The US government has dug itself into a debt hole. With spending being its go-to solution for most problems, it is unclear how the situation will be resolved. Worryingly, some of the mooted solutions are likely to negatively impact the entire savings industry. Thalia Petousis looks at why the current trajectory of debt is unsustainable.

"Under current policy and based on this report’s assumptions, [United States government debt relative to GDP] is projected to reach 566 percent by 2097. The projected continuous rise of the debt-to-GDP ratio indicates that current policy is unsustainable." - Financial Report of the United States Government, 16 February 2023

It is well understood that the United States government has a debt problem. To be a bit more exact, a US$34.5tn debt problem. If one wants to split hairs, or flatter the numbers, then the problem is only US$27.3tn when reflecting the value of US debt “held by the public” (i.e. across institutions like commercial banks, mutual funds, and the global savings industry), while the remainder is owned by the US Federal Reserve (the Fed), the country’s central bank. This means that the volume of sovereign debt in issuance is equivalent to 124% of the size of the US economy, as measured by its gross domestic product (GDP), or 98% of GDP if one strips out the Fed’s holdings.

As large healthcare spending and unrestrained fiscal budgets have become the norm, so has larger government debt.

None of this information is “new news”, which seems to lull market participants into a sleepy sense of comfort with the status quo, despite some arguably ominous developments in the situation. The first of these is the US Office of Debt Management’s deteriorating long-dated forecasts of the debt trajectory. Next is credit rating agencies’ increasingly sour and more discerning assessment of the situation. The third, and arguably most interesting development, is a paper published by the St. Louis Federal Reserve last year, in which they debated how this debt problem will be “solved”. Stated differently: What is the endgame?

