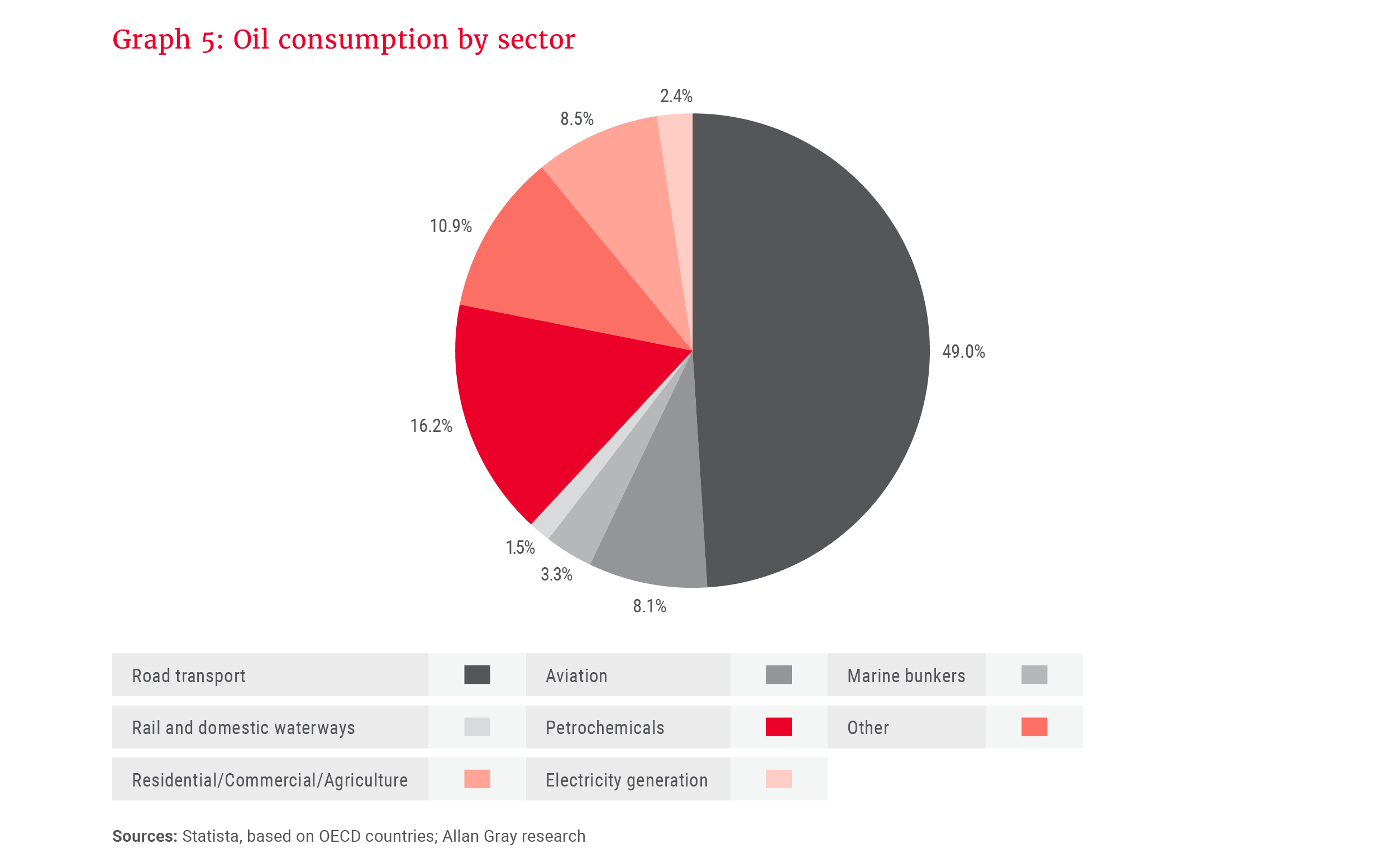

Oil demand is better supported than PGM demand, given the number of ICE vehicles actively on the road. This will take time to roll over. There are about 1.4 billion passenger vehicles on the roads globally today, of which EVs are roughly 4% (and BEVs even less). As Graph 5 shows, road transport, and within this, passenger vehicles, account for 49% and 30% of annual global oil demand respectively. The heavy commercial vehicle segment consumes disproportionately more fuel versus its fleet size and will be slower to decarbonise.

As the country furthest along in its EV transition, Norway offers a glimpse into the future. From 2016, when EVs accounted for 5% of Norway’s passenger vehicle fleet, to 2023, when they had grown to 28% of the fleet, road fuel demand declined by just 16% (on account of PHEVs still consuming fuel). Over this same period, Norway’s total oil demand declined by only 1% cumulatively. As Graph 1 shows, global EV penetration is on a significantly slower trajectory than Norway, and oil demand this decade is likely to be – excuse the pun – sticky. From 2002 to 2012, oil demand growth averaged 1.2% per annum. From 2013 to 2023, this slowed to 0.9%, and in 2024, demand grew by 0.8%. In the next decade, this will likely be lower, but is unlikely to be sharply negative.

Notably, China’s large refiners are calling the country’s peak oil demand in the next few years, meaning that global demand destruction may intensify post 2030. For the decade to 2023, China accounted for more than 60% of global oil demand growth, while in 2024, this declined to 20%. From an offset perspective, the petrochemicals sector and India are oil’s two biggest growth drivers to watch.

The bottom line

Despite the direction of travel for negatively impacted sectors such as PGM miners and oil and gas companies, as bottom-up stockpickers, a company in a “sunset” industry can still be a great investment if the entry price has more than discounted those risks. Meanwhile, a future-facing company that is priced for perfection – much like Tesla – may well be a poor long-term investment if that perfect scenario doesn’t play out.

In 2024, the combined market capitalisation of the world’s top 11 traditional vehicle manufacturers ex-China was not much greater than Tesla’s market capitalisation alone, yet collectively they sold 30 times the number of vehicles and generated 20 times as much revenue. Of course, relative valuations are never this simple, but it highlights how sentiment can drive excessive disparities between the perceived winners and losers – and how bottom-up stockpickers stand to gain from doing their homework.

Explore more insights from our Q1 2025 Quarterly Commentary:

- 2025 Q1 Comments from the Chief Operating Officer by Mahesh Cooper

- Tariffs: The stealth tax by Sandy McGregor

- How to invest in a volatile market by Stephan Bernard

- Orbis Global Balanced: Defensively positioned to deliver long-term returns by Alec Cutler and Rob Perrone

- Allan Gray Orbis Foundation: 20 years of purpose-driven impact by Nontobeko Mabizela

- A phased approach to your retirement journey by Nshalati Hlungwane

To view our latest Quarterly Commentary or browse previous editions, click here.