The deterioration in US debt management office forecasts

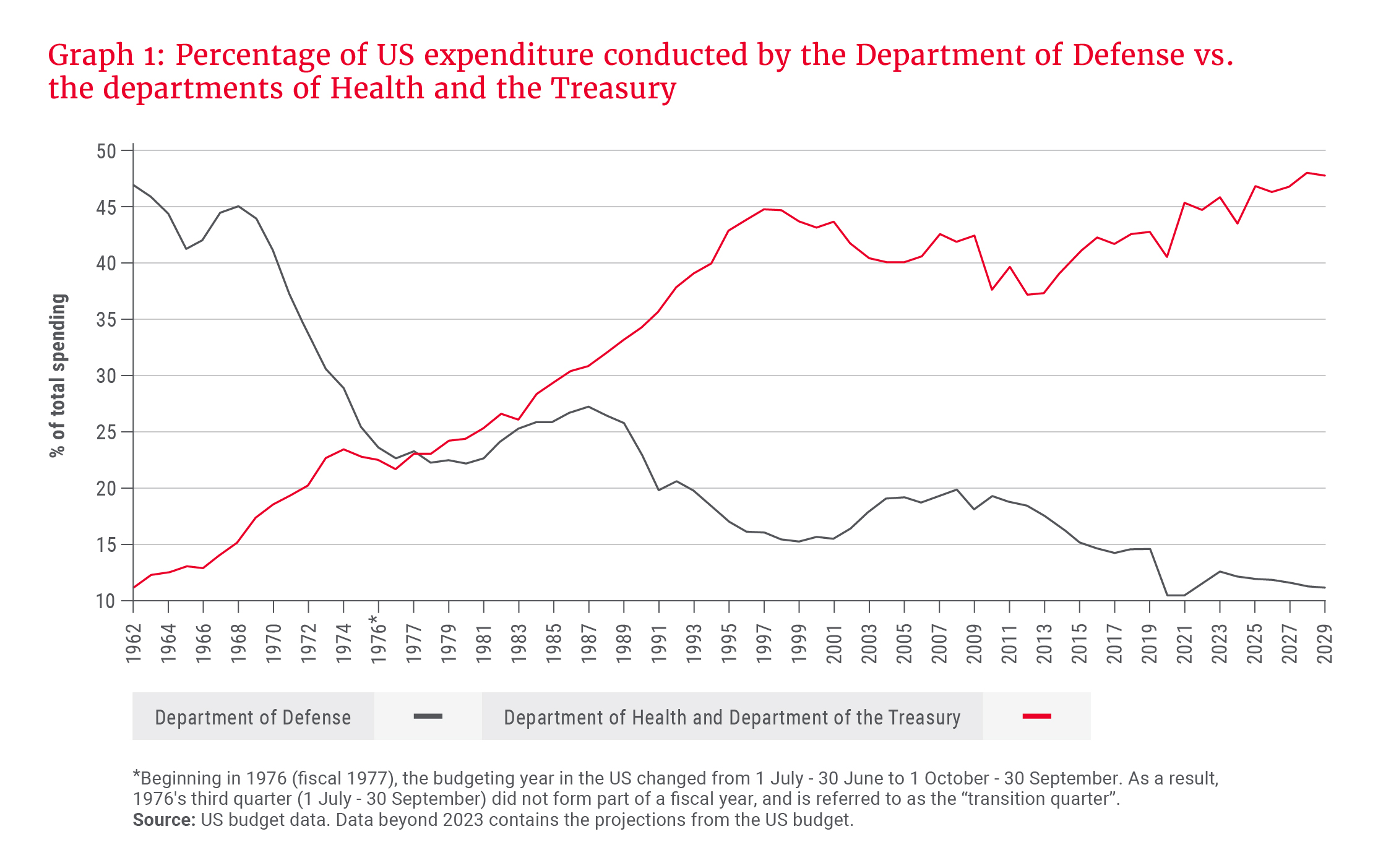

The largest ticket spending items in the US budget are healthcare, social security, defence, and interest payments, but the distribution of these expenditure items has shifted enormously over time. Since the end of World War II in 1945 and the emergence from the Cold War years in the 1990s, global spending on military defence has gradually fallen. The establishment of the North Atlantic Treaty Organization (NATO) and its key tenet that “an armed attack against one or more shall be considered an armed attack against them all” has underpinned collective security and 30 years of global peacetime. From 1962 to the present, US spending by the Department of Defense has fallen from 47% of total national spending to just 12.6% – as seen in Graph 1. In its place, the US has seen a phenomenal rise in healthcare spending. As large healthcare spending and unrestrained fiscal budgets have become the norm, so has larger government debt. This debt must naturally be serviced by the Department of the Treasury as it pays out interest to debtholders, also called lenders. Graph 1 reflects that the departments of Health and the Treasury now account for 46% of combined US national spending, from just 11% in 1962.

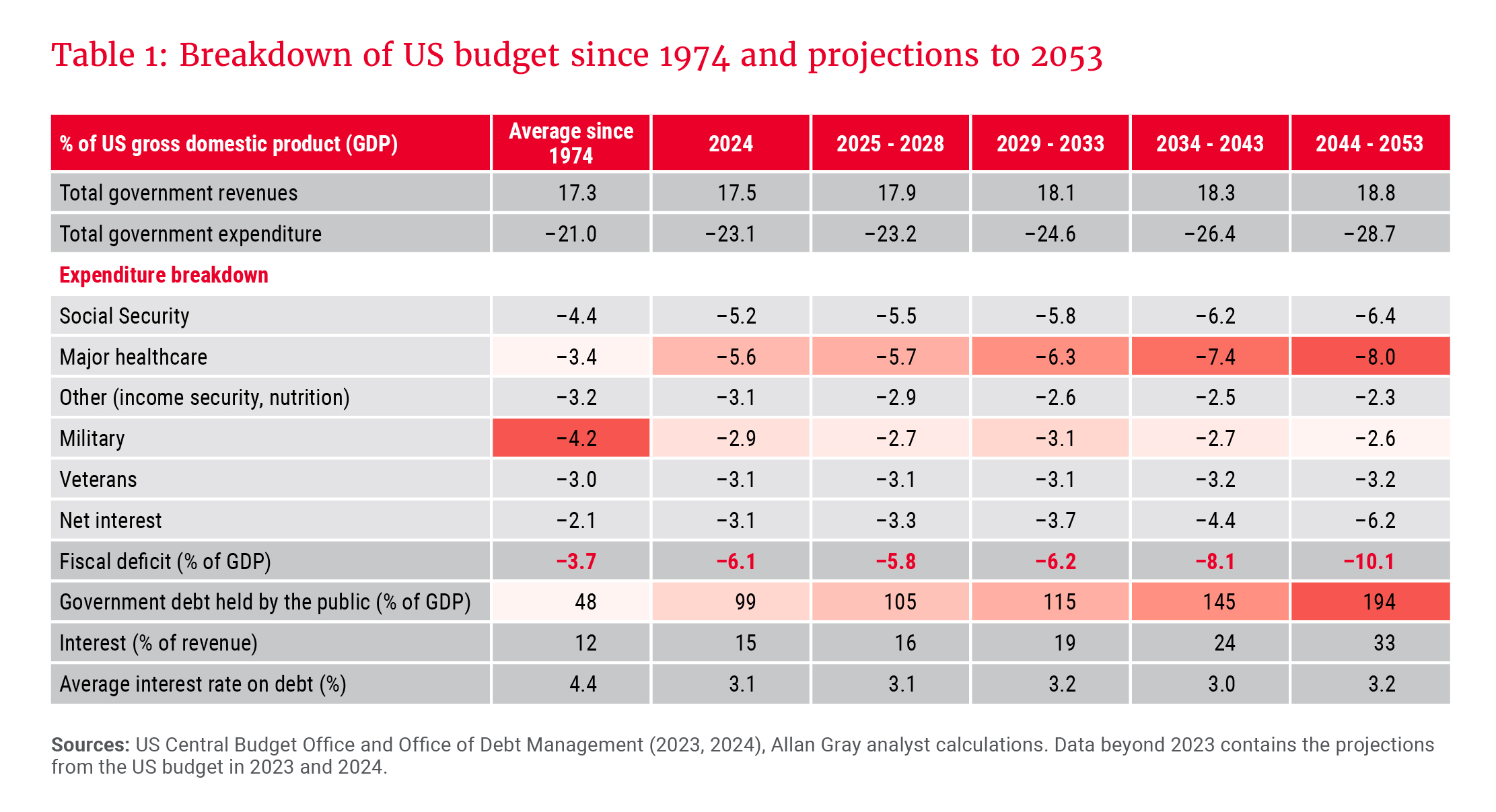

On average since 1974, US government revenue (which is predominantly taxes) has averaged 17.3% of GDP, while expenditure has averaged a greater 21% of GDP. As reflected in Table 1, this has led to an average deficit of 3.7% of GDP per annum, which must be funded by borrowing. On average since 1974, the quantum of US government debt held by the public has been 48% of GDP, but it has been steadily growing, to reach an expected 99% in 2024. The projections for 2024 and beyond show the enormous rise in expected “major healthcare” spending as a percentage of GDP.

Why does the US spend so much on healthcare? The Centers for Disease Control and Prevention (CDC) estimates 50% of US adults (approximately 142 million people) will be obese by 2030, compared to 42% (115 million) currently. This implies that the number of obese adults will grow at a compound annual rate of 2.5% to 2030, outstripping the rate of population growth, which is predicted to decline over the period. Additionally, an estimated 31% of US adults (85 million) are currently in the overweight category, but just shy of obese.

Obesity is naturally associated with greater risk of heart disease, stroke, diabetes, and a range of other ailments that weigh on hospital budgets and healthcare spending. Recently, much attention has also been devoted to trying to quantify the economic cost of the US opioid epidemic, or abuse of prescription painkillers, in terms of both lost productivity and more direct healthcare and criminal justice spending. Additionally, much of the rise in expected healthcare spending to 2050 is underpinned by the ageing of the large baby boomer generation, who will be requiring elderly assistance, while productivity will simultaneously be lost within the economy.

Since 1974, an average of 12 cents on every tax dollar have gone towards servicing debt, as reflected by the interest (as a percentage of revenue) row in Table 1. As shown in the table, using a net interest rate of 3%, the Treasury projects that 33 cents on every tax dollar will go towards servicing interest on debt by 2053.

[The US] ran up government spending enormously to stimulate the economy and bail out the banking system.

That said, there are large forecast risks underlying these assumptions. Firstly, the Congressional Budget Office assumes that military spending will decline over the forecast period, which is at odds with the increasing armed conflict we are seeing across a politically divided world. Additionally, the assumption of a 3% average interest rate on US debt might be far too conservative. If one uses a 4% rate of interest, then the US will be paying 33 cents on every tax dollar towards servicing interest within the next decade, and by 2050, that will have ballooned to 40 to 50 cents on every tax dollar. This would be a higher interest service burden than what is paid by many African sovereigns (South Africa pays 21 cents at present, and Senegal pays only 9 cents). When governments reach the point of paying 50 cents of interest service on every tax dollar is typically when they begin to default on debt.

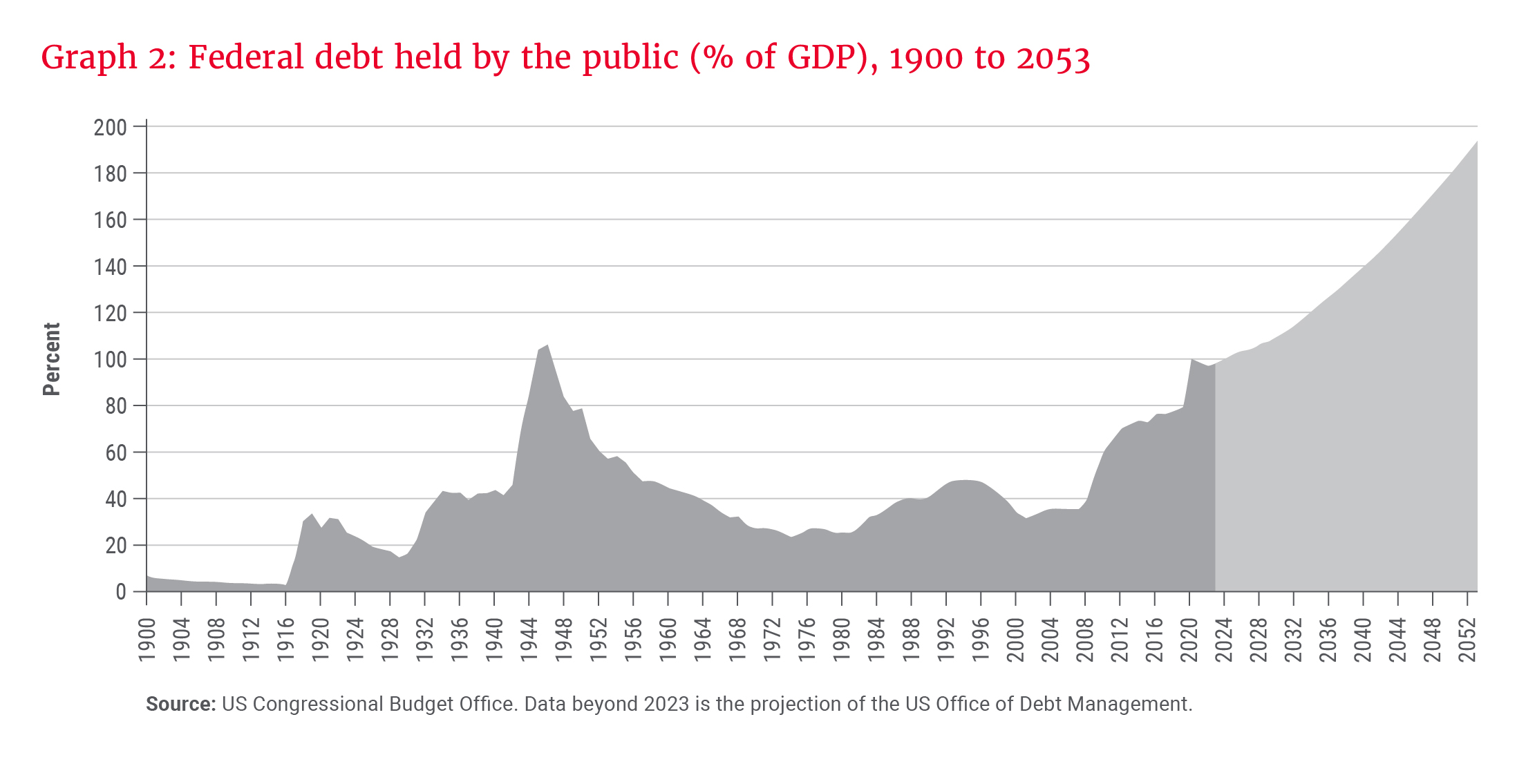

Using the assumptions of the debt management office in Table 1, US debt held by the public will reach around 200% of GDP by 2053, as seen in Graph 2. When many developed market sovereign debts reached north of 100% of GDP during the post-World War II era, it was only via both rapid inflation and the financial repression of savers that this could be resolved.

Credit rating agencies acknowledge the problem

Last year, the global credit rating agency Fitch joined the ranks of other agencies who will no longer afford the US government a AAA credit rating, instead downgrading them to one below (AA). Fitch cited the looming insolvency of the US Medicare Hospital Insurance Trust Fund and US Social Security Trust Fund in the next decade as a key consideration in their decision, which represented a refreshingly prescient set of observations. They also cited the erosion of governance over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions.

The decision to downgrade the US was arguably long overdue – the AAA-rated peer group is a class of sovereigns with debt of only 39.3% of GDP on average. This is a level of debt that the US last held prior to the 2008 global financial crisis. It subsequently ran up government spending enormously to stimulate the economy and bail out the banking system.

Fiscal dominance and the endgame

What, then, is the endgame, and how does the US avoid a default in the next 30 years? Will the discussed dynamics lead to the uncontrolled inflation seen following World War II, when developed market government debts surpassed the 100% of GDP threshold?

... it is quite possible that a fiscal dominance episode in the US would result in a financial repression of the entire savings industry …

Fiscal dominance refers to the possibility that the accumulation of government debt and continuing government deficits will produce increases in inflation that “dominate” central bank intentions to keep inflation low. This conundrum, as well as that of borrowing from the future, only to find that the debt is no longer realistically serviceable by that future date, was addressed by the St. Louis Federal Reserve in the aforementioned paper published last year. It argued that by the year 2050, one of the only practical solutions to the problem of fiscal dominance might be the elimination of the payment of interest on reserves. Reserves are the cash that commercial banks are required to keep at the US Federal Reserve (its central bank). The Fed pays out interest on these reserves on behalf of the US government. The above “solution” therefore implies a financial repression of the US banking industry such that the banks will no longer earn interest on cash forcibly held at the Fed:

"If the government wishes to fund large real deficits, that will be easier to do if the government eliminates the payment of interest on reserves. This potential policy change implies a major shock to the profits of the banking system." – Federal Reserve Bank of St. Louis, 2 June 2023

The St. Louis Federal Reserve took this idea a step further and suggested that the amount of zero-interest reserves kept at the Fed might need to be as high as 40% of deposits. In such a world, banks would likely cease to pay interest to their end clients. As such, it is quite possible that a fiscal dominance episode in the US would result in a financial repression of the entire savings industry via high inflation and an artificially low rate of interest being maintained in an economy that does not compensate one for the erosion of wealth. In such an environment, long-duration fixed-rate bondholders could suffer enormously.

This notion was, in fact, well acknowledged by the St. Louis Federal Reserve, as seen in their honest assessment of the situation in the said paper:

"If the bond market does not anticipate a fiscal dominance shock sufficiently far in advance (where the definition of “sufficiently far” is determined by the duration of bonds held by the public), then bond investors would be caught with losses on high-duration bonds. All of these changes imply that the effects on banks and mutual funds and pension funds and others would be potentially quite dramatic.”

One man’s financial repression is another man’s prudent regulation.

One man’s financial repression is another man’s prudent regulation. The measures discussed by the St. Louis Federal Reserve have been the only mechanism by which we have seen developed market sovereigns resolve enormous levels of debt in the past. Generally, the market tends to think of a “debt default” as an explicit announcement of non-payment followed by an explicit haircut on bondholders. A far more insidious way of extracting cash from the savings industry, which is nonetheless as damaging for the public and for savers, is the erosion of savings not only via high inflation, but via intentionally suppressing the interest rates that are paid on those savings – in this case to nil